RTO Insider

CAISO/WEIM

ERCOT

FERC & Federal

ISO-NE

MISO

NYISO

PJM

SPP

ERO Insider

FERC & Federal

NERC & Committees

Regional Entities

Resource Adequacy

Standards/Programs

State Regulation

NetZero Insider

Agriculture & Land Use

Building Decarbonization

Commentary & Special Reports

Company News

Equity & Economics

Federal Policy

Generation & Fuels

Impact & Adaptation

Industrial Decarbonization

State and Local Policy

Technology

Transmission & Distribution

Transportation Decarbonization

Calendar

Bookmarks

Skip to content

RTO Insider

CAISO/WEIM

ERCOT

FERC & Federal

ISO-NE

MISO

NYISO

PJM

SPP

ERO Insider

FERC & Federal

NERC & Committees

Regional Entities

Resource Adequacy

Standards/Programs

State Regulation

NetZero Insider

Agriculture & Land Use

Building Decarbonization

Commentary & Special Reports

Company News

Equity & Economics

Federal Policy

Generation & Fuels

Impact & Adaptation

Industrial Decarbonization

State and Local Policy

Technology

Transmission & Distribution

Transportation Decarbonization

Calendar

RTO Insider Events

ERO Insider Events

NetZero Insider Events

July 26, 2024

Log In

Subscribe

July 27, 2024

`

July 27, 2024

Log In

Email address:

Password:

Login

Reset

Close

A link has been emailed to you - check your inbox.

Already registered?

Login

Reset your password?

Reset Password

Looking to read the full article? Scroll down and login or sign up today!

Page Reload Scroll Position

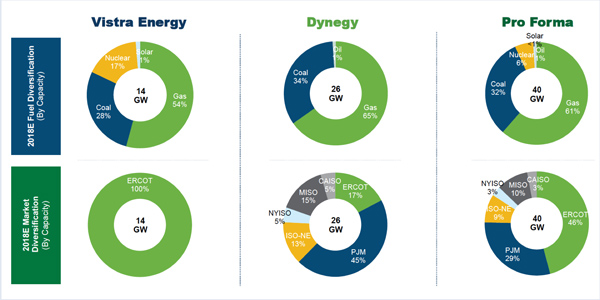

Vistra Energy Swallowing Dynegy in $1.7B Deal

Oct 30, 2017

Vistra Energy will acquire Dynegy in a $1.7 billion all-stock deal that will create a generation giant owning 40 GW of capacity.

Company News

ERCOT

ISO-NE

PJM

Keywords

Dynegy

Electric Reliability Council of Texas (ERCOT)

ISO New England (ISO-NE)

merger

PJM Interconnection LLC (PJM)

Vistra Energy

Michael Kuser

NY Legislators Frustrated by Lack of Answers at ZEC Hearing

More From This Author

→

We Recommend

1

CenterPoint CEO Promises PUC Utility Will ‘Improve’

Jul 25, 2024

Company News

Tom Kleckner

2

MISO Sets Sights on 50% Peak MW Cap in Annual Interconnection Queue Cycles

Jul 25, 2024

MISO

Amanda Durish Cook

3

NRDC: Coal Plants Squeezing Out Cheaper Resources in MISO Market

Jul 24, 2024

Markets

Amanda Durish Cook

4

Order 1920 Debated at House Hearing with All 5 FERC Commissioners

Jul 24, 2024

FERC & Federal

James Downing

5

NV Energy Should Do More to Tap VPP Potential, Report Says

Jul 25, 2024

CAISO/WEIM

Elaine Goodman

Popular Stories

1

10 Northeastern States Sign MOU on Interregional Transmission Planning

Jul 9, 2024

Public Policy

James Downing

2

Pathways Participants See ‘Pivotal’ Chance to Build New Kind of RTO

Jul 15, 2024

CAISO/WEIM

Robert Mullin

3

Talen Energy Deal with Data Center Leads to Cost Shifting Debate at FERC

Jul 11, 2024

Company News

James Downing

4

Stakeholders Battle over Battery as Proxy in NYISO Demand Curve Reset

Jul 7, 2024

Markets

Vincent Gabrielle

5

SPP’s Experience with Seams Could Help Markets+

Jul 15, 2024

Markets

Tom Kleckner

Industry Gatherings