Oregon has released a draft road map to provide state lawmakers with recommendations on how to proceed with offshore wind endeavors, while acknowledging the uncertainty the industry faces.

The Oregon Department of Land Conservation and Development (DLCD) released the draft offshore wind energy road map for public review Feb. 17.

The document is the product of 2024 Oregon House Bill 4080. The 192-page report comes amid policy uncertainty, with the federal government attempting to stop offshore wind projects across the country. (See N.Y. Cancels Solicitation but Remains Committed to OSW.)

“Since the adoption of House Bill 4080, uncertainties about federal policy and the future of the offshore wind energy industry have grown,” the document states. “Nevertheless, the need remains to advance state clean energy and climate goals, to strengthen state policies, and to build capacity and knowledge should the federal interest in offshore wind energy development off Oregon’s coast return.”

The report considers four scenarios: large-scale offshore wind development, pilot projects, economic participation without wind turbines or opting out of wind development.

Under the large-scale offshore wind development and pilot project scenarios, the DLCD recommends launching rulemaking efforts to address policy gaps related to offshore wind technology.

Policymakers should encourage investments and reduce risks for emerging technologies, collaborate with other states, support local governments, and enhance coordination in areas like transmission and procurement, among other recommendations, according to the road map.

“By leading with proactive planning, broad community engagement and strategic capacity-building now, Oregon can better position itself to protect its treasured resources, secure meaningful community benefits and be ready to make informed decisions when the time comes to decide on offshore wind energy development,” the DLCD wrote. “Under any future scenario, Oregon can act now to strengthen its policy standards, grow the state’s knowledge of the ocean and build a resilient energy system that moves Oregon closer to our climate goals and prepares us for the multiple paths ahead.”

The deadline to submit comments on the road map is April 3. The public can send comments to dlcd.oswroadmap@dlcd.oregon.gov.

Solar and wind resources could generate up to 85% of California’s electricity by 2045, according to a report being drafted by the state’s Energy Commission.

CEC staff presented the findings at a Feb. 19 workshop on SB 100, the law requiring that renewable and zero-carbon resources supply 100% of retail sales and electricity procured in California by 2045.

The findings are part of a joint agency draft report on SB 100 that has not been published. The commission expects to publish the report in April, Senior Information Officer Stacey Shepard told NetZero Insider.

At the workshop, CEC staff presented a reference scenario in which the total system capacity increases from 150 GW in 2025 to 310 GW in 2045, with most of the new resources coming from solar (97 GW), energy storage (45 GW) and wind (24 GW in-state, 27 GW out of state).

“However, all scenarios do have a need for some other sort of resources in addition to solar and storage,” Hannah Craig, lead modeler for the CEC, said at the workshop. “Some scenarios are building carbon capture and storage, and some scenarios are building geothermal, and a lot of scenarios are building in-state wind.”

Natural gas could provide as little as 3% of the state’s energy, according to the presentation.

The federal One Big Beautiful Bill Act increased the cost of the modeled resources by 20 to 30%, Craig said. Staff observed that the model selected more clean, firm resources, such as geothermal and carbon capture and storage, moving “a little bit away from wind and solar [because] those resources are no longer receiving” subsidies under the Inflation Reduction Act, Craig said.

Solar curtailment no longer would be limited to spring in California, according to the model. Instead, curtailment increases throughout the year because of the widespread deployment of solar resources, along with changing import patterns, Craig said. “So out-of-state imports are dropping in the spring and summer, but they’re rising in winter, and the model really does depend a lot on those imports being able to show up in winter.”

California also becomes a net electricity exporter in the model, Craig added.

One potential hole in the model is that it does not currently include forecasted data center loads, and data center growth is one of the biggest uncertainties for California’s grid, CEC Vice Chair Siva Gunda said at the workshop.

Data center load in the state could reach 25 GW by 2045 under some scenarios, Gunda said. However, the demand scenarios used for the SB 100 report use the 2023 integrated energy policy report demand forecast, which doesn’t include this level of new data center load, CEC staff said.

CPUC President Alice Reynolds asked if the upcoming expansion of Western markets would affect the model’s resource mix.

“The more that we can integrate California with the West, the more that we can tap into synergies,” Craig replied. “It’s just a little bit easier for the model because there’s different renewable profiles happening all across the West. There is a lot of value in being able to ship that power and meet some of your winter needs with out-of-state wind.”

To feed the voracious energy appetite of the AI revolution, Silicon Valley has found a massive, carbon-free battery: the American nuclear fleet.

Faced with a staggering projected increase in summer peak demand over the next decade, Big Tech is attempting to bypass congested grid interconnection queues. Its solution is co-location: physically plugging hyperscale data centers into nuclear power plants. (See Talen, Amazon Enter PPA for 1.9 GW of Power from Susquehanna.)

While FERC and state regulators fiercely debate whether these deals will shift costs onto residential ratepayers, they are ignoring a more critical question: By physically and electrically fusing our most hyper-connected digital assets (AI data centers) with our most sensitive kinetic assets (nuclear reactors), are we engineering a catastrophic vulnerability?

Put simply: If a co-located data center is hit with ransomware, does the nuclear plant have to trip offline?

Shahid Mahdi

To find the answer, we must look to the greatest cybersecurity failure in modern U.S. energy infrastructure history: the May 2021 Colonial Pipeline attack. (See Colonial Hack Sparks Competing Recommendations at FERC.)

In the energy sector, infrastructure is built on distinct layers of technology. There is the information technology, which handles software and billing, and the operational technology, which are the physical levers, valves and switches that control the flow of energy.

When Russian ransomware group DarkSide infiltrated Colonial Pipeline, it did not hack the OT. It never touched the pipeline’s physical controls. It attacked the IT systems, locking up administrative files containing sensitive information and demanding a $5 million ransom.

Yet the pipeline was shut down, paralyzing the Eastern Seaboard. Why? Because out of blind panic and an inability to safely segregate the IT networks from the OT networks, the operators were forced to pull the plug on the physical infrastructure to prevent the infection from spreading.

Ultimate IT and OT Assets

An AI data center is the ultimate IT asset. It is a sprawling supercomputer designed to be connected to global networks, ingesting and processing massive amounts of data from the open internet. A nuclear power plant, conversely, is the ultimate OT asset, reliant on precise, secure and isolated physical engineering.

If a state-sponsored adversary or a ransomware-as-a-service syndicate breaches the data center’s IT network, the resulting chaos will not be contained to silicon chips. If the utility operator cannot prove an “air gap” exists between the data center’s infected servers and the nuclear reactor’s operational controls, they will face the same horrific choice Colonial Pipeline did. Out of an abundance of caution, the nuclear reactor may have to be scrammed — abruptly taken offline — costing millions of dollars and draining firm baseload power from the surrounding public grid.

Currently, the regulatory apparatus is fundamentally misaligned to handle this threat. State utility commissions and federal agencies are operating in a “regulatory labyrinth,” tracking thousands of filings across a fragmented system. But their focus remains mostly financial. FERC in 2025 was directed to initiate a proceeding (EL25-49) to consider issues related to the co-location of large loads at generation facilities, but the primary concerns remain grid reliability and cost allocation.

As Congress, FERC and NERC establish the rules of the road for AI-nuclear co-location, they must mandate “resilience by design.” Tech companies seeking direct access to nuclear power must be required by law to finance and implement military-grade network segmentation. The burden of proof must fall on the developers to demonstrate that a catastrophic digital breach of their AI servers will not mathematically or operationally necessitate the shutdown of the adjacent nuclear core.

The AI era promises immense breakthroughs, but it also transforms every server farm into a potential backdoor to our critical infrastructure. We learned the hard way that a hacked billing system can stop the flow of gas. We cannot afford to learn what a hacked algorithm might do to a nuclear reactor.

Shahid Mahdi is a director at energy regulatory intelligence company EnerKnol and an expert in cybersecurity threats to energy infrastructure.

ERCOT staff have promised more clarity on the link between the initial batch study process for large loads and the subsequent studies and existing planning structure during a workshop scheduled for Feb. 26.

Jeff Billo, the grid operator’s vice president of interconnection and grid analysis, told the Texas Public Utility Commission at its open meeting Feb. 20 that several open questions remain from the first of two previous batch study workshops and the stakeholder input gathered since (59142).

“There’s still things we need to work through … to try to address that feedback,” he said.

Chief among them is the linkage between the batch studies and ERCOT’s Regional Planning Group, the primary forum for discussion, input and comment on issues related to planning the system for reliable and efficient operation. He said stakeholders want to know how “Batch Zero,” the first study, will link directly to “actionable” transmission project approvals by the RPG.

Also at issue is how controllable load resources (CLRs) and co-located generation should be treated within the batch study.

Billo said ERCOT expects four sets of revision requests will be needed to resolve those questions and fully implement the batch process:

the transitional Batch Zero study, with a filing targeted for March 4;

the ongoing study process referred to as Batch One+;

co-located generation; and

the CLR concept.

Stakeholders have coalesced around a six-month cadence for batch studies; more proactive, structured and transparent communication; and including operation readiness and financial commitments for Batch Zero eligibility, Billo said.

ERCOT is targeting the Board of Directors’ meeting June 1-2 to receive approval for Batch Zero. It has scheduled four workshops on the filing, with the later meetings narrowing in on specific topics with deep-dive discussions.

The grid operator also is attempting to bring the co-located generation and CLR revisions to the same board meeting.

“There is just a lot of technical details to work through with those,” Billo said. “It’s possible that those don’t make it to June, but we’re at least going to start off with the anticipation that we’re going to try for that.”

He said staff will work with the Technical Advisory Committee’s leadership and schedule additional meetings to ensure protocol changes for another ancillary service, Dispatchable Reliability Reserve Service, and voltage ride-through requirements don’t fall through the cracks. ERCOT plans to bring both to the board in June.

“I think the key to being successful here is listening to stakeholders about the questions … specifically around transparency into this process,” PUC Chair Thomas Gleeson said. “I think ERCOT heard loud and clear from the commission that this needs to be a public process with a lot of input.” (See Batch Study Job No. 1 for ERCOT Stakeholders.)

PUC Rejects EPE Cost Recovery for Newman

The PUC approved an administrative law judge’s proposed decision in El Paso Electric’s first fully litigated base-rate case since 1991, but not before directing revisions to 10 items in the order primarily related to cost recovery.

EPE was seeking 100% recovery of $47 million in cost overruns for Newman Unit 6, with 100% allocation to its Texas retail jurisdiction. The gas-fired unit, which serves parts of neighboring New Mexico, was brought online in 2025.

The commissioners agreed with Gleeson’s recommendation to reject the utility’s request. They added a finding that EPE’s off-system sales margins “are being used in a way that benefits both New Mexico and Texas customers.”

EPE filed the rate case in January 2025, seeking a $129 million increase in Texas-jurisdictional retail rates. The utility cited about $1.55 billion in investment in new and existing generation, transmission and distribution capacity and was attempting to set all customer class base-rate levels at the total cost of service.

NYISO proposes to use a set of scenarios rather than relying on a single base case in its Reliability Planning Process to avoid study-by-study fluctuations in determining reliability needs.

ISO officials detailed its proposed revisions for the first time in a marathon meeting of the Transmission Planning Advisory Subcommittee (TPAS) on Feb. 19.

Under the new process, NYISO would compose a base case and several alternative scenarios with stakeholder feedback. It then would determine whether reliability violations occur across the scenarios and base case. If a large magnitude violation persisted across multiple scenarios, NYISO would declare a reliability need.

Yachi Lin, NYISO director of system planning, said this would help avoid being too conservative and overbuilding the system.

NYISO now relies on a single base case, which is updated annually based on what system changes the ISO observes. In recent cycles, this has led to finding and declaring needs only to retract them as the base case updated.

“We have that issue of flip-flopping based on year-over-year volatility of our assumptions,” said Ross Altman, senior manager of reliability planning for NYISO. The new process would weigh the base case against a range of “likely scenarios.”

Altman pointed to the whiplash of reliability findings for New York City. (See NYISO Cancels 2033 Reliability Need for NYC.) He said under the new system, the ISO would not declare a reliability need if a reliability violation did not “significantly persist” across multiple scenarios.

How these findings would interact with other NYISO reliability studies will be discussed at a joint meeting of the TPAS and Installed Capacity Working Group on Feb. 26.

The discussion at the Feb. 19 meeting lingered on whether stakeholders would have voting power over which scenarios would be included in the Reliability Needs Assessment.

“It looks like NYISO is developing all the scenarios without market input. Results are posted for consideration of feedback which NYISO may ignore, which may actually lead to way overbuilding the system,” said Martin Paszek, system and performance planner for Consolidated Edison. “Why not give the market a vote on what scenarios go forward?”

This question seemed to confuse Lin, who said stakeholders would be able to comment on scenarios and base case assumptions during the process. Zachary Smith, vice president of system planning for NYISO, reinforced the notion that stakeholders would be involved at the start of base case development through the process.

“Ultimately this will result in the same vote that there is today in the process,” Smith said. “We document all of that in the Reliability Needs Assessment report, which goes in front of the Operating Committee and Management Committee for two separate stakeholder votes.”

Kevin Lang, representing New York City, said this missed Paszek’s point that stakeholders should have input on the scenario development process. Smith said stakeholders would be encouraged to provide feedback under the proposed process.

“The point is that we are giving NYISO all the power in this case,” Paszek said. “There is a difference between feedback and … having some real market input. There’s a huge difference.”

Another stakeholder asked whether the ISO would be able to provide calculated probabilities of the likelihood of each scenario. Lin said given the number of inputs into the calculation, this was not feasible with NYISO’s current workflow.

“We’re talking about the things that keep me up at night,” Lin said. “With large loads, for example, it’s almost impossible to say if this load is coming online with 50% likelihood or 20%. … There is very little transparency, not because NYISO isn’t trying, but because that’s just how the load centers are.”

Lin detailed how NYISO would define and consider the magnitude, urgency, severity of impact, number of scenarios and duration over the planning horizon for determining whether something constituted a reliability violation.

“It’s important to us moving ahead with any scenario planning that it is not in any way, shape or form turned into some formulaic default,” Smith said. “I want us to take a balanced approach to considering the uncertainty around demand forecasts, around generation mix, and everything else that goes into our planning.”

Dominion Energy reported earnings of $567 million for the fourth quarter and $3 billion for 2025, as executives offered updates on the firm’s offshore wind project and pipeline of data centers coming onto its system.

The Coastal Virginia Offshore Wind (CVOW) project was delayed by a federal decision that since has been overturned by the courts. Its total cost increased to $11.5 billion from $11.2 billion before the delay, the company told the Securities and Exchange Commission in January. (See Dominion Wins Injunction, Can Restart Offshore Wind Construction.)

“We’re now over 70% complete,” CEO Robert Blue said during an earnings call Feb. 23. “We continue to be on track for the delivery of first power to the grid by the end of March. That will represent a remarkable project milestone.”

The installation of monopiles went more quickly than expected, as has work around the transmission elements of CVOW, which are over 70% installed, with the rest of the equipment on-site at the Portsmouth Marine Terminal awaiting installation.

The towers are 70% manufactured, and the blades are 30% manufactured. Dominion successfully completed the first turbine in January.

“During the first few iterations, we’re deliberately moving more slowly in order to ensure we figuratively measure twice and cut once,” Blue said. “We view this as prudent construction management aligned with the lessons we’ve learned over years of large project construction.”

Once the stop-work order was lifted, winter weather added to another week of delays in the turbine installation process, Blue said. Workers are getting used to the process, as Dominion has seen in other parts of the project, and turbine installation should get easier and take less time as it continues.

While the project is expected to deliver its first power in the next month or so, Dominion’s schedule to finish CVOW runs through July 2027. That includes some expected downtime for weather, but delays will raise the budget by about $150 million to $200 million/quarter, some of which would be covered by Dominion’s financing partner, Blue said.

One analyst asked about the possibility of the federal government appealing the decision that allowed CVOW construction to resume. Blue argued that would not make sense given rising demand in Dominion’s territory.

“We continue to see CVOW as the fastest way to get a significant amount of electricity at a low-cost way [online] for our customers who are leading the AI race, who are building ships for the Navy,” Blue said. “And so, we continue to believe it just makes sense for this project to be allowed to continue. Slowing it down, as was demonstrated with the last stop-work order, adds costs. And adding costs and delays in the data center capital of the world — we think that doesn’t make sense.”

The pipeline of new data centers Dominion hopes to serve continued to grow in the past quarter.

“We now have over 48 GW in various stages of contracting as of December 2025, which compares to around 47 GW as of September, an increase of approximately 1.4 GW, or 3%,” Blue said.

That includes 10.2 GW that have signed an electric service agreement — the highest level of commitment — and 11 GW that have signed construction letters of authorization. That leaves 27.4 GW in the least certain category, which have a “substation engineering letter of authorization,” where the utility is reimbursed for detailed engineering plans.

Load growth already is showing up on its system, with 14 out of its top 20 demand days in history having occurred in the past 14 months, the company reported.

Data centers also are at issue with Dominion’s Millstone nuclear plant in Connecticut, where it continues to look for an off-taker.

“In January, the Connecticut Department of Energy and Environmental Protection issued a zero-carbon energy request for proposals for which Millstone is eligible,” Blue said. “Bids are due in the RFP in March. The Connecticut RFP process also intends to coordinate bid evaluation in conjunction with other New England states. In addition to state-sponsored procurement, we continue to evaluate the prospect of supporting incremental data center activity.”

Any deals with data centers would “need to be pursued in a collaborative fashion with stakeholders in Connecticut,” and Dominion remains committed to achieving a constructive outcome for the nuclear plant, he added.

A bill in the Colorado legislature seeks to reduce the environmental impact of federal orders delaying the retirement of coal-fired power plants.

House Bill 26-1226, introduced Feb. 18, would require utilities to report quarterly on the costs of running coal plants beyond their retirement dates. It would limit nitrogen dioxide and sulfur dioxide emissions from coal plants that are still operating in 2031.

The bill also would direct the Colorado Public Utilities Commission to approve new resources to help the state meet its 2030 climate goals.

HB26-1226 follows a U.S. Department of Energy order under Section 202(c) of the Federal Power Act to keep Unit 1 of the coal-fired Craig Generating Station operational for 90 days, which the department said was needed to prevent blackouts. The order was issued Dec. 30, a day before the unit was set to retire, as had been planned since 2016. (See DOE Blocks Retirement of Another Coal-fired Plant.)

State Sen. Mike Weissman (D) said the Trump administration was using the order “to turn years of careful planning on its head.”

“This will result in increased air pollution, higher energy costs and a delay in achieving our renewable energy goals,” Weissman said in a statement. HB26-1226 “gives the state tools to address these impacts.”

In addition to Weissman, the bill’s major sponsors are Rep. Jenny Willford, Rep. Meg Froelich and Sen. Lisa Cutter, all Democrats. The bill has been referred to the House Energy and Environment Committee.

The Sierra Club supports the bill, pointing to the costs of keeping aging coal plants running. A Grid Strategies report, commissioned by the Sierra Club and other environmental groups, found that the cost to ratepayers of keeping Craig running past its retirement date would be about $80 million/year.

“We urgently need laws like this to protect our state against the high price — both financial and environmental — the federal government is trying to foist on us,” Sierra Club Colorado Director Margaret Kran-Annexstein said in a statement.

Tri-State Generation and Transmission Association, co-owner and operator of Craig Unit 1, announced in January that it had completed repairs to return Unit 1 to operational condition. Tri-State declined to disclose the cost.

HB26-1226 would require investor-owned utilities and wholesale electric cooperatives to file a report every 90 days after a federal order to keep one of their coal-fired units running past its retirement date. The report must include capital costs and maintenance and operations expenses to keep the unit online. It also must state the number of hours the unit ran over the past 90 days, the amount of electricity generated, and the resulting amount of resource curtailment and its cost.

An IOU that owns but does not operate the coal-fired unit would report its share of the costs. The bill would allow an IOU to apply for a financing order to recover the costs of complying with an order.

DOE’s order to Craig said there is an energy emergency in the WECC-Northwest assessment area. The order pointed to projected load growth in the area paired with planned retirements of baseload generation.

Although the order expires March 30, some are concerned it will be extended.

On Jan. 29, Tri-State and Craig Unit 1 co-owner Platte River Power Authority filed a request for rehearing of the order, arguing it disrupts their “carefully considered reliability planning.” (See Fight Heats up over Colorado’s Craig Coal Plant Extension.)

Challenges to the order were also filed separately by the Colorado attorney general and a coalition of environmental groups. DOE has 30 days to respond; if it does not, the request is automatically deemed denied.

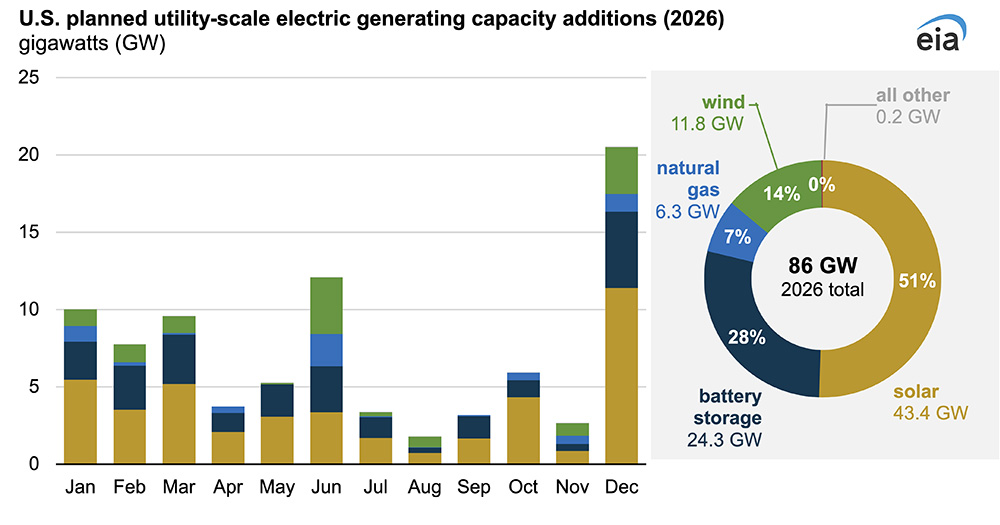

A record 86 GW of utility-scale generation capacity is projected to be added to the U.S. power grid in 2026.

The Energy Information Administration (EIA) said Feb. 20 that if the plans reported by power plant developers and operators come together as expected, they would far outpace the 53 GW of capacity added to the grid in 2025, which was the most since 2002.

Rising demand expected from new data centers and other larger loads has touched off a scramble to add power generation.

But details of the EIA analysis suggest the surge projected in 2026 is rooted at least in part in the clean energy push of the Biden administration, rather than the fossil-heavy energy dominance push of the Trump administration.

EIA calculated 43.4 GW of solar, 24.3 GW of battery storage and 11.8 GW of wind coming online in 2026, or 93% of the 86 GW total.

Just 6.3 GW of new utility-scale natural gas capacity is expected.

The U.S. Energy Information Administration breaks down by technology the expected utility-scale capacity additions to the U.S. grid in 2026. | EIA

Given the time frames involved in development, permitting and interconnection, the Biden-era surge of renewables development still is in process in the second year of the Trump administration and the Trump 2.0 push for fossil generation has not yet resulted in extensive construction.

President Donald Trump engineered an accelerated phaseout of the lucrative federal tax credits President Joe Biden engineered for solar and wind development, so there is additional impetus for renewables developers to accelerate construction of their projects.

EIA broke the numbers down by geography and technology:

The 43.4 GW of new solar would be a 60% increase over 2025.

Texas is the site of 40% of the planned solar construction; rounding out the top three states are Arizona and California, at 6% each.

The 24.3 GW of new battery capacity expected in 2026 would continue the technology’s five-year streak of exponential growth in the U.S. and would far surpass the record 15 GW installed in 2025.

Three states account for most of the new batteries expected to come online in 2026: Texas (53%), California (14%) and Arizona (13%).

Annual wind power additions have slumped since exceeding 14 GW in both 2020 and 2021; the 11.8 GW projected in 2026 would not be a complete rebound but would be more than double the amount that came online in 2025.

Four states account for nearly 60% of the wind total: New Mexico, Texas, Illinois and Wyoming.

The largest onshore wind project in the nation, New Mexico’s 3,650-MW SunZia, is expected to start commercial operation in 2026, as are the nation’s first two large offshore wind projects, the 710-MW Revolution Wind and the 800-MW Vineyard Wind 1 along the New England coast.

Combined-cycle generation accounts for 3.3 GW of the 6.3 GW of natural gas capacity expected to be added in 2026; the planned combustion turbine units total 2.8 GW.

Florida, Ohio, Oklahoma, Tennessee and Texas together would host more than 80% of the gas-fired capacity additions.

The 1,158-MW Orange County Advanced Power Station in Texas is the largest single gas addition expected in 2026.

Generation additions for all other technologies are expected to total approximately 0.2 GW.

EIA has not released full data for electrical generation in 2025.

But the most recent electric power monthly update indicates that through the first 11 months of 2025, significant changes in utility-scale generation were seen with solar (34.5% higher than the first 11 months of 2024), coal (13.8% higher) and natural gas (3.7% lower).

Also in the first 11 months of 2025, U.S. electricity consumption was 2% higher, the average price was 5.3% higher and revenue from sales was 7.4% higher.

MISO is confident that meeting spring demand should be a breeze. The grid operator said it will be able to deliver on both its coincident and non-coincident peak forecasts through May.

During a Feb. 19 Market Subcommittee meeting, MISO’s Jason Howard told stakeholders that the RTO is in “good standing” for spring.

MISO predicts a 100.2-GW load over spring under a 50-50 coincident peak forecast, while its non-coincident peak forecast calls for a 95.8-GW peak in March, an 89.5-GW peak in April and a more dramatic 107.3-GW peak in May.

MISO’s coincident peak forecast draws on load-serving entities’ load forecasts and attunes them to the entire RTO’s simultaneous, seasonal peak. The non-coincident peak forecast, on the other hand, is the peak load submitted by each load-serving entity per month considered in isolation.

The RTO indicated it should have plenty of non-emergency electricity supply under either scenario.

The grid operator’s spring capacity auction cleared 118.3 GW of offers and attracted 123.4 GW in offered capacity.

On top of that, MISO has about 15 GW in load-modifying resources available for grid emergencies. At this point, the RTO doesn’t foresee a need to use them.

Ramping Demand Curve Increase Imminent

The MSC is set to explore upping the pricing of its ramping product through changes to its associated demand curve.

The RTO hopes to stimulate much-needed up-ramping movement to accommodate a growing solar fleet that signs off in the evenings.

Senior Market Engineer Chuck Hansen said MISO hasn’t updated its reserve demand curves, including the one governing its up-ramping capability, since it increased its value of lost load. He said MISO similarly should adjust the up-ramping demand curve to better reflect how high MISO is willing to increase prices to satisfy reserve requirements.

MISO’s existing up-ramp demand curve is priced at just $5/MWh until MISO experiences a 50% ramping deficit. Then, the curve uses eight steps to top out at $31/MWh.

In MISO, it’s become cheaper for the market to “violate the up-ramp constraint than to procure and price the full requirement,” Hansen said.

MISO leadership has frequently discussed its more intense need for ramping, the thrust behind more frequent reserve shortages.

Hansen said over the past three years, MISO has experienced more instances of reserve shortages in the real-time markets. He said they most notably include real-time operating reserve shortages and day-ahead up-ramp shortages.

Hansen said 80% of intervals with real-time operating reserve shortages occurred in an hour that contained a day-ahead up-ramp shortage.

He said while there has been a more than threefold increase in day-ahead up-ramping capability shortage hours, market clearing prices have increased only 21% over the same time.

In many cases, prices don’t reflect the “reserve shortages that are imminent,” Hansen said. He said MISO should formulate prices that are high enough to incent units to be flexible and be fairly compensated.

MISO also hopes to include a deliverability component to its reserves to make sure they’re helpful.

MISO said that as congestion patterns become more active, it will need to ensure reserves can be delivered where needed.

MISO clears its ramp product on a system-wide or zonal basis to cover for load variation. But MISO’s Congcong Wang said the RTO can over-clear ramping capability in MISO South, some of which runs headlong into the 2,500 to 3,000-MW transfer limit between the South and Midwest.

MISO said it needs to manage deliverability in its ramping products so they can meet needs in a subregion. Wang said MISO should devise a way to clear ramping help behind constraints to avoid manual operator interventions such as derates or generator disqualification.

Wang said MISO will review past reserve deliverability to propose a solution.

MISO Makes DER Task Force More Permanent Group

Finally, MISO stakeholders officially disbanded the Distributed Energy Resources Task Force and reformed it into a more permanent working group.

The MSC voted by consent at the Feb. 19 meeting to form the new DER Working Group, issuing it a charter and management plan. Prior to that, the DERTF had been operating on multiple annual stakeholder votes to extend.

Stakeholders also voted in early January to give the DERTF a more stable foundation. In MISO, task forces are temporary stakeholder groups that must be renewed every year to avoid a mandatory sunset date. Working groups, on the other hand, are permanent fixtures that have a charter.

Stakeholders at the time reasoned that a longer-form committee would be best suited to discuss perennial DER topics.

Chair Zachary Callen, an economic analyst at the Illinois Commerce Commission, has said the DERTF is “outgrowing” the definition of a task force, considering the permanence of DER topics in MISO. He said while renewal doesn’t take much, MISO and stakeholders spend hours preparing documents and procedures to re-up the group year after year.

“Importantly, I think the working group is a standing entity that won’t require a renewal process,” Callen said at the DERTF November meeting.

EPA Administrator Lee Zeldin traveled to the Mill Creek coal plant in Kentucky to announce the agency is reversing 2024 amendments that expanded the scope of the Mercury and Air Toxics Standards (MATS), saying the change is expected to save $670 million.

“The Biden-Harris administration’s anti-coal regulations sought to regulate out of existence this vital sector of our energy economy,” Zeldin said in a statement accompanying the Feb. 20 announcement. “If implemented, these actions would have destroyed reliable American energy. The Trump EPA knows that we can grow the economy, enhance baseload power, and protect human health and the environment all at the same time. It is not a binary choice and never should have been.”

The reversal restores as the law of the land the 2012 MATS rule, a regulation that pushed many plants to retire, along with cheap shale gas that made older coal-fired plants less competitive in the markets.

“The Obama administration’s 2012 MATS rule was one of the biggest blows against West Virginia in the war on coal, putting an indescribable strain on our dedicated coal miners, their families and communities and our entire state,” Sen. Shelley Moore Capito (R-W.Va.) said in a statement. “The Biden administration only made matters worse when it included an even more stringent MATS rule in its package of regulations aimed at eliminating coal from our nation’s energy mix.”

The 2024 revisions to MATS established more stringent standards for non-mercury emissions from coal generators and mercury emissions from lignite-fired generators and required all generators to install continuous emissions monitoring systems for particulate emissions.

EPA said that by 2021, the 2012 MATS rule had cut mercury emissions by 90%, acid gas pollutants by more than 96% and emissions of non-mercury metals such as arsenic and lead by 81%.

“EPA has re-evaluated the 2024 final rule and, after considering public comments, finds that the revisions to the emissions standards were not ‘necessary’ because they impose unwarranted compliance costs or raise potential technical feasibility concerns,” the agency said in its repeal.

Reactions to EPA’s announcement varied, with environmental organizations lamenting that the repeal will allow coal- and oil-fired power plants to emit more brain-damaging mercury, other harmful metals and soot. That pollution puts the public at greater risk of cancer, premature deaths, and heart and lung disease, according to a joint statement from the Clean Air Task Force, Earthjustice, Environmental Defense Fund, Environmental Law & Policy Center, Natural Resources Defense Council and Sierra Club.

The eliminated requirement to install monitoring systems on power plants deprives communities of a powerful tool ensuring that the facilities comply with emissions standards, they added.

“This repeal is an unprecedented, unlawful and unjustified reversal that flies in the face of congressionally mandated efforts to reduce hazardous air pollution from industrial facilities,” Clean Air Task Force attorney Hayden Hashimoto said in a statement. “EPA’s repeal puts polluters’ interests over public health by loosening the limits on emissions of air toxics from power plants, which the agency has previously recognized as the largest domestic emitter of mercury and other hazardous air pollutants. Allowing more emissions of air toxics puts Americans at greater risk for the benefit of a small number of particularly dirty coal plants.”

Coal trade group America’s Power welcomed the reversal, saying it will help power plants stay online at a time when they are needed for reliability. More than 55 GW of coal generators are currently scheduled to retire in the next five years as demand continues to rise, CEO Michelle Bloodworth said.

“In combination with other EPA rules, the 2024 MATS rule would have helped accelerate coal plant retirements, ignoring the critical role these facilities play in providing dependable, baseload power,” she added. “Utilities have already invested more than $2.5 billion to comply with the original 2012 MATS rule, and the 2024 update would have required roughly $1 billion in additional costs that ultimately would have been borne by ratepayers.”