NYISO exceeded its winter baseline peak load forecast on Feb. 7 with 24,317 MW, COO Emilie Nelson told the Management Committee on Feb. 25.

The baseline forecast was 24,200 MW. From Jan. 25 to 30, load ranged from 23,417 to 24,177 MW. Demand response contributed “several hundred” megawatts of net load relief, Nelson said, with NYISO calling on its DR programs six times in January and an additional two times in February. “This is an unprecedented level for the winter.”

Wind performed “as expected” during the month. Roughly 2.4% of wind generation was curtailed during January. Solar always performs worse in winter but was basically unavailable for the worst of the month. Nelson pointed to Jan. 25, the start of Winter Storm Fern, when snow and heavy cloud cover began blanketing most of the state.

“Solar drops down entirely,” Nelson said. “You had a significant snowstorm and then it stayed cold, so you had snow on panels, and you did not get behind-the-meter solar generation.”

The peak of winter consumption occurs in the early evening, which she said made the issue even worse. Without solar to blunt it during the day, fuel demand remained high both on- and off-peak, straining resources.

“So much of managing a winter event is managing scarce energy,” Nelson said. “The fact that you have less solar production during the day with snow on panels makes managing those liquid fuels and scarce energy that much more important and challenging.”

She segued into a discussion of unavailable resources in the day-ahead market during the same period. Fuel shortages, inclement weather and difficult travel conditions forced many dual-fuel units offline. (See NYISO Recounts Challenges During January.) This continued into early February, Nelson said.

“You can see some pretty high numbers here, ranging from about 1,000 MW to up to 2,000 MW on a daily basis throughout,” she said.

Kevin Lang, representing New York City, asked whether this was comparable to prior winter storms. Nelson said it was about the same.

“If what we’re seeing is consistent with prior storms, that actually is good news that we’re not seeing a falloff in production or performance,” Lang said.

Aaron Markham, vice president of operations for NYISO, said that while it was broadly “good” news, it was still challenging to manage the high number of forced outages in both the real-time and day-ahead markets.

Another stakeholder said that while the number of forced outages might be roughly on par with what was seen before, it was important to remember that New York had fewer resources overall to call on, which made system conditions more stressful.

“I want to highlight the extraordinary efforts that were taken this time to keep units running, things like climbing up and knocking ice off fans in sub-zero weather,” said Doreen Saia, a lawyer from the Greenburg Traurig law firm representing generation interests. “I think we need to be careful. … It was a significant test for the system.” She said she didn’t want anyone to walk away from the meeting thinking things were fine.

Another stakeholder pointed out that external control areas actually received roughly 1,000 MW of exports from NYISO.

“I think it’s time we review how generous we can be under these cold snap conditions,” they said. “It’s a mess. We can’t have all these alerts and no major emergencies. That tells me something is going on.”

Stakeholders requested that the ISO identify which zones the outages were concentrated in and what the causes of the outages were. Nelson said that Markham was planning on covering the causes of the outages in his upcoming incident report.

Nelson said NYISO was not planning on identifying where these outages occurred. Other stakeholders asked whether the ISO could present the data in an anonymous form so they could understand the outages better.

Another stakeholder asked whether the ISO could highlight what system conditions were causing wind curtailments during the periods of high demand. They said it would be helpful for identifying necessary system upgrades.

ERCOT says it plans to use a third workshop to inform the discussion with stakeholders on the Dispatchable Reliability Reserve Service, which faces a June deadline to be brought before the Board of Directors.

The DRRS product, now in its third iteration since being mandated by Texas law in 2023, requires resources providing the service to be capable of running for at least four hours at their high sustained limit (HSL); to be online and dispatchable not more than two hours after being deployed; have the flexibility to address inter-hour operational challenges; and reduce the amount of reliability unit commitment by the amount of DRRS procured.

Keith Collins, ERCOT’s vice president of commercial operations, told the Technical Advisory Committee on Feb. 25 that staff’s position is to get more information on the product’s four-hour capability at HSL during the DRRS’ upcoming March 9 workshop. HSL is the maximum, non-curtailed, five-minute sustained energy output capacity a generator can produce, updated in real time by qualified scheduling entities.

“It’s come up a few times in the workshops related to how to consider the four-hour capability at HSL and how to consider that element,” Collins said.

ERCOT has filed two protocol changes and two related changes to the Nodal Operating Guide to make DRRS a reality. The first (NPRR1309) would meet all statutory criteria while also allowing online resources to participate. It would enable the product to be awarded in real time and would co-optimize its procurement with that of energy and other ancillary services under the new Real-Time Co-optimization market tool.

NPRR1309 has been granted urgent status and is due before the board for its June meeting.

The second protocol change (NPRR1310) has not been accorded urgent status. It would add energy storage resources as DRRS participants and a release factor so the product can support resource adequacy.

NPRR1310 “can be addressed as part of the market design elements of the reliability assessment later this year,” Collins said, referring to the biennial Grid Reliability and Resiliency Assessment, which is required by state law.

TAC members also discussed a Feb. 23 ERCOT market notice that directed transmission service providers within West Texas counties to include a no-solar scenario as part of their large load interconnection studies. ERCOT has identified an emerging reliability risk of local load shed in the region during low-wind conditions at night, especially during transmission and thermal resource outages.

ADER Pilot Expands

ERCOT staff updated TAC members on the Aggregate Distributed Energy Resource (ADER) pilot project, saying seven resources are fully participating in the program, providing 193 MW of energy and ancillary services as of February.

Staff have also accepted six additional ADERs that are in various stages of registration and qualification but cannot yet participate.

“The good news story is that the ADER pilot is growing, and it’s been growing significantly, particularly toward the second half of last year into this year,” said Ryan King, manager of market design. Existing QSEs expanding under a developed business model that meets telemetry requirements account for much of the growth, he said.

The seven ADERs offer 107.7 MW capability for energy, 35.4 MW capability for non-spinning reserve service and 49.9 MW capability for ERCOT Contingency Reserve Service. The total ADER qualified and potential capacities are 121.4 MW, 35.4 MW and 49.9 MW, respectively.

King said concerns remain within ERCOT that the pilot is moving too far and too fast on ancillary service limits. Those limits are necessary to manage system impacts and the ability of staff and resources to be able to support the pilot, he said.

The program’s governing documents allow ERCOT to increase limits as needed. It plans to increase the registered capacity limit from 200 MW to 500 MW and the QSE limit from 20 to 90%. The AS service limits will remain the same.

King promised further updates in the second quarter on plans to move the pilot into the protocols.

Members Praise Departing Maggio

TAC members heaped praise on Dave Maggio, director of market design and analytics, who is leaving ERCOT after 19 years for a position with Energy and Environmental Economics.

Among those offering plaudits was former ERCOT COO Kenan Ögelman, now vice president of strategic projects and optimization at the Lower Colorado River Authority.

“The words that come to mind are ‘intelligence,’ ‘industriousness,’ ‘calm,’ ‘compassion’ and — the one I know for sure I don’t have in bunches — ‘structured.’ You’re so good at putting everything together and moving things along,” he said.

“I’ve always appreciated just how talented you are at taking very complex and technical matters,” Vistra’s Ned Bonskowski said. “You’ve always been very good about engaging directly on the level and helping break it down in ways that all the different stakeholders can engage with, identifying what the real concerns are and finding solutions that help make consensus happen. … That’s something that I think all of us as stakeholders will need to embody, and in the Dave Maggio spirit.”

“The way you deal with issues is unique and just a rare skill set of exceptional knowledge on subject matter. … You will be missed greatly,” Reliant Energy Retail Services’ Bill Barnes said.

Speaking remotely by phone, Maggio said he was “overwhelmed with all the kind words” and that it was an honor to work at ERCOT.

“Not just for ERCOT the company, but with ERCOT the market and ERCOT the stakeholders,” he said. “I’m very grateful to you all. I’m proud of the work we’ve done together over the last almost two decades. Perhaps I’ll have an opportunity to work with you all again in another capacity.”

Maggio’s last day at ERCOT is March 12.

LLWG Leadership Retained

Longhorn Power’s Bob Wittmeyer, chair of the Large Load Working Group, asked that TAC’s approval of the stakeholder group’s leadership be placed on the combination ballot as evidence of his “bigger idiot theory.”

“We did poll the [LLWG] for stupid volunteers, and we have the same idiots we had last time,” he cracked. “However, I would be OK if someone said this was a really bad idea and had a bigger idiot.”

Unfortunately for Wittmeyer and ERCOT’s Patrick Gravois, vice chair, there were no takers, and both retained their positions unanimously.

The combo ballot also included Pedernales Electric Cooperative staffer Eric Blakey’s nomination as vice chair of the Protocol Revision Subcommittee and singular revision requests for the protocols, the Operating (NOGRR) and Planning (PGRR) guides, and the Verifiable Cost Manual (VCM) that, if requiring board approval, will:

NPRR1314, PGRR139: Relocate each term and acronym from Planning Guide section 2: Definitions and Acronyms to the protocols and align related defined acronym usage. The NPRR also eliminates the abbreviations for “Current Year” and “Future Year” to avoid future confusion.

NOGRR281: Modify when an approved mitigation plan can be executed.

VCM44047: Remove the association between the term “long-term service agreement” and the abbreviations “LTSA,” which represents “Long-term System Assessment” in the Planning Guide.

NERC and the regional entities had reduced their backlog of compliance cases by almost 50% by the end of 2025, the ERO said in the annual report of its Organization Registration and Certification Program and Compliance Monitoring and Enforcement Program.

The ERO Enterprise had 2,601 open violations at the end of 2025, according to the report, down from the 2,996 at the end of 2024, as reported in the 2024 ORCP and CMEP annual report. More than 80% of open cases were first reported within the past three years, NERC said; by contrast, 92% of the open cases at the end of 2024 were fewer than three years old.

The annual ORCP and CMEP report is intended to help NERC and the REs track their progress achieving goals across the four focus areas identified in the ERO’s long-term strategy:

Energy: Help stakeholders and policymakers address existing risks to grid reliability and prepare for emerging risks.

Security: Enhance the security posture of the industry through existing cyber and physical security programs.

Engagement: Ensure stakeholders and policymakers have access to accurate and trustworthy information from the ERO Enterprise.

Agility and sustainability: Coordinate team activities effectively while delivering value for stakeholders and capturing cost efficiencies when practical.

NERC wrote in the report that 1,054 of its open violations at the end of 2025 were reported the same year. This represents a slight decline from the previous year, when 1,162 of the open violations at year’s end were reported in 2024, but it does not include the violations that were processed the same year, which represented 38% of the total in 2025. The previous year’s report did not include this figure.

NERC’s Critical Infrastructure Protection standards once again accounted for the largest number of violations reported to the ERO in 2025. The most-reported standard was CIP-010-4 (Cybersecurity — configuration change management and vulnerability assessments), with 245 violation reports received — more than the top three most-reported operations and planning (O&P) standards combined.

CIP standards also were the top three most represented standards for moderate-risk violations, with 40 infringements reported for CIP-007-6 (Cybersecurity — system security management), 20 for CIP-010-4 and 17 for CIP-003-8 (Cybersecurity — security management controls). On the other hand, the only three serious-risk violations reported in 2025 concerned the O&P standards IRO-001-4 (Reliability coordination — responsibilities), PRC-023-6 (Transmission relay loadability) and TOP-001-6 (Transmission operations).

The report also provided an update on NERC’s processing of minimal-risk violations, which the ERO identified as a key performance metric in a June 2025 filing following up on its five-year performance assessment. (See NERC Details Performance Metrics in FERC Filing.)

NERC wrote that it and the REs have worked to improve processing efficiency by streamlining the reporting template for compliance exceptions (CEs) — which allow minimal-risk violations to be processed without penalty and without affecting future violation penalties — along with updating the registered entity self-report and mitigation plan user guide and training.

About 83% of noncompliance reports processed in 2025 were handled as CEs, NERC wrote, with another 14% disposed under the Find, Fix, Track and Report (FFT) program, another option for addressing minimal-risk violations. Like the CE program, FFT requires registered entities to mitigate the noncompliance and make the facts and circumstances of the incident available for review by NERC and appropriate governmental authorities.

Of the remaining violations processed in 2025, 35 were covered by NERC’s monthly spreadsheet notice of penalty and 23 in a notice of penalty. In all, NERC processed 1,945 violations in 2025, 281 more than the year before.

The state authority managing New York’s clean-energy transition has estimated one part of complying with the state’s landmark climate law could carry a gross impact of more than $4,000 per year per household in some cases.

The details in a memorandum provide new fuel for arguments that New York is doing too much to help save the planet or it is not doing enough and trying to justify doing less. Advocates on both sides of the debate latched onto the memo as evidence of their point.

The New York State Energy Research and Development Authority (NYSERDA) operates at the direction of Gov. Kathy Hochul, a moderate Democrat who has pivoted her focus to affordability as she seeks support for re-election from more liberal downstate and conservative upstate regions.

On Feb. 26, NYSERDA President Doreen Harris sent Hochul’s director of state operations an estimate of near-term costs of implementing a cap-and-invest system to help reach the emissions-reduction mandate of the 2019 Climate Leadership and Community Protection Act (CLCPA). It calculates that by 2031, upstate households burning oil or natural gas and operating two vehicles would see more than $4,100 a year in new costs.

After that detail, the memo notes that cap-and-invest’s affordability benefits for moderate-income New Yorkers would reduce the annual impact to about $2,500, and those who upgrade fossil fuel equipment would be expected to see an even smaller impact, or possibly a net benefit.

It calculates charges of $2.23/gallon of gasoline and comparable charges for other fossil fuels because of carbon emission allowances that would reach nearly $180/ton by 2031 under the cap-and-invest blueprint that was prepared but which Hochul has refused to implement. (See NY Defers Action on Controversial Cap-and-invest.)

The calculations in the Feb. 26 memo were not announced in a news release, but NYSERDA provided the memo to journalists who requested it.

It opened a new chapter in the long-running argument over when and how decarbonization will produce results, and at what cost — a particularly fraught debate as energy prices rise faster than inflation in a state with above-average fuel prices and some of the most expensive electricity in the nation.

Critics pounced on the memo from both sides.

State Sen. Mario Mattera, the ranking Republican on the Senate Energy and Telecommunications Committee, said March 2, “As New Yorkers continue to discover the true cost of Albany Democrats’ energy mandates, which a NYSERDA memo last week clearly outlined, it is time for New York to face reality and help its residents. [The Senate’s Republican minority] has repeatedly raised the alarm that the illogical mandates of the CLCPA are costing New York families and businesses billions.”

But New York League of Conservation Voters President Julie Tighe said the NYSERDA analysis was flawed because it factored in the most aggressive implementation of the program but not the counterbalancing cost controls and consumer rebates, or the health and societal benefits that cleaner air would provide.

She called the memo a negotiating tactic during the contentious talks shaping the state budget due March 31, and said: “Building a green economy and protecting New Yorkers’ wallets are not at odds with each other. New York has both a legal mandate and a moral responsibility to cut pollution, and that is exactly what cap-and-invest will achieve.”

In the memo, Harris said NYSERDA’s estimate is not a worst-case scenario but a conservative one, adding it may be an underestimate because it does not reflect the “hostile and disruptive” actions of the federal government. Beyond that, she said, the acceleration of clean-energy deployment needed to achieve the CLCPA’s goals is infeasible.

Despite highly supportive policy stances by Hochul and her predecessor, Andrew Cuomo (D), New York remains a slow and expensive place to develop energy generation and transmission.

After a decade of development and billions of dollars in public subsidies, New York received only 23.6% of its electricity from renewables in 2024, less than in 2014. (See N.Y. Reports Minimal Increase in Renewable Power.)

Development is expected to get more expensive as Trump administration policies begin to impact renewables. Renewable energy skeptics say it’s time for New York to step back; advocates say it is time for New York to double down; and the governor or her aides say it is time for New York to be flexible with the CLCPA’s timeline and goals.

Drafted a month before the budget deadline and released to the media, the NYSERDA memo could be viewed as what Tighe called it: a step in the bargaining process; an appeal to New Yorkers already worried about their utility bills. (See Electricity Rates are the Political Livewire Threatening the Industry.)

The memo flags several requirements of the CLCPA as expensive and/or difficult to comply with. Among them is Global Warming Potential 20 (GWP20), a mandate to consider the effect of emissions over a 20-year period. That is more stringent and expensive than GWP100, the one-century standard adopted by the Paris Agreement of 2015.

It is one more factor boosting the cost of implementing the CLCPA, which the memo reminds readers was enacted before the COVID-19 pandemic and its supply chain constraints, the return of inflation, increased geopolitical turmoil and the re-election of President Donald Trump.

Hochul unsuccessfully attempted to engineer a switch from GWP20 to GWP100 during budget talks in early 2023, when New York’s renewable pipeline was full and Washington was offering piles of money to support it.

In its December 2025 update to the State Energy Plan, a panel consisting mostly of Hochul appointees took the pragmatic path of preserving the clean energy vision of the CLCPA while also preparing for delays in achieving it. (See N.Y. Embraces All of the Above in Energy Strategy Update.)

The conversation during a five-hour meeting on changes to NYISO’s transmission planning processes became heated at times, as stakeholders challenged ISO officials on exactly how they will develop the possible scenarios they propose to use to determine reliability needs.

The joint meeting of the Installed Capacity Working Group and Transmission Planning Advisory Subcommittee on Feb. 26 was originally budgeted for only three hours, but it took up the entire morning and ran into the afternoon. More than 100 stakeholders joined the meeting by phone.

NYISO has argued that it needs multiple scenarios in its Reliability Planning Process and Short-Term Reliability Process to take uncertain future grid conditions into account. The ISO would identify only needs based on “significant and persistent” violations of reliability criteria across more than one scenario. This would avoid overbuilding the grid as well as prematurely identifying needs, NYISO argues. (See NYISO Seeks to Avoid ‘Flip-flopping’ in Revised Planning Process.)

The ISO is trying to roll out the changes before the next Reliability Needs Assessment, a timeline that requires submitting tariff revisions with FERC by summer.

Under the proposal, NYISO would first review its baseline assumptions and those for scenario development with the Electric System Planning Working Group. After conducting its analyses based on the group’s feedback, the ISO would review the recommended scenarios with the ESPWG and TPAS, initiating a 15-day comment period. The ISO would then issue a draft of the RNA for stakeholder feedback at two additional ESPWG/TPAS meetings.

The final draft RNA would need approval from the Operating and Management committees before going before the Board of Directors.

Chris Casey, an attorney representing the Natural Resources Defense Council, retorted that if the ISO had unlimited discretion to create scenarios, then they could be just as conservative, propagating similar problems across them. He said he did not see any guardrails to prevent this from occurring.

Stu Caplan, representing the New York Transmission Owners, asked about the timing of the meetings, saying he was concerned that there needed to be ample time for stakeholder feedback. He said this was particularly true for transmission owners because of their reliability obligations under state law.

“If there are multiple scenarios where elements from different scenarios contribute to common reliability, but if those elements are not correlated or likely to be coincident, then there’d be a need to provide feedback before the ISO is in a situation where it must rush to get the RNA to the Operating Committee,” Caplan said.

Zach Smith, vice president of system and resource planning, replied that the second feedback meeting was the time for stakeholders to issue support or opposition or comment on specific reliability scenarios.

“Only after weighing all that feedback would we finalize the RNA scenarios for use in the remaining analysis,” Smith said.

Mike Mager, a lawyer from Couch White representing large industrial customers, asked whether there would be a formal vote on the planning scenarios, echoing a request from earlier meetings. Smith said there is not one in the current proposal.

“We’re seeking to create a balance with the … comment period that serves to provide in a very clear and open and transparent matter the feedback everyone would have without taking that one extra step of having a formalized vote that may stand in the way of us conducting this process,” Smith said.

“This stakeholder feedback process is good; it’s absolutely what I expect from NYISO as a bare minimum,” Casey said. “I don’t consider it anywhere near sufficient. I am looking for methodological guardrails that bound scenario development and define and bound ‘significant and persistent.’”

According to its presentation, “in determining the influence of a trend or group of trends on potential scenarios, … NYISO will consider the likelihood that a trend or grouping of trends will occur in the study period; the diversity of scenarios; and the interdependence of the underlying assumptions of the scenarios.”

But multiple stakeholders had concerns about how NYISO develop plausible scenarios.

“On whether NYISO will consider the likelihood [of scenarios], I get that [the proposal] says ‘will,’ but the key word there is actually ‘consider,’” said Michael Lenoff, representing Earthjustice. “So yes, NYISO will consider, but it’s not bound by anything.”

Lenoff said any bounds on NYISO should be in the tariff because the ISO has already included what he called an implausible scenario in its Q3 2025 Short Term Assessment of Reliability report, in which the Champlain Hudson Power Express was assumed to miss its operation date.

“I think it should be that NYISO ‘shall not’ select a scenario as actionable unless it is reasonably plausible, or something like that,” Lenoff said.

A transmission planner with Consolidated Edison also noted the CHPE assumption as evidence of the need for binding rules on NYISO in the process.

Doreen Saia, a lawyer representing generation interests, said she was concerned about setting too many parameters in the tariff because it could create inflexibility. She said the current issues, such as large loads from data centers and political instability, would not have been predicted a decade ago. She urged the ISO to try to capture this in the manuals, which are easier to change than the tariff.

Saia also pointed out that the current process provides for stakeholder “discussion and action” at the MC and OC but that approval is not required. The ISO could produce a similar mechanism where stakeholders vote to indicate where they land on different scenarios. This would give the board a sense of how comfortable market participants were with the process, she said.

“It’s not perfect, but at least it provides a little more grounding on what can go forward,” Sai said. “At the end of the day, even the current tariff does not have a provision that allows market participants to stop an RNA in its tracks.”

Tony Abate, representing the New York Power Authority, said he wasn’t sure how productive it was to get so stuck on the wording of the tariff without considering whether the process is actually sufficient to meet reliability needs.

“We need some time to go through this,” Abate said. “The TOs are still thinking this through. There’s some serious technical considerations.”

“I just want to understand why there is seemingly more concern about … using conservative assumptions in the base case than using multiple scenarios,” Casey said. “I am lost by NYISO maintaining the base case as it is now and then creating as many scenarios as it wants with pretty unlimited discretion. Doesn’t that pose the exact problem you’re articulating?”

“That’s exactly the reason why we put in a lot of thought about how to build scenarios and how to take into account reliability needs,” said Yachi Lin, NYISO director of system planning.

FERC has approved NorthWestern’s acquisition of Puget Sound Energy’s shares in the coal-fired Colstrip power plant in Montana and authorized NorthWestern to sell electricity produced by the plant.

FERC issued two orders Feb. 27 related to the company’s acquisition of shares in Colstrip (ER26-129 and ER26-411). Both orders concern NorthWestern’s subsidiary NorthWestern Colstrip, which was created to hold ownership in the coal-fired generation asset, according to FERC.

In the first order, FERC accepted NorthWestern’s cost-based rate (CBR) tariff for short-term sales of electricity produced by its share of the plant. In the second order, the commission approved a power purchase and sale agreement between NorthWestern and Mercuria Energy America.

FERC said both filings were “just and reasonable and not unduly discriminatory or preferential.” The orders are effective Jan. 1, 2026.

NorthWestern reached an agreement in 2024 to acquire PSE’s 370-MW stake in two units of the Colstrip power plant effective Jan. 1, 2026. The deal came about after PSE was forced to exit the plant because of Washington state law.

NorthWestern also has acquired Avista’s 222-MW share in the plant, giving the company 55% ownership, according to NorthWestern’s website.

The transaction received backlash from Montana Public Service Commissioners and the Montana Environmental Information Center. The opponents argued in filings with FERC that NorthWestern failed to receive authorization for the agreement under Section 203 of the Federal Power Act.

The opponents said there is a risk that “generation from the Colstrip station will be contracted to a large load customer and will not benefit the people and small businesses of Montana,” according to the orders.

FERC rejected those arguments, saying the FPA requires prior authorization only for transactions valued at more than $10 million.

NorthWestern acquired PSE’s shares in the power plant “at a transaction price of $0. Therefore, this transfer is under the $10 million threshold required for commission jurisdiction under Section 203,” the orders stated.

Montana Gov. Greg Gianforte (R) supported the deal, saying the plant is “essential” to “maintaining reliability during winter conditions, stabilizing the regional grid and keeping energy affordable for Montana families, farmers and employers,” according to the orders.

According to the CBR filing, NorthWestern is negotiating various deals and made the filing to ensure it has the authority to make any short-term sales while committing to filing any long-term sale agreements with the commission.

FERC accepted NorthWestern’s proposed maximum demand charges under the CBR:

$11,920/MW-month

$2,750/MW-week

$390/MW-day

$16.30/MWh

The order states that all services agreements should be governed under the terms and conditions of the Western Systems Power Pool agreement.

Meanwhile, NorthWestern’s agreement with Mercuria Energy provides for the sale of long-term capacity and energy from the power plant. NorthWestern is responsible for all “interconnection and transmission arrangements, electric losses and necessary costs to deliver energy, capacity and ancillary services to the point of delivery,” according to the order.

FERC found the agreement’s proposed capacity and energy rates “just and reasonable” because they fall below the ceiling demand charge in the associated CBR tariff, the order stated.

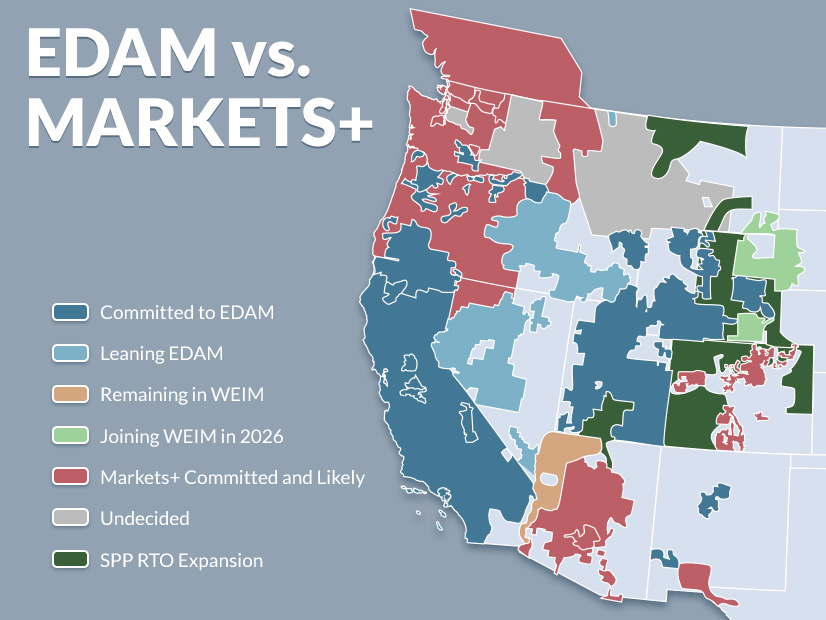

BOULDER, Colo. — Conversations remained cordial despite the ongoing competition between CAISO and SPP in the West as the RTOs’ top executives took the stage at Yes Energy’s annual EMPOWER conference.

RTO Insider’s Robert Mullin moderated a panel in which Elliot Mainzer of CAISO and Lanny Nickell of SPP emphasized the importance of cooperation and friendly competition while making their pitches for their respective Western markets.

CAISO is preparing to launch its Extended Day-Ahead Market (EDAM) in May, while SPP plans to roll out Markets+ — which includes day-ahead and real-time market components — in October 2027.

Over the past few years, the competing markets have fought to sign up participants across the West. CAISO plans to go live with EDAM in May with the participation of PacifiCorp, with Portland General Electric to join in the fall. SPP also has several major commitments, headlined by the Bonneville Power Administration’s decision in May 2025 to join Markets+. (See BPA Chooses Markets+ over EDAM.)

Mainzer clearly was disappointed with BPA’s choice. He was BPA administrator and had worked there for 18 years before moving to CAISO in 2020.

Regardless of the choices of individual entities, CAISO and SPP “continue to motivate each other to get better,” Nickell said. “If one of us goes away, the motivation to improve isn’t as great.”

Mainzer and Nickell emphasized those potential cost savings associated with the adoption of day-ahead markets in the West.

Mainzer said the success of the Western Energy Imbalance Market (WEIM), launched by CAISO in 2014, gave participants confidence in the possibilities of regionwide markets.

“Now we’re seeing this second chapter,” he said, with participants realizing “we’re leaving money on the table now in the day-ahead.”

In SPP’s eastern RTO territory, Nickell said the wholesale markets provided about $10 billion in adjusted production cost savings over the past five years.

The launch of organized day-ahead markets in the West will “allow the provision of energy in a much more affordable way because we will have access to resources across a much broader region, and we’ll be able to commit those on a day-ahead basis, which will ensure a much higher degree of reliability,” he added.

The CEOs’ perspectives differed regarding potential issues associated with the seams between the market areas, reflecting ongoing debates about the benefits of the two markets.

“When you look at that map and look at the Swiss cheese that’s opening up in the West, that’s going to be challenging to deal with,” Mainzer said. While seams agreements can help mitigate issues, seamless market footprints provide the greatest reliability value, he added. (See FERC Report Urges West to Address Looming Market Seams Issues.)

As the lines between markets harden, “I don’t think any seams agreement or combination of seams agreements is going to be able to fully restore the loss of efficiency that we’re going to get from breaking apart [WEIM] and having multiple market operators,” he said. “We’ll work hard to do it, but it is a point of departure.”

Nickell expressed more optimism about the potential for productive seams agreements and said the only way to truly eliminate all seams is through the creation of a regionwide RTO.

“Seams exist all over the West today, and they’re still going to exist … there’s still going to be balancing authorities, there’s still going to be transmission owners and providers operating their own tariffs,” he said. “We’re simply operating markets.”

“Our job is to work together to try to optimize the exchange of energy, not only within the market but across the two markets,” he added. “I think we can optimize those seams in a way that assures that energy is produced, it’s accessed and it’s delivered in a much more reliable way.”

Governance Structures

Trust in SPP’s governance structure has been a key factor for entities deciding to join Markets+, Nickell said. BPA cited governance as a key qualitative factor in its decision to join Markets+.

Nickell emphasized the importance of developing long-term trust with stakeholders, saying trust is “hard to get and it’s easy to lose, and we’ll do everything we have to maintain that trust that our participants have with us.”

“We’ve operated a highly engaged stakeholder process for decades,” he said. “We’re experienced in doing that, and I think a lot of the Western participants and stakeholders saw that and found it attractive.”

Mainzer said participants joining EDAM have been motivated primarily by economic considerations.

“We’ve tried to really build on the platform of physics and economics… and continue evolving the governance,” he said.

In an effort to address concerns about the influence of California policymakers on EDAM, the state passed legislation in the fall enabling the creation of an independent regional organization to govern WEIM and EDAM. (See Newsom Signs Calif. Pathways Bill into Law.)

When he was CEO of BPA, Mainzer said he knew “as well as anybody” the governance concerns about CAISO’s markets.

“The governance structure for [CAISO] for many years was just not a sustainable structure for true multi-state participation,” he said. “That’s why we spent five years working to get that law passed last year.”

“You’ve done great work — I think it’s awesome that you were able to get those governance reforms in place,” Nickell said to Mainzer.

Asked whether the ultimate goal of Markets+ is to expand SPP’s western RTO footprint, Nickell said it’s possible SPP will continue to expand its RTO operations in the West but emphasized that “you can’t force somebody into an RTO — that’s a voluntary construct.”

“It takes time and it takes people getting comfortable with that approach,” he said.

SPP’s western RTO expansion is to take effect April 1 when it incorporates utilities in Arizona, Colorado, Utah and Wyoming.

Mainzer framed the developments in the West as a process of natural evolution that started with the implementation of real-time markets and has moved gradually toward the addition of components that can add value for the region.

“I think both our constituencies have tended to prefer this matchbox slogan of ‘evolution, not revolution,’” he said, adding that the West can benefit from best practices and lessons learned from existing markets across the country.

He emphasized the importance of maintaining local responsibility for resource adequacy planning and generation development as the markets grow.

“You are going to see a ton of change and continued evolution, but we get the chance to do it with steps and features that we think really produce value with less downside,” he said.

U.S. Sens. Peter Welch (D-Vt.) and Dave McCormick (R-Pa.) have introduced the Reconductoring Existing Wires for Infrastructure Reliability and Expansion (REWIRE) Act, which aims to accelerate the deployment of advanced transmission technologies.

The bipartisan bill comes as Congress is working on permitting legislation. It seeks to streamline environmental reviews for projects like reconductoring or installing grid-enhancing technologies (GETs) on existing rights of way.

“We’re up against the clock when it comes to meeting America’s growing energy needs,” Welch said in a statement March 2. “Increasing the capacity of the grid by accelerating the permitting process and incentivizing practices like reconductoring will not only allow us to connect new and affordable clean energy to the grid — it’ll also save consumers money.”

Demand is projected to rise by as much as 5.7% by 2030. This requires about 5,000 miles of new, high-capacity transmission lines each year, but in 2024 the country saw only 322 miles constructed, the senators’ offices said.

“Electricity demand in Pennsylvania and across America is rising rapidly, and that requires innovative solutions to strengthen our electric grid and cut through the bureaucracy that’s holding us back,” McCormick said in a statement. “The bipartisan REWIRE Act is exactly the kind of common-sense fix we need by using the infrastructure we already have, bringing down costs and stopping years of unnecessary permitting delays from standing in the way of real progress.”

The REWIRE Act would encourage upgrading existing transmission with advanced conductors that can double the capacity of existing transmission lines, which is far cheaper and quicker than building new lines from scratch.

The bill would create a categorical exclusion from the National Environmental Policy Act for projects that increase grid capacity within existing rights of way such as reconductoring, GETs or deploying energy storage.

It would direct FERC to improve the return on equity for reconductoring projects to encourage wider adoption of advanced transmission conductors. The bill would allow state energy offices to use federal funds from the Department of Energy to conduct feasibility studies for reconductoring and GETs projects.

The bill proposes regional collaboratives between DOE, national laboratories and universities to evaluate grid performance and identify good opportunities for deploying advanced transmission. DOE would be authorized to create a national clearinghouse of advanced transmission applications, case studies and best practices to spread the information nationally.

The REWIRE Act has a lengthy list of supporters including American Clean Power, American Council on Renewable Energy, Bipartisan Policy Center Action, Conservative Energy Network, CTC Global, Electricity Consumers Resource Council, EQT Corporation, Grid Action, GridWise Alliance, National Electrical Manufacturers Association, PPL Corporation, the Solar Energy Industries Association and others.

“The REWIRE Act is a smart, bipartisan step to unlock more capacity from the grid we already have,” Grid Action Director Christina Hayes said in a statement. “Reconductoring and advanced transmission technologies can deliver meaningful reliability gains and additional transfer capability faster and more cost-effectively by working within existing rights of way.”

The demand growth the industry is facing requires both the kind of near-term upgrades that would be encouraged by the bill, along with a buildout of completely new transmission, she added.

“The REWIRE Actis exactly the kind of pragmatic, bipartisan policy needed to unlock grid capacity quickly and affordably,” CTC Global Chief Policy Officer Theodore Paradise said in a statement. “By accelerating reconductoring with advanced conductors in existing rights of way, the bill lowers costs, strengthens reliability and delivers meaningful transmission capacity on timelines the grid urgently needs.”

When it comes to the grid, can artificial intelligence be two things at once? Demand planners and climate realists see AI as the bad guy, driving up demand and grinding decarbonization goals into the ground. Yet industry leaders and techno-optimists believe it can be the good guy.

I met with some of Silicon Valley’s biggest brains recently to unpack this complex question — and, critically, whether AI can be the good guy while meeting FERC-approved NERC Critical Infrastructure Protection (CIP) standards.

There’s no doubt AI could be exponentially faster, smarter, more innovative and more efficient than the current workforce, but can it be reliable? We’ve all heard of AI hallucination in everything from government reports to research papers, but when you are dealing with HVDC, errors can have life-and-death consequences.

If the industry does not quickly define “reliable AI” and build guardrails around its deployment, we risk importing stochastic behavior into systems designed for determinism.

That is not a technology debate. It is a reliability and safety debate. And it is one RTOs, regulators, grid and power plant operators, and utilities cannot afford to postpone.

The AI-Enabled Vision for the Future Grid

Dej Knuckey |

AI can optimize transmission and distribution, move more electrons through the same wires, free workers from mundane tasks, and manage preemptive maintenance. And there are ways it can help the grid that we are only beginning to imagine.

One of the most interesting use cases is building photorealistic digital twins of nuclear power plants and substations to enable remote operations and maintenance, which I’ll dig into more later.

Another application involves drones analyzing snow-cloaked power lines without waiting for a winter storm to provide the training environment. AI not only creates images of the storm-that-doesn’t-exist but also teaches the system what to look for in the white-on-white, post-storm landscape from all the angles an experienced drone pilot would use. The goal: eliminate the need to wait until roads are accessible before lines can be inspected. Grid operators will be able to keep drones in habs (the boxes drones call home) near HVDC towers so they can deploy after storms and for regular maintenance.

There also are ways to make AI less power-hungry, at least in an electron sense. AI may still want to rule over its human underlings but can do so more efficiently with better data compression.

Why AI Sometimes Gets it Wrong

AI is ubiquitous: You can’t do a simple web search without an AI-generated summary popping up. Sometimes it’s great. Other times it’s amusingly wrong.

“When I ask it to search the web, nine out of 10 times it gets the right source with the right quote. But 10%, I go to the link that it showed, and it doesn’t exist,” said Yuriy Yuzifovich, chief technology officer of enterprise AI at GlobalLogic, while referring to a popular AI assistant.

Users refer to AI errors as hallucinations. When I was using early versions of ChatGPT to research technical topics, rather than admit “I can’t find any sources for that,” the eager-to-please AI would sometimes invent research papers. If I’m searching for sources for an RTO Insider article, that hallucination is an annoyance. I correct it and move on.

And here’s the part that’s poorly understood in the public conversation: The large language models (LLMs) that power consumer AI tools are built to behave this way. They are intentionally probabilistic.

Hallucinations and HVDC Don’t Mix

You have to go inside LLMs to understand how and why it can deliver errors with such confidence.

LLMs “understand” the world with tokens and vectors. Tokens break language down into small chunks that AI models read, while vectors represent those tokens in a numerical, high-dimensional way that give each token context and relationships with similar tokens. If “All-Bran” were a token, its vector would tell you it’s in aisle 5 on the third shelf with all the other cereals. AI constructs answers to questions by stringing together a series of tokens it has found using vectors.

Continuing to use a three-dimensional analogy to simplify the multidimensional space that AI operates in, imagine AI is doing your shopping. It enters the supermarket, looking where the vector has directed it. At the third shelf of aisle 5, it grabs the closest box of cereal with bran in its name. Because it is closer than the proper target and similar enough, the model assumes it’s right and stops looking.

As it gives you bran flakes, it hasn’t made a wild guess, but it has delivered something any fan of All-Bran (yes, they exist) would consider wildly, soggily wrong.

“The randomness of the answer is built in. It’s a feature. It’s not a bug,” Yuzifovich said.

In some cases, such as writing a conference presentation, that randomness can look like creativity. But the stakes are higher in the electricity sector. The grid, especially the HVDC side, operates with life-and-death stakes. If AI was advising one of your control room operators during a switching event, or guiding a field crew during storm restoration, that “nine out of 10 times” isn’t innovation. It’s an unacceptable risk.

Does this mean there’s no space for AI in managing critical infrastructure? The problem is most public discourse treats “AI” as a monolithic technology. It isn’t. And if regulators and operators fail to draw sharper distinctions, we risk regulating the wrong thing while deploying tools that introduce the instability we work hard to eliminate.

When ‘Good Enough’ AI Isn’t Close to Good Enough

Utilities have been pitched an avalanche of AI solutions over the past few years: copilots for engineers, chatbot overlays for procedures, systems that promise to answer questions from internal manuals.

On slides, it looks compelling, but in practice, the results have been uneven.

“Most of these organizations love the idea that you’re going to do something with their data and get some magic beans of intelligence back,” Malcolm Hay, GlobalLogic’s vice president of energy, said. “There have been a lot of proof of concepts done that are kind of ‘meh.’ They deliver a bit,” he said, but are not accurate enough to be relied on in operational settings that can’t tolerate any kind of ambiguity. “Any hallucinations … would destroy confidence and obviously [pose] security and safety risks.”

Retrieval-augmented generation (RAG) is a perfect example of this gap between promise and performance. Instead of letting a model roam the internet, you point it at curated internal documents. The failure mode, however, is often indistinguishable.

“RAG is similar to ChatGPT, but instead of the internet, you give your documents,” Yuzifovich said. “The results are very similar: most of the time it gets it right, but sometimes it doesn’t — and when it doesn’t, you don’t know when.”

That last clause is the operational killer. If a human has to verify every output, the efficiency case collapses.

Meanwhile, workforce pressures are intensifying. During one storm restoration workshop, a utility described line workers running 16-hour shifts after a major event. “We need to really help them and give them the tools they need to support us,” said Carlos Elena-Lenz, vice president for digital enablement and transformation at Hitachi Energy.

Those tools cannot be probabilistic guessers.

What ‘Reliable AI’ Actually Means

In the aerospace world, craft or launch vehicles that carry people are called “human-rated” in contrast to vehicles that carry a non-human payload. They are designed to a higher standard because their failure has more significant consequences. It’s a concept that easily translates to the energy world. Every day, crews work with a complex system that, if mishandled, could have fatal consequences.

In safety-critical environments, the definition of AI success is radically different from Silicon Valley’s definition.

Four requirements for “Reliable AI” surfaced repeatedly in my conversations.

1. Deterministic, not Stochastic

If you ask the same question under the same conditions, you have to get the same answer every time. “It’s very important to show … on a small subset … that no matter how many times you’re asking the same question, it’s the same answer,” Yuzifovich said. Variability is intolerable in a control room.

2. Grounded in Structured Knowledge

The foundation of reliable AI is not linguistic fluency; it is structured domain knowledge. “Knowledge is just a collection of interconnected knowledge: This fact is related to this fact,” Yuzifovich said. “With LLMs, we can finally produce enormous amounts of this knowledge as code.”

This is not “upload your PDFs and hope.” It requires iterative extraction, validation and SME oversight, and multiple passes of extraction with a human in the loop to codify critical rules.

3. Able to Say ‘I Don’t Know’

Safety-critical systems must value accuracy over giving an answer. It needs to know when it doesn’t know and never guess. In other words, we want a Hal that will say, “I’m sorry, Dave. I’m afraid I can’t do that.” An “I don’t know” state is not weakness. It is governance.

4. Traceable and Auditable

When an AI suggests an action, operators must see the chain of reasoning and trace back as far as needed, even if it means going back to the source documents that contain the standard operating procedures. Mainstream AI models often are opaque by design, but grid-grade AI must be engineered for auditability. The system must behave like a senior engineer, not just a librarian. It must be grounded in rules, not merely fluent in text.

Building the World of Truth

As part of the nation’s critical infrastructure, utilities, power plant owners and grid operators must isolate their data systems from external sources to ensure cybersecurity. That means even if some of the data exists on the web, it’s not accessed there. For example, the installation and commissioning manual for a transformer may exist on the manufacturer’s website, but it will need to be replicated inside a secure system for internal use.

To create “knowledge as code,” everything gets uploaded, Renan Giovanini, chief technology officer of energy business at GlobalLogic, said. And by everything, he means everything: the original RFQ with specs, the operations manuals of every component, the history of faults and repairs.

For a greenfield plant, that’s probably already digitized and easily uploaded. However, for a 70-year-old substation with transformers as old as the average worker, creating the knowledge base requires sifting through warehouses of records and digitizing the handwritten notes of electricians who have serviced the plant over the years.

The sheer magnitude of the task may seem overwhelming and industry players will need to believe there will be a real return on that investment. The challenge for technology providers will be to help customers make the case for the long-term benefits the considerable investment will deliver.

From Chatbots to Operational Systems

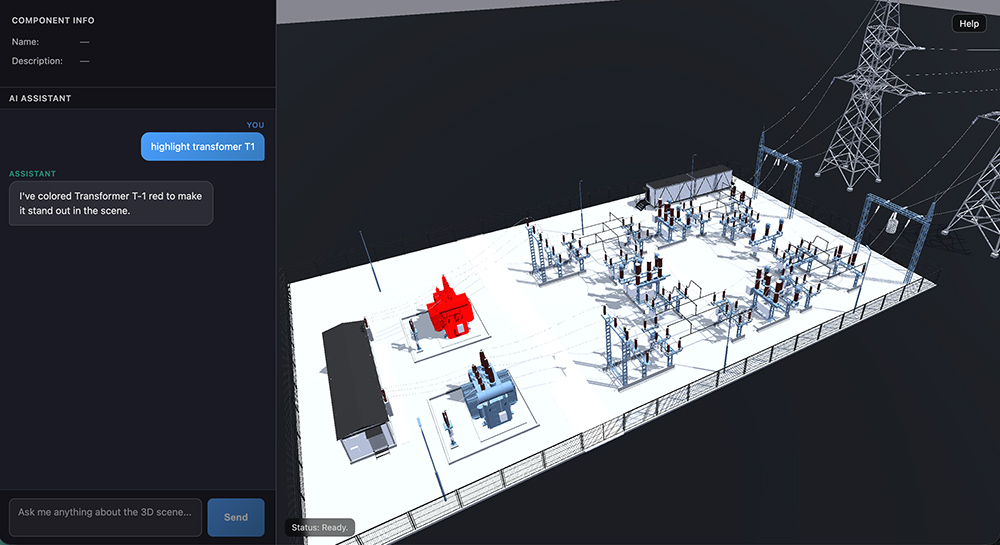

The public narrative around AI remains chatbot-centric. Inside utilities and OEM environments, the picture looks very different. In one nuclear maintenance platform demonstration, a GlobalLogic project that is live today, engineers built a detailed digital twin tied directly to procedures and asset data.

“The customer wanted to have a solution to better coordinate their maintenance teams, so they could remotely get together and plan for work,” Giovanini said. “They had team members across the globe, that, in the past, would go to a [Microsoft] Teams meeting.” The challenge would come as soon as people on the call needed the position of a particular piece of equipment or access to a user guide. “We worked with them to create a digital twin representation of the nuclear power plant and enrich it with many different data sets, user guides, maintenance procedures and so forth.”

The representation replicates the plant’s facilities in an immersive metaverse, enabling remote access, real-time collaboration and AI-powered operations management. The visual layer is important, but the real innovation is underneath: structured rule enforcement tied to plant documentation.

A digital twin of a nuclear power plant (right) is a realistic representation of the real thing (left) layered with manuals, data and other intelligence. | GlobalLogic

In a demonstration of a substation digital twin under development, those structured rules became concrete: an operator instructed the AI to open a disconnector. The system refused.

“I cannot open this disconnector because there is a circuit breaker that must be opened first,” it replied.

The rule was not manually coded by a software engineer.

“What we take is a standard operating procedure from the utility that gets ingested by a knowledge database. There is no need now for a software engineer to transform that into rules,” Giovanini said.

It enables procedural enforcement at machine speed.

In storm response, similar pipelines are emerging, as in the example of the inspection drones. “We started using synthetic data generation to create snowy scenes and we’re feeding them into our computer vision model,” Elena-Lenz said.

Beyond having a fleet of drones that can inspect and report on damage, the sensing-to-decision architecture should be able to collate the damage reports, prioritize them, and then feed into a workforce management platform that can assign the work based on the crew’s locations, tools and capacity, he said.

Remote teams can interact with a digital representation of a substation using natural language questions. | GlobalLogic

The Human Knowledge Emergency

The most urgent case for reliable AI is not automation. It is retention. The industry is facing a crisis as the generation that holds deep experience retires.

“We’re losing this context for these old systems,” Giovanini said. “By capturing this knowledge into a digital format, that tribal knowledge now will be part of this utility or company knowledge space.”

Another engineer described veterans who can diagnose issues by sound alone. “They can go out to a substation and just by listening tell you if everything is working. You can’t create software that beats decades of knowledge.” Yet the industry must capture as much of that knowledge as it can before it loses that experience, and possibly train systems in ways no one planned, such as audio detection of certain fault types.

Reliable AI, in this context, becomes a continuity strategy, embedding institutional memory into auditable systems.

Planning for an AI-enabled Future

By the end of a dozen conversations and demonstrations, I’d laid my dun-colored climate realist glasses to one side and donned a techno-optimist’s hat. AI data centers’ demand may create a challenge for the grid, one that will put emissions reduction goals on the back burner in a way that I find hard to stomach, but that doesn’t mean the industry won’t also benefit from it.

The select few examples of how AI can multiply human capabilities and preserve human experience for generations to come barely scratch the surface. There are many ways AI can help the industry become faster, smarter, safer and more responsive at getting more out of existing assets.

But regulators and industry leaders need to ensure the industry maintains the highest standards in this rapidly evolving digital world.

“Reliable AI” guardrails are essential, not only to meet NERC’s CIP requirements, but to also continue protecting the grid and the people who work on it and live near it in the conservative, risk-averse way the industry holds as sacred.

Power Play Columnist Dej Knuckey is a climate and energy writer with decades of industry experience.

MISO said its modeling estimates show it could have 413 to 501 GW of installed capacity on its system by 2045.

The grid operator is nearing its final four futures scenarios, which estimate the system makeup 20 years down the road for transmission planning purposes. The nearly final estimates are higher than MISO’s prior draft release. (See MISO Draft Tx Planning Futures Envision 400-GW Supply or More by 2045.)

Across all futures, MISO shows that solar, natural gas and wind resources would jockey for lead fuel type:

MISO’s low-end estimate of 413 GW includes 32% solar, 26% gas and 21% wind. However, it only expects to use gas 14% of the time and lean on wind and solar 28 and 27% of the time, respectively.

The middle-of-the-road future has a 437-GW fleet at 28% gas, 26% wind and 23% solar. Gas would supply output 13% of the time, with solar at 17% and wind at 36%.

The third future, which allows for the fastest fleet transition, contains 501 GW split among 27% wind, 27% gas and 24% solar. In that scenario, gas generation is dispatched 10% of the time, with solar at 18% and wind 36%.

Finally, MISO’s supply chain-constrained scenario has a 455-GW fleet by 2045, at 30% solar, 28% gas and 20% wind. Gas and solar are used equally, 23% of the time, while wind is responsible for 28%.

In all four cases, battery storage remains at 4% of the mix. “Other” generation (oil, conventional hydro, biomass, geothermal and other resource types) takes a 10% slice in nearly all futures.

The most aggressive, 500-GW future contemplates an 8% share of nuclear power that supplies 25% of output – the highest MISO foresaw. Meanwhile, coal ranges between 4% (the supply constrained future) and 1% (the aggressive fleet change future) and mostly runs 1% of the time.

MISO said its resource mixes were shaped by planning reserve margin requirements and states’ carbon-reduction and renewable energy goals.

Members have 171 GW planned by 2045. Natural gas and solar take the largest share at 53 and 50 GW, respectively. Members also plan to add 30 GW of the “other” generation, 24 GW of wind, 12 GW of battery storage and 3 GW of nuclear.

MISO currently has 202 GW of installed capacity.

The RTO plans to finalize its 20-year transmission planning scenarios early in the second quarter of 2026; it will host a final stakeholder workshop April 9.

At a Feb. 26 workshop webinar to discuss the futures, MISO Policy Planner Logan Pollander said all four futures are resource adequate. He said the RTO’s loss-of-load expectation analysis exhibited no expected unserved energy in each of the selected study years (2030, 2035 and 2045).

The modeling doesn’t include a finalized capacity accreditation method for energy storage. Multiple stakeholders said MISO was missing a large piece of the puzzle if it didn’t decide accreditation values for storage.

Pollander said the results could change once MISO factors in storage accreditation.

Red States Ask for Comparison Model Free of Clean Energy Goals

Bill Booth, a consultant to the Mississippi Public Service Commission, asked MISO to create a purely economic expansion future that doesn’t consider any carbon goals in order to see how much transmission might be built for the purposes of decarbonization.

MISO Executive Director of Transmission Planning Laura Rauch said the RTO is not comfortable with scenarios that diverge from enacted carbon-reduction laws and the goals of members.

South Dakota Public Utilities Commission staffer Darren Kearney said he would like to see a “counterfactual” of what the buildout would be without the constraints of carbon abatement, so states with carbon-reduction goals don’t pass on their costs to those without them.

Rauch said MISO could have a discussion on that once new transmission is proposed.

But the Union of Concerned Scientists’ Sam Gomberg cautioned the RTO against singling out renewable energy goals to make some states’ cost allocation smaller.

“In each state you can find biases and preferences … written in state code that drive resource adequacy decision-making outside the bounds of least-cost planning,” Gomberg said.

For example, he said, if states restrict or shut out cost-effective solar or wind generation when their political climate is suited for it, that’s putting their thumb on the scale. “We could go in countless directions here … and find ourselves in a death spiral of paralysis by analysis,” Gomberg said.

According to MISO, just 3% of its load base is not associated with any carbon-reduction goals.

The Independent Market Monitor has been in discussions with MISO about introducing a sensitivity that reflects a maximum willingness to pay for carbon reductions. IMM David Patton has said the RTO should “balance cost objectives with carbon objectives” in the futures.

At previous futures workshops, Patton has said it’s worthwhile to examine the point at which members wouldn’t invest in a new clean energy technology because it would lose money or “produce retail rates that are astronomical.”

Representing MISO industrial customers, Kavita Maini said she had a hard time believing states would reason that “even if this standard costs a million-bajillion dollars, I still want to pursue this” when rates become unaffordable.

WEC Energy Group’s Chris Plante said he struggled with how MISO could assume no expected unserved energy from its modeling. “I don’t think that’s even possible based on the probabilities,” he said.

“It’s below the criterion. It doesn’t mean there’s no expected unserved energy. It just doesn’t exceed the one-day-in-10-years” standard, said RaeLynn Asah, MISO senior manager of regulatory and policy planning.

Plante argued the RTO can meet the loss-of-load criteria but still experience unserved energy. He said they are two separate concepts.

Asah clarified there was no significant unserved energy, not a complete lack of unserved energy.

MISO’s modeling does not factor in deliverability or transmission constraints.

Booth said it would behoove the RTO to consider transmission so it doesn’t rely on generation that’s situated in MISO South that might not be deliverable to the Midwest. He said its resource-adequate assumption is flawed without deliverability considerations.

Asah said MISO would consider deliverability when it sites its generation totals across the footprint. MISO’s Neil Shah added the method is in line with how the RTO conducts its loss-of-load expectation studies.

“How do you not consider whether these resources are actually deliverable?” Booth asked.

Shah said deliverability is handled in subsequent steps and said MISO doesn’t account for transmission constraints in its first step.