California Public Utilities Commission President Alice Reynolds is leaving the CPUC and joining CAISO’s Board of Governors after more than four years at the helm of the state’s utility regulator.

Gov. Gavin Newsom (D) appointed CPUC Commissioner John Reynolds (no relation to Alice Reynolds) to the top spot at the agency.

John Reynolds will “build on” Newsom’s effort to lower utility bills, ensure that wildfire safety spending delivers real value, and hold utilities accountable for safe, reliable and affordable service, the governor’s office said in a Feb. 18 news release.

Newsom appointed Alice Reynolds as CPUC president in 2021 following on her role as senior adviser on energy for his office from 2019 to 2021. She previously was senior adviser for climate, energy and the environment for the office of Gov. Jerry Brown (D) from 2017 to 2019.

“It has been the honor of a lifetime to serve the people of California as the president of the Public Utilities Commission,” Alice Reynolds said in the release. “I look forward to continuing to carry out the vision of a safe, clean, reliable, affordable electricity system that benefits all Californians, and I leave knowing that the commission is in good hands.”

Alice Reynolds plans to leave the CPUC in late February to join the CAISO board.

Electricity markets in the West are “very fragmented,” she said to the lawmakers at the time. “So, this effort is really thinking about the benefits of a larger market, meaning, think about a market with a footprint that is larger than any one weather event.”

Energy Affordability Highlighted Again

Front and center at the CPUC is energy affordability.

John Reynolds will lead the effort to align infrastructure investments with affordability goals, and ensure utilities deliver results for ratepayers — without slowing California’s clean energy progress, Newsom’s office said in the release.

His appointment “underscores a renewed focus on cutting costs and improving performance as extreme heat, wildfire risk, and upgrades to the electric grid drive new demands on the system,” Newsom’s office said.

“I look forward to continuing the state’s work to drive towards more affordable utility services while supporting safe and reliable infrastructure that delivers on our ambitious climate agenda,” John Reynolds said.

Christine Harada will join the CPUC as a commissioner. Harada is undersecretary of the California Government Operations Agency and previously was senior adviser at the U.S. Office of Management and Budget from 2023 to 2025.

FERC approved four transmission security agreements between Exelon’s Commonwealth Edison and new data center customers in Illinois, laying out conditions for their transmission service.

All four orders, issued Feb. 17, included two identical concurrences: one from Commissioner Judy Chang, and a joint concurrence from FERC Chair Laura Swett and Commissioner David LaCerte apparently in response to Chang’s.

The customers include Karis Critical, for a data center in DeKalb (ER26-853); Aligned Data Centers, for a facility in Coal City (ER26-838); Monarch Rock Air, for a facility in Rockford (ER26-839); and Red Energy Partners, for a data center in DeKalb (ER26-841).

The deals all cover the terms of ComEd’s provision of retail service to the data centers; they had to be submitted to FERC for approval because they include the construction and operation of transmission facilities. They include provisions seeking to ensure the data centers pay for those investments even if their development is delayed; they use less power than planned; or they shut down earlier than expected.

FERC approved the proposal under the Mobile-Sierra public interest standard of review, which holds that the terms of arms-length contract negotiations are presumed just and reasonable, absent a showing they are contrary to the public interest.

The entire commission agreed that the deals offer protections for other customers that would not otherwise exist and that the Illinois Commerce Commission can use its authority to place additional conditions protecting other retail customers.

But in her concurrence, Chang noted that using Mobile-Sierra means FERC has not independently assessed the deals against its just-and-reasonable standard. She referenced her concurrence on a similar deal FERC approved for another Exelon subsidiary, PECO Energy, in November. (See FERC Approves PECO-Amazon Transmission Agreement for Pa. Data Center.)

“I write separately to reinforce my concern that reliance on bilaterally negotiated agreements, particularly ones shielded from meaningful commission review by the Mobile-Sierra presumption, may not be sufficient to ensure that customers are protected against unjust cost shifts from new large loads,” Chang said.

The commitments are better than not having an agreement, Chang acknowledged, and they reflect a meaningful revenue contribution to transmission costs that other customers would otherwise have to pay.

“However, there is a need to protect other customers from potential unjustified cost shifts, and neither the terms of the agreement nor ComEd demonstrate how these commitments achieve that higher and more essential standard,” Chang said. “So, while the commission properly accepts the agreement under the Mobile-Sierra framework, that acceptance does not necessarily protect other customers.”

When utilities must expand their transmission systems to offer new service, it can lead to an increase in rolled-in embedded cost rates. To protect wholesale customers, FERC allows transmission providers to charge the higher of the rolled-in embedded cost of the expanded system, or the incremental costs of the expansion itself, but not the sum of the two.

“Today’s order conforms to this line of precedent by acknowledging ComEd’s intention to seek rolled-in rate treatment to recover the costs of serving these new customers,” Swett and LaCerte wrote. “The commission will always reject a rate that seriously harms the consuming public.”

In the PECO concurrence, Chang suggested that FERC could apply “the higher” policy to large loads interconnecting directly to the grid. But that would first require the incremental costs of the upgrades to be quantified, “an exercise that notably has not been conducted and reflected in” the four ComEd agreements, she wrote.

“In fact, the agreement does not identify any specific upgrades needed to interconnect the data center,” Chang said. “Instead, it contemplates that, if the large load that materializes through this agreement triggers transmission upgrades on ComEd’s system, the costs of those system upgrades would be added to ComEd’s transmission revenue requirements and thereby rolled into transmission rates that all customers pay.”

That doesn’t necessarily mean rates for other customers will rise, she noted, but they certainly could.

“The commission and our state counterparts must not let the commission’s acceptance of the agreement and others like it dissuade us from taking additional action to protect customers where we think it is necessary,” Chang said. “Instead, absent some demonstration that the agreement and similar arrangements provide the necessary level of consumer protection, they should be treated simply as one piece of a broader package of federal and state measures to protect customers, rather than the primary or exclusive means to do so.”

For FERC’s part, Chang suggested assessing how to develop customer protection frameworks that can complement and supplement ongoing efforts at the state level.

Swett and LaCerte noted that Mobile-Sierra is just a presumption that presents a higher legal bar to overturning contracts, but that can be done if one “seriously harms the public interest.”

“The Mobile-Sierra presumption is not a straw man behind which the commission hides to evade its statutory duty of ensuring that the American consumer pays just and reasonable rates,” they wrote.

If the circumstances demonstrate serious harm to the public interest, especially other ratepayers, then FERC has a statutory responsibility to act, which could include overcoming the Mobile-Sierra presumptions.

“As we head down the road where it appears that agreements similar to those approved today may become more common, we also would like to clarify that the commission’s existing transmission policy ‘endorses transmission pricing flexibility,’ not a linear analysis,” they said.

NERC’s Standards Committee members had many questions about organizational changes that will likely lead to their committee’s disbanding, with leaders promising answers as soon as they are available.

The SC gathered for its monthly conference call Feb. 18, a week after NERC’s quarterly Board of Trustees meeting in Savannah, Ga., where trustees agreed to adopt the final recommendations of the Modernization of Standards Processes and Procedures Task Force (MSPPTF). (See NERC Board Accepts MSPPTF Recommendations.)

Under the task force’s recommendations, the Reliability and Security Technical Committee would conduct a biannual review of standard initiation requests to determine whether a new standard was needed. Standard proposals would be handed to a new subcommittee of the Reliability Issues Steering Committee, which would consult with industry to determine a plan for development.

A new pool of on-staff subject matter experts would work with NERC staff to develop a draft standard, which would be posted for stakeholder comment and then revised by a project team. Industry stakeholders then would vote on the standard in a confirmation ballot.

Chair Todd Bennett of Associated Electric Cooperative, who was at the board meeting, discussed with SC members what he knew of NERC’s future steps, but acknowledged that beyond the goal of having the new process in place by the end of 2027, few details of the implementation plan had been worked out. He confirmed this goal included “sunsetting” the SC and revising the charters of the RSTC and RISC, and said the two processes likely would run side-by-side while NERC staff worked out the kinks.

Jennie Wike of Tacoma Public Utilities asked when the SME pool would be formed and if there would be any impacts to existing standard drafting teams. NERC Manager of Standards Development Alison Oswald said there were “quite a few steps to put in place before that can happen.”

Vicki O’Leary of Eversource observed that half the SC members’ terms will expire at the end of 2026, and asked whether NERC would hold an election to fill those vacancies.

Oswald said NERC “had not specifically thought about” that question but said she “could foresee that we would continue on the normal path as is.”

Bennett added that his preference depended on the timeline for the SC’s disbandment. If the committee is dissolved in early 2027, he said, he would prefer “just to keep the same committee … and engaged members that we have.” But if it will last longer, he said it might be better to hold formal elections.

Standards Actions

Along with the MSPPTF updates, the committee had a full slate of standards actions to consider.

A proposal to supplement the SDT for Project 2023-09 (Risk management for third-party cloud services) led the agenda. Manager of Standards Development Jordan Mallory explained that the project — which NERC considers high priority “due to increasing threats to the electric system” — recently lost three of the original 13 SDT members.

Although NERC typically considers 10 members to be sufficient for an SDT, Mallory said because the project is expected to modify a large number of Critical Infrastructure Protection standards, the team believes it will need a larger-than-usual number of members.

NERC staff recommended that the SC approve the solicitation of nominees from industry to bring the team back to full strength. Members approved the proposal unanimously.

Another proposal to replace three departing SDT members — this time for Project 2022-05 (Modifications to CIP-008 reporting threshold) — also gained approval from SC members, though not without some discussion. In this case, NERC already had processed 10 nominations from industry and chosen three candidates to recommend to the committee for approval.

Keith Jonassen of ISO-NE suggested approving one of the remaining nominees as well, arguing that the individual, who was not identified during the meeting would add needed balance to the team by representing ISOs and RTOs. Mallory replied that NERC felt the three chosen “were the top contenders,” adding that in any case, the person in question had expressed a lack of interest in serving on the team. Jonassen’s motion to add the extra nominee was rejected and the original slate passed.

Members also approved proposals to draft Canadian-specific revisions to NERC’s cold weather standard EOP-012-3 (Extreme cold weather preparedness and operations), to modify PRC-029-1 (Frequency and voltage ride-through requirements for inverter-based resources) and to update requirements for supply chain risk management.

The annual status report from the Business Council for Sustainable Energy (BCSE) finds sustainable energy met rising U.S. power demands in 2025 despite the far-reaching policy shifts roiling the sector.

The report also flags this policy uncertainty — along with the slow pace of permitting and interconnection — as a potential barrier to meeting the sharply higher power demand expected in coming years.

The “2026 Sustainable Energy in America Factbook,” prepared by BloombergNEF and published Feb. 18 by BCSE, is the 14th of its kind. It comes at a tumultuous time for the U.S. electricity sector: The Trump administration is executing a sharp shift in strategy while power demand has begun significant growth after more than a decade of minimal increases.

BCSE and BloombergNEF frame this as a time to recommit to sustainable energy.

“These fast-moving dynamics provide an opportunity to accelerate investment into a broad portfolio of sustainable energy technologies,” BCSE President Lisa Jacobson said in a news release. “This diverse set of resources will allow the U.S. economy to prosper, boost national security and economic competitiveness, and deliver reliable and affordable energy for all Americans.”

Ethan Zindler, BloombergNEF’s head of country and policy research, said: “As demand from energy-hungry data centers continues to grow, we’ll likely continue to see upward pressure on power prices. The need to expand supply from sustainable energy sources has never been clearer.”

This emphasis on sustainable energy would be at direct odds with Trump administration policies under many definitions of “sustainable.” But BCSE defines natural gas as sustainable, aligning it with one of President Donald Trump’s priorities: boosting the U.S. natural gas sector. The industry trade group American Gas Association is a BCSE member and helped sponsor the factbook, as did other notable members of the natural gas sector.

The factbook is the latest in a sea of analyses, opinions and invectives that have attributed demand growth to data centers. The authors stop short of blaming data centers for rising electricity prices, a primary line of criticism.

Instead, they acknowledge that data centers — particularly for AI applications — have become central to power planning and are poised to be the dominant force behind rising power demand.

Their power consumption was 18% higher in 2025 than in 2024 and has risen more than 150% over the past five years, the authors write. Data center load reached 23 GW installed and 48 GW under construction or committed to construction with land, power and permits secured. Early-stage announcements — a less certain prospect — combined for 165 GW of potential additional load.

The evolution of the U.S. power generation mix is tracked over 13 years. | BloombergNEF

Meanwhile, a record 1.6 million electric vehicles were sold in the U.S. in 2025 as consumers rushed to qualify for federal tax credits about to expire. This also drove grid investment.

“The need for electricity infrastructure is growing rapidly with rising EV sales and the AI data center buildout,” said Trina White, BloombergNEF’s senior associate for North American energy transition. “This is creating some supply chain bottlenecks while raising the costs for key grid equipment.”

But the same federal policy changes and regulatory obstacles influencing the power sector also crimp the ability or willingness of some private-sector businesses to respond, BCSE said.

Eighty-seven new tariff and trade policies were announced in 2025, the authors said, eroding the stability and confidence needed to attract investment in the clean-tech sector.

“Businesses are ready to deploy solutions to meet energy demand, but they need certainty that policies and permits will not change once commitments to long-term energy sector investments have been made,” Jacobson said.

A total of 54 GW of new utility-scale generation and storage capacity was commissioned in 2025, the most in more than two decades; 90% of it was wind, solar and storage.

New gas generation more than doubled from record-low 2024 additions but still totaled only 5 GW.

New corporate zero-carbon energy procurements totaled a record 29.5 GW.

The One Big Beautiful Bill Act accelerated the phaseout of key tax credits for clean energy development and cut federal subsidies for clean-tech manufacturing.

Permitting setbacks and outright interference were dealt to solar, onshore wind and particularly offshore wind.

As it was hampering other forms of clean energy, the Trump administration boosted support for nuclear generation, geothermal and hydropower technologies.

Overall energy transition investment grew 3.5% to $378 billion.

Greenhouse gas emissions from the power sector rose 3.6% as coal-fired generation increased.

Overall energy costs for consumers, a metric that is taking a prominent role in policymaking and political rhetoric, actually fell 0.2 percentage points to 3.66% of personal expenditures, due to lower gasoline prices; however, natural gas and electricity rose from 1.6% to 1.62%, a reversal from recent years.

Energy consumed to produce electricity rose 2% to 33.4 quadrillion BTU but still was well below the peak of 38.5 quadrillion in 2007, reflecting improvements in energy efficiency and productivity.

Interconnection requests to the seven ISOs and RTOs reached a combined 377 GW, the largest component being storage and the largest number of requests being submitted to ERCOT, followed by MISO and PJM.

The factbook was commissioned by BCSE and supported by contributions from a diverse group of sponsors including Amazon, American Clean Power, JPMorganChase, Schneider Electric, the Polyisocyanurate Insulation Manufacturers Association and Sempra.

Massachusetts could decarbonize its peaking power portfolio by 2050 through aggressive deployment of wind, batteries and demand flexibility, according to a new analysis by a group of environmental nonprofits.

The report found that while decarbonizing the peak would increase electricity costs, overall costs would be comparable to or less than fossil alternatives when accounting for climate and health effects.

“The analysis confirms that decarbonizing peak demand is not an abstract aspiration but a practical and necessary component of Massachusetts’ clean energy transition,” the authors wrote.

Synapse Energy Economics conducted the analysis for the Massachusetts Clean Peak Coalition, with the intention of supporting discussions on the topic at a working group convened by the Massachusetts Office of Energy Transformation.

The consulting firm estimated 2050 costs for clean-peak, business-as-usual and alternative-fuel pathways. It assumed a load profile based on current demand levels plus new load from heating and transportation electrification. Based on historical weather data, it estimated that the state would need an average of 9 GW — and up to 13.9 GW — of peaking capacity by 2050.

The clean energy pathway assumed 24% demand flexibility, which would require aggressive deployment of “a suite of load reducing and load shifting measures” including efficiency upgrades, smart appliances, managed vehicle charging, behind-the-meter energy storage and advanced thermal storage technologies, the authors said.

Massachusetts also is rolling out advanced metering infrastructure, which should help enable incentives for demand flexibility for residential ratepayers and help lower peak load.

Notably, the study’s cost comparisons did not include costs associated with demand flexibility or other demand response resources.

The clean energy pathway assumed a cost-optimized mix of offshore and onshore wind and batteries with storage durations ranging from two to 100 hours. Storage was the largest component of the clean peak portfolio, with 100-hour storage comprising most of the storage built by the model. The model also assumed 4.4 GW of offshore wind and 2 GW of onshore wind.

“While onshore wind is less expensive to build, onshore wind capacity was capped at 2 GW to reflect the constraints of siting onshore wind,” the authors noted.

Synapse compared the annualized cost of energy of the clean energy pathway to portfolios composed of new gas turbines and generation fueled by hydrogen and “renewable” natural gas.

When adjusted for the value provided by off-peak wind generation, the findings show the decarbonized pathway to be cheaper than the alternative fuel pathways but more expensive than the gas-based pathway. However, when accounting for “externalities” like carbon emissions and public health impacts the modeling showed the clean portfolio to be the most cost effective.

The report found that the adjusted costs of the clean portfolio would add about $10 per month to the average residential electric bill.

“While these efforts may result in moderate cost increases for ratepayers, the costs need to be considered within the context of the high social and environmental costs of continuing to depend on polluting gas and oil power plants,” the authors wrote.

Recommendations

Based on Synapse’s findings, the authors provided a suite of recommendations aimed at promoting clean peaking resources. These include expanding demand flexibility programs and incentives; prioritizing medium- and long-duration storage; and accounting for public health and climate costs when calculating cost effectiveness.

They expressed skepticism about the potential of alternative fuels to meet peaking demand, pointing to high cost projections and arguing that “replacing fossil fuel use with these alternative fuels won’t meaningfully decrease greenhouse gas emissions and will often maintain the same, or worse, levels of local air pollution.”

The report coincides with intense policy debates in the state over how to define and address issues of energy affordability.

Democratic leaders in the Massachusetts House of Representatives have been working to advance a controversial energy bill that would scale back several key climate programs in the state, particularly its energy efficiency program.

In contrast to the report authors’ emphasis on accounting for the full range of climate effects, the initial version of the House bill proposes to eliminate requirements for the state Department of Public Utilities, including emissions costs when calculating cost effectiveness. The bill also would prohibit state agencies from implementing any regulations or programs with “unreasonable adverse impacts” on energy costs or the state’s economic competitiveness. (See Top Mass. House Members Seeking Major Rollback of Climate Laws.)

MISO said lackluster generating unit performance led to an emergency declaration during the late January winter storm.

The grid operator also dealt with its own technical issues during the storm that caused pricing glitches.

MISO declared a maximum generation emergency around 6 a.m. Jan. 24 for its Midwest region. It made emergency power purchases from PJM, used its member generators’ emergency ranges, sent instructions for members to make public appeals for conservation and called on load-modifying resources to meet demand. (See MISO Enters Max Gen Emergency in Arctic Blast.)

Ultimately, MISO’s 105.3-GW peak demand Jan. 27 during conservative operations was higher than Jan. 24’s approximately 96.4-GW crest.

“It’s become an annual event to see these deep, cold events push in,” Executive Director of System Operations J.T. Smith said during a Reliability Subcommittee meeting Feb. 17.

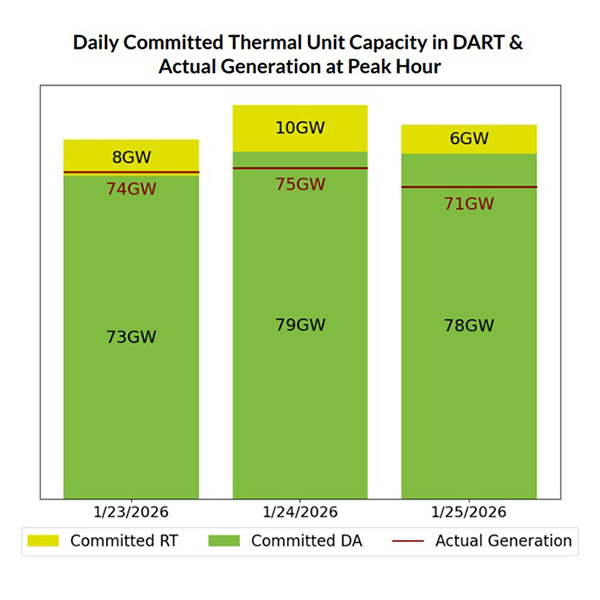

This time, Smith said thermal generators were “not living up to the offers they submitted” to MISO. Instead of resources tripping offline, they simply became unavailable. The RTO said that of the 79 GW committed in the day-ahead market and the additional 10 GW committed in real time, 75 GW in total generation showed up Jan. 24.

MISO’s committed day-ahead and real time commitments compared to actual generation Jan. 23-25, 2026 | MISO

“From a reliability operations perspective, we need good, valid offers,” Smith said.

Smith said up until the evening of Jan. 23, “we were showing in our next-day plan to be fairly long.” That changed as MISO entered the operating day. It forecast “persistent negative capacity margins” for its Midwest region Jan. 24, forcing it to declare the emergency, Smith said.

Combustion turbines’ lead times “hindered real-time commitments,” Smith said. In MISO Midwest, 29 CTs extended their start times “significantly” Jan. 23. Of those, Smith said 13 made sure to stay under the RTO’s 24-hour lead time threshold to ensure they did not lose capacity accreditation value.

Smith said some of the resources modified their start-up times in real time. MISO staff said they are examining the 24-hour limit to see if it is too generous.

“Right now, a lot of folks are trying to mitigate their capacity accreditation impacts, and that’s understandable,” he said. “That is starting to become a problem in the winter that we’re going to have to have some conversations about.”

Smith also said when MISO asks its members to make sure offers are updated, that means for the next few days, not just the day of.

Of the 44 GW in total generation outages Jan. 24, MISO experienced 17 GW of unplanned outages. It also counted low wind production throughout the sustained cold Jan. 22-27, averaging slightly above 3 GW.

“During [Winter Storm] Fern, at one point, we got below a gigawatt of wind on either Jan. 23 or Jan. 24,” Smith said.

MISO reported that it exceeded its regional transfer limit by about 1,500 MW in the South-to-Midwest direction during the emergency. There is usually a 2,500-MW limit for South-to-Midwest flows.

JT Smith, MISO | New Orleans City Council

“That is something that is not preferred for your contingency management,” Smith said, adding that MISO was able to work with the Tennessee Valley Authority, Southern Co. and other parties to the transfer agreement to secure extra space on the constraint.

MISO saw potential for a 5-GW deficiency on the morning peak Jan. 24. It secured 2 GW from available load-modifying resources and lined up 3 GW of emergency purchases from PJM. The RTO also called for members to appeal to the public, which was a “big deal,” Smith said.

Ahead of the evening peak, MISO again projected a 2- to 3-GW deficiency as solar lowered output and other generation ramped up to replace. Once again, MISO made the decision to make emergency purchases.

Smith said MISO was not certain if load-modifying resources would again spring into action after delivering reductions that morning. Under its tariff, MISO’s load-modifying resources are under no obligation to perform once they have already been called up in a day.

He said operators’ thinking was MISO was “only allowed to touch those resources once in a 24-hour period.”

“We did walk out of those emergency purchases pretty quick and were able to come out of the emergency declaration,” Smith said. As the next week began, and the cold moved from west to east, MISO was able to return the favor and export to the east, he said.

Pricing Malfunction

MISO’s internal systems hit a snag during the emergency.

The grid operator experienced software failures affecting its ex post pricing engine that prevented it from publishing its emergency prices for an 11-hour span Jan. 24. Because of that, MISO said prices did not reflect emergency conditions, and imports were not as incentivized as they would have been if the higher prices had been known. The RTO used a workaround to publish its real-time locational marginal pricing until Feb. 5, when it made a permanent fix.

The RTO said the imports it accepted from PJM were not motivated by pricing, but instead by its explicit request to purchase emergency power.

Multiple stakeholders asked MISO to analyze the impact that unpublished prices had on market behavior and share the results. They also asked about emergency pricing extending into MISO South on Jan. 24, when the region was not under emergency orders.

Smith said MISO would discuss pricing effects at upcoming Market Subcommittee meetings. It has yet to root out the cause of emergency pricing bleeding into MISO South, where no emergency was present.

‘Slow to Solve’

Smith also acknowledged that “the day-ahead markets were slow to solve” as weather moved in and complicated operations.

He said the day of the emergency, MISO’s systems struggled to manage about $870 million in market transactions. For comparison, “today, we cleared at $40 [million] to $50 million,” he said.

The complexity of added demand, pricing nodes and constraints taxed MISO’s computing power. “We might have to think about that. If the world is going to get more complex, we’re going to have to think about our market days,” Smith said, suggesting that the RTO may want to start clearing its day-ahead market earlier. “There is a computational issue that we need to think about overall.”

MISO’s slow-to-post day-ahead prices undoubtedly led to difficulties for market participants securing gas supplies.

Finally, Smith said MISO’s call for members to issue public appeals for conservation needs should be easier to understand.

“I don’t know if that is because it was 6 a.m. on a Saturday,” Smith said. “We’re going to have to do something to create a more clear outcome on this. … We got a ton of phone calls asking, ‘Are you really doing this, or not?’”

“This is significant to go to Step 2c,” said Jim Dauphinais, an attorney for multiple industrial customers, referring to the RTO’s emergency levels. “I believe that hasn’t happened in 17 years.”

At the height of the storm, MISO entered Step 2c, which is equivalent to NERC’s Level 2 Energy Emergency Alert. The next step would have entailed load shedding.

Dauphinais asked MISO to create a frequently asked questions document on the incident for stakeholders to review.

“It really comes down to the communications for WPPI,” said WPPI Energy’s Valy Goepfrich. Even though MISO claimed it was looking for emergency resources that could be deployed in two hours or less, the utility never received orders from the RTO, she said.

“We kept waiting for the scheduling instructions. It was really confusing,” she said.

MISO will go over its emergency actions again during its quarterly Board Week in late March in New Orleans. There, the Board of Directors will hear details and pose questions to RTO leadership.

The U.S. Department of Energy has issued a fourth emergency order keeping the J.H. Campbell coal plant in Michigan online through mid-May.

DOE renewed its emergency declaration Feb. 17, the day it was set to expire, under Federal Power Act Section 202(c). The 1.45-GW coal plant in western Michigan is now mandated to remain operational until May 18. (See DOE Issues 3rd Emergency Order to Keep Michigan Coal Plant Open.)

Energy Secretary Chris Wright said emergency grid conditions “will continue in the near term and are also likely to continue in subsequent years.” Campbell has been operating since May 2025 under orders from the department.

The running total for keeping the plant open is up to $135 million as of the end of 2025, according to a Securities and Exchange filing Feb. 10 from owner Consumers Energy.

Over 2025, the trio of DOE directives led Consumers to accrue $290 million in costs. The company said plant output earned the utility $155 million in revenue, leaving $135 million due in costs including fuel, employee pay and plant maintenance. That means the utility lost nearly $631,000/day over the last seven months of 2025 running the nearly 64-year-old plant.

Consumers sought FERC approval in late January to pass nearly $42 million in net costs for running Campbell on to utility customers across MISO Midwest (ER26-1138). Those costs stem from the first order in May 2025 only.

Despite opposing the forced operations of the plant, the Michigan Public Service Commission supported the cost recovery.

“While the Michigan PSC adamantly disputes that there is, in fact, an energy emergency that warrants the use of the Federal Power Act to keep the Campbell plant open, the merits of the DOE order are not at issue in this docket,” the commission said.

The utility anticipated the issuance of the fourth order in its FERC filing.

“Expeditious action is warranted here to ensure regulatory certainty as we approach the expected issuance of a fourth DOE order requiring the company to keep the Campbell plant available to operate for another 90-day period,” Consumers said.

Environmental groups condemned the fourth issuance, which would keep the plant operating nearly a year past its regularly scheduled retirement date.

“Because of the Trump administration’s illegal mandates, this aging, polluting coal plant is bleeding millions of dollars, and Midwestern families are footing the bill for it,” Ted Kelly, counsel with Environmental Defense Fund, said in a statement. “None of this is necessary. The utility and state officials worked for years to replace the capacity of this more than half-a-century-old coal plant with cheaper, cleaner energy — and made sure that these plans would deliver reliable power. It’s yet another example of the Trump administration putting its thumb on the scale to prop up the coal industry at the expense of people’s health and their hard-earned money.”

In early February, Wright credited DOE’s string of emergency orders to keep coal plants online with helping to avoid power failures during the late January winter storm and subsequent cold snap. The department’s initial order to stop Campbell from shuttering has proven to be a familiar script for other orders to coal plants in Washington, Pennsylvania, Colorado and Indiana.

Prior to the second Trump administration, DOE generally used such emergency orders for short-lived periods during unexpected events, such as extreme weather or natural disasters.

EDF said three coal plants associated with the orders are increasingly in disrepair: The Campbell plant partially failed during MISO’s June 2025 peak demand; Unit 18 at the R.M. Schahfer Generating Station in Indiana is broken and has been since July 2025; and a unit at the Craig plant in Colorado broke down in late 2025 after a valve failed.

Cyber threat groups around the world continued to expand their capabilities in 2025, while their targets in developed countries largely failed to keep pace, cybersecurity firm Dragos warned in its Year In Review report released Feb. 17.

Multiple threat groups “crossed a line” by taking steps toward active disruption of victims’ operational technology and industrial control systems assets, rather than “simply gaining access and waiting,” Dragos said. The firm called this action “the removal of the last practical barrier between having access and being able to cause physical consequences” and a sign that malicious actors are preparing to act against their targets.

Dragos used multiple sources to compile the report, including its monitoring resources inside clients’ OT environments, trusted partners and third-party datasets. The firm considers its information “the world’s largest dataset on OT security … threats and vulnerabilities” but warned that “no government, vendor or other entity can have” a complete view of the threat landscape.

Among the 26 threat groups Dragos tracks, 11 were active in 2025. The active groups included Electrum, blamed by Dragos for an attack against Poland’s power grid Dec. 29. (See Dragos Blames Electrum Group for Poland Grid Cyberattack.) The company has a policy against identifying threat actors with specific countries, but the Cybersecurity and Infrastructure Security Agency has linked Electrum to Unit 74455 of Russian military intelligence. The group also has been linked with cyberattacks against Ukraine’s energy grid in 2015 and 2017.

Dragos has called the December event “the first major coordinated attack targeting distributed energy resources at scale.” Attackers targeted systems managing communications and control between grid operators and DERs, gaining access to OT systems with direct access to generation assets.

Although communication was lost, no outages occurred because the default behavior of the affected devices was to remain on. Dragos also wrote in its report on the incident that the relatively large percentage of inertial generation on Poland’s grid — with coal-fired plants representing more than 50% of the generation fleet — made the attack “unlikely to cause a nationwide blackout.”

In a press conference accompanying the release of the report, Dragos CEO Robert M. Lee said the Poland attack should set off alarms in countries that have moved more aggressively to transition to DERs.

“These are usually remote assets. … Because they’re not big, they generally don’t have the same level of budget [as coal and nuclear plants]; therefore, they’re not getting … the security, which we wish was better, for even those facilities,” Lee said. “But they’re making up more and more of the energy portfolio. [It] used to [be], going after a wind farm … we can cover it. But if 25% of your electric system is wind farms and somebody goes after them, it could be impactful to you.”

Lee said utilities should take the event as a sign that threat actors have recognized the growing importance of DERs on the system. He emphasized that while there is no evidence the attackers tried to use the compromised communications equipment to misoperate the connected DERs, this reflects a lack of visibility into the system and should cause concern rather than relief.

“I can’t say with confidence that the attacker wasn’t inside the control loop. … When I talk to governments … I don’t love being in the position to tell them, ‘We’re not actually sure if the adversary is there or not, but the power is on,’” Lee said. “That’s not a very comfortable place to be for a lot of folks. What I can tell you is that [with] the access they had, they absolutely could have gone further. … It wouldn’t have been rocket science to go the extra step.”

Lee praised FERC and NERC for adding requirements to the ERO’s Critical Infrastructure Protection standards in 2025 that electric utilities implement internal network security monitoring at many grid-connected cyber systems to detect intrusions into their OT networks. (See FERC Responds to ERO’s INSM Clarification Filing.) However, he urged utilities to get their monitoring in place ahead of the deadline, saying that the Poland attack shows attackers already are willing and able to infiltrate them.

New Attackers Identified

Three other threat actors, named Azurite, Pyroxene and Sylvanite by Dragos, were newly identified in 2025, although they are believed to have been active for longer.

All three have targeted victims in the U.S., among other countries. Azurite and Sylvanite are known to have targeted the electric industry.

On a technical level, Azurite’s attacks share similar techniques with the Flax Typhoon threat group. Microsoft has claimed that Flax Typhoon is based in China and primarily operates against targets in Taiwan.

Dragos wrote that Azurite’s activities have demonstrated the ability to reach Stage 2 of the ICS kill chain, defined by SANS Institute as a capability to meaningfully attack the ICS, as opposed to espionage or intelligence gathering. The organization clarified that it has not yet observed Azurite manipulate or modify OT software, but the threat group has been seen to operate in OT environments using lateral movement and has demonstrated “knowledge of OT-centric software.”

Pyroxene also has demonstrated Stage 2 capabilities, Dragos wrote. The group has overlaps with APT35, a cyber actor linked with the government of Iran and also known as Charming Kitten, Phosphorus and Mint Sandstorm.

Pyroxene’s targets to date have been in the utility, telecommunications, technology, manufacturing and logistics space, including a water utility serving the port of Haifa in Israel. Other victims have been in the Middle East, U.S. and Europe.

Sylvanite has demonstrated only Stage 1 capabilities, specializing in gaining initial access that it then hands off to other actors for further exploitation. The group’s partners include Voltzite, which Dragos reported had gained Stage 2 capability in 2024. (See Dragos: Attacks on ICS Increased in 2024.) Dragos found “extensive technical overlaps” between Voltzite and Volt Typhoon, the China-connected group that has been accused of embedding itself in the information technology networks of U.S. critical infrastructure organizations for more than five years.

Just a few weeks after taking over as CEO of ISO-NE at the beginning of 2026, Vamsi Chadalavada faced a trial-by-fire introduction to the job.

Temperatures plunged Jan. 24, followed by heavy snowfall across the region the next day. With the snow suppressing behind-the-meter solar generation, ISO-NE exceeded its high-range winter peak load forecast.

The low temperatures persisted, averaging 14 degrees F below normal over the last nine days of January and leading to significant depletion of generators’ stored fuel inventories as gas prices skyrocketed. Energy costs shot up, and ISO-NE experienced the highest monthly energy costs in its history. (See Prolonged Cold Drove Record Monthly Energy Costs in New England.)

Despite the challenging conditions, ISO-NE met all reliability requirements throughout the prolonged event and officially lifted its preemptive abnormal conditions alert Feb. 11.

“I’m glad we’re through it,” Chadalavada said in a recent interview with RTO Insider. “The fact that we were able to maintain not only the energy demand but also operate with the levels of reserve margins that indicate that we’re capable of withstanding the first or second contingency, is extraordinary.”

While Chadalavada is new to the job, he is far from a new face at ISO-NE: He joined the RTO in 2004 and served as COO from 2008 through the end of 2025 under longtime CEO Gordon van Welie.

“A lot of what we’re doing right now I’ve had some experience with,” he said. He credited ISO-NE’s success throughout the extended cold stretch in large part to the high levels of collaboration among the RTO, state and federal agencies, and the region’s generation fleet.

He said ISO-NE also has benefited from technology investments made in recent years, including incorporation of probabilistic modeling into its rolling 21-day energy assessments, which the RTO published daily throughout the event.

“A tool like that is invaluable in preparing us with a higher degree of confidence than we’ve ever had,” he said, adding that the analyses gave the RTO “a good sense of the worst-case outcome,” allowing it to plan effectively.

Consensus and Agility

While ISO-NE’s performance during the cold snap has drawn praise from stakeholders, the price spikes brought by the event have fueled concerns about the design of the RTO’s new day-ahead ancillary services (DAAS) market.

At the February meeting of the NEPOOL Participants Committee, Chadalavada announced ISO-NE’s support for a series of “narrowly targeted” DAAS market changes recommended by the ISO-NE Internal Market Monitor (IMM), along with plans to evaluate changes to its pay-for-performance rate and its treatment of exports during scarcity events.

“Typically, those would all be 12- to 18-month projects,” he said. “We’re challenging our organization to do all of them in six to nine months, including a stakeholder process.”

These projects come on top of an already-packed annual work plan, which includes work to establish an internal asset condition project reviewer; select a preferred solution from the first iteration of the Longer-term Transmission Planning procurement process; and complete work on the RTO’s long-running Capacity Auction Reform (CAR) project.

The DAAS market has been the subject of growing concern from the end user and supplier sectors in recent months amid mounting costs. While ISO-NE’s initial impact analysis — based on 2019-2021 data — estimated the annual incremental costs of the market to be about $140 million, the IMM calculates those costs over the market’s first 11 months reached about $921 million.

The IMM’s proposed changes are intended to induce lower-priced offers and greater market participation. While the details have yet to be refined, ISO-NE has offered high-level support for the reforms.

The recommendations generally have been well received by market participants, while some stakeholders have asked for even more urgency from the RTO, with one group pushing for a vote on the proposals at the NEPOOL Markets Committee in March.

Chadalavada has emphasized the importance of being nimble in response to market issues while also building strong consensus among stakeholders to ensure durable solutions. The proposed DAAS market changes could be an important early test of this approach.

Long project timelines have been especially apparent in ISO-NE’s resource capacity accreditation efforts. The RTO initiated the ongoing project in 2021 before expanding the scope in 2024 to include broader capacity auction changes.

If everything goes according to plan with the CAR project, ISO-NE finally will file the accreditation changes by the end of 2026 and implement them for the 2028/29 capacity commitment period.

“If we have long life cycles — three to five years — by the time you deploy them, you’re already behind,” Chadalavada said.

To reduce project timelines, he said ISO-NE could look to split larger projects into smaller components; deploy artificial intelligence and technological innovation; and pursue simpler solutions, which it could refine after implementation.

Managing Uncertainty

Chadalavada said he intends to focus on planning “in five- to seven-year increments, making sure that each increment fits into the future direction for New England.”

This should help ensure ISO-NE is preparing for the future in the most cost-effective manner amid great uncertainty about the region’s future load profile and resource mix, he said.

Predicting demand over the long-term is similarly challenging. While ISO-NE forecasts substantial demand growth through 2050 due to the electrification of transportation and heating, the pace of electrification has proven hard to predict, and the RTO has scaled back its 10-year forecast of electrification demand in each of the past two years. (See ISO-NE Scales Back Vehicle, Heating Electrification Forecasts.)

The possibility of data center development adds another major source of load-side uncertainty. While New England so far has experienced relatively limited impacts from the data center boom, some utilities have reported an uptick in data center interconnection requests.

Chadalavada said ISO-NE is “actively monitoring” the potential for new data center loads.

“We’re active behind the scenes,” he said. “I think we haven’t had to mobilize in earnest because we haven’t had the volume of requests and the urgency that’s playing out in PJM and other parts of the country. But I do expect that it’ll make its way to New England, and we will be ready.”

In late January, six New England senators signed a letter to Chadalavada seeking information on how ISO-NE plans “to protect residential ratepayers from data center-driven price increases.” It stressed the need “to require tech companies, not American families, to foot the bill for their load.”

In his response, Chadalavada noted that “no new large data centers (or other large electrification projects) have committed to proceeding with construction at this time.”

In conversation, he echoed the importance of preventing cost shifts onto other consumers. He also expressed optimism about the role markets will play in ensuring resource adequacy in the coming decades.

He said he views markets as “the most cost-effective way to not only provide incentives for new entry, but also price retirement and deactivation of resources.”

The capacity, energy and ancillary services markets all play an important role in signaling the need for new resources while protecting consumers from investment risks, he said, adding that he expects wholesale markets will continue to work for the region over the long term.

“Will it be easy? No. Will it be controversial? Yes, because there are always different sorts of opinions and viewpoints about the effectiveness of markets,” he said. “But from an ISO standpoint, I cannot think of a better way to achieve resource adequacy for New England while having cost effectiveness as an equally important measure.”

Portland General Electric has agreed to buy most of PacifiCorp’s Washington utility operations for $1.9 billion, PGE said Feb. 17.

Under the terms of the deal between the two Portland, Ore.-based utilities, PGE will acquire three generation facilities, 4,500 miles of transmission and distribution lines, and a 2,700-square-mile service territory containing about 140,000 electricity customers concentrated in Yakima, Walla Walla and nearby communities.

The generating facilities include the 477-MW gas-fired Chehalis Power Plant, as well as the Goodnoe Hills and Marengo wind farms, rated at 94 MW and 234 MW, respectively.

PGE plans to manage the Washington operation through a newly formed subsidiary regulated by the Washington Utilities and Transportation Commission. The utility is partnering on the acquisition with Manulife Investment Management, which will own 49% of the new company.

“We are excited for the opportunity to continue to grow, expanding into Washington and building upon PGE’s foundation of operational excellence and customer service,” PGE CEO Maria Pope said in a statement. “We look forward to our partnership with Manulife Investment Management, who bring a track record of investment success across the utility sector and Pacific Northwest agriculture and timberland industries.”

“We are pleased to partner with PGE to support this investment in reliable generation, transmission and distribution for Washington communities,” said Recep Kendircioglu, global head of infrastructure at Manulife Investment Management. “This partnership represents an opportunity that fits well within our infrastructure strategy and leverages our experience in utility investments.”

In a separate statement, PacifiCorp said “diverging policies” among the six states the utility serves “have created extraordinary pressure” that has affected its ability to reliably serve its customers at the lowest cost.

“These challenges have impacted the company’s financial stability, liquidity and credit ratings. The sale will be a critical step in strengthening PacifiCorp’s financial position and simplifying operations across its service area,” the company said.

“This is a targeted step toward ensuring the continued delivery of safe, reliable power to our nearly 2 million customers in the West and Intermountain West,” PacifiCorp CEO Darin Carroll said. “This will improve the company’s financial stability while simplifying our operations to support our long-term commitment to customers in each of our remaining states.”

The two utilities said the deal, which is subject to state and federal regulatory approval, should close in about 12 months.