DTE Energy is weeks away from finalizing an additional power agreement for a large-scale data center, even as friction continues over its deal in late 2025 to supply 1.4 GW to a $7 billion facility under construction.

The Michigan energy company provided the update with its fourth-quarter and full-year financial report Feb. 17.

DTE President Joi Harris emphasized there would be no downside for existing ratepayers as she highlighted the benefits that would accrue to the utility and its shareholders from the agreement to power the data center that Oracle and its partners recently began building on farmland south of Ann Arbor.

While the company’s 2026 financials are solid and are expected to improve with these and other data center agreements, financial analysts on the call asked about the potential negative effects of data center deals.

The Pushback

Michigan has become a flashpoint in a rapidly evolving discourse that has put Big Tech on the defensive in a matter of months.

On the same day DTE announced its results and its plans, The New Republic published an overview with a headline that concisely summed up the sentiment: “Data Centers Are the Enemy We’ve All Been Waiting For.”

The article was national in scope but made special mention of Michigan, where data center moratoria proposals are proliferating. Politicians and grassroots groups have been fighting against the Oracle-backed data center that will run on up to 1.4 GW of power supplied by DTE.

To submit a commentary on this topic, email forum@rtoinsider.com.

Bridge Michigan recently reported that all 11 of the people publicly vying to replace Gretchen Whitmer (D) as governor want to protect Michiganders from the negative effects of data center development, and some propose to do this by limiting construction.

In another example of how quickly the narrative has turned against Big Tech and its data centers, it was only in early 2025 that Michigan attempted to attract data center development by extending and expanding tax exemptions.

The Michigan Public Service Commission approved DTE’s contracts for the new Saline Township data center (Case No. U-21990) on Dec. 18 over the objections of state Attorney General Dana Nessel and consumer advocates. (See Michigan PSC OKs DTE Energy’s 1.4 GW Data Center Contract, AG Pans Process.)

Nessel is not finished. On Jan. 20, her office filed a motion to reopen the proceeding on the grounds that DTE did not accept the conditions the PSC attached to its approval.

DTE replied Feb. 6 that it had, in fact, accepted the conditions. Nessel’s motion to reopen the case does not meet legal standards for reopening, it said, adding that the attorney general and others submitting motions are not parties to the proceeding and may not seek to reopen it.

The Message

In its Feb. 17 news release, DTE celebrated its “landmark” first hyperscale data center contracts and noted their benefits to the community.

Also Feb. 17, Oracle Senior Vice President Josh Pitcock explained in a news post how the company expands its global network of data centers, which as of late 2025 numbered 147 online and 64 being built. His headline: “Designing Data Centers for the Communities and Natural Environments Where We Operate.”

Both messages are part of what now is being called a scramble to redirect the national discourse to what data centers will do FOR Americans, rather than TO Americans.

In early 2026, The New York Times, Grist, Bloomberg, POLITICO and others have declared a public relations blitz is underway by Big Tech and some of its partners in other sectors, trying to change the message.

But all the arguments for and against expanding data center infrastructure and the artificial intelligence computing revolution it will enable seem to have become secondary to one concern in the mind of Middle America and the politicians angling for its vote:

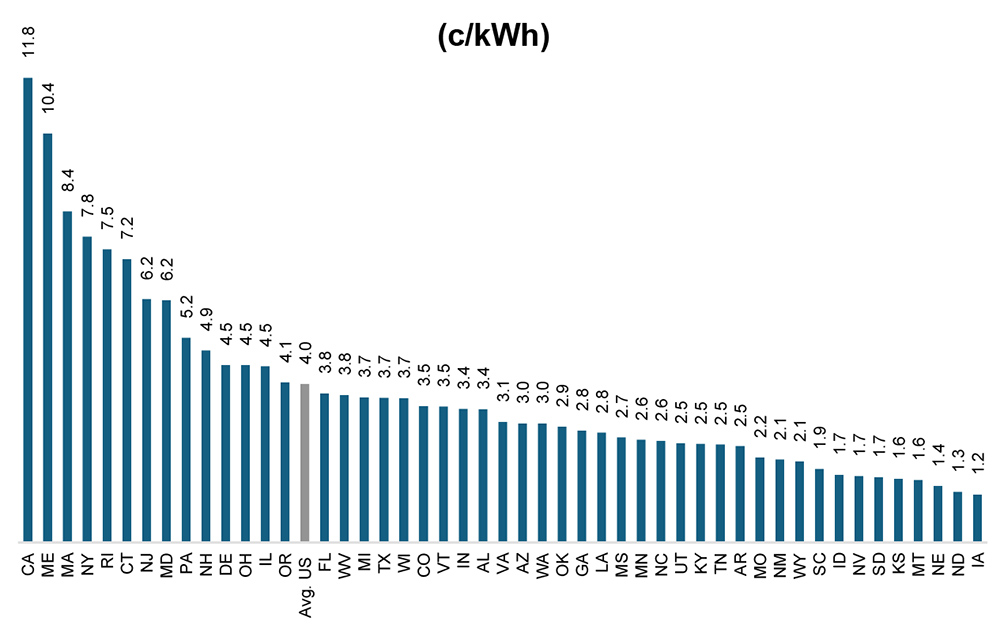

The voracious electrical appetite of these facilities could further boost retail electrical costs that already are climbing at a rate far greater than most other consumer costs and most household incomes. (See Electricity Rates are the Political Livewire Threatening the Industry.)

Boom.

The jobs that data centers might support or create someday, the competitive advantage they might provide to America, the effects they might have on water and air, the quicker or more accurate or more clever computing they might deliver — none of these seem to be as tangible as the bill that comes due each month and has become egregiously large in parts of the United States this winter. (See U.S. Utility Rate Increase Requests Topped $30B in 2025.)

The industry response has been for data centers to propose bringing their own power or for utilities to write contracts that remove financial risks from other ratepayers, as DTE stressed it is doing.

How effective either strategy is at protecting ratepayers depends heavily on the details. The Michigan PSC indicated Dec. 18 and DTE affirmed Feb. 17 that those details are all buttoned down.

But Nessel yellow-flagged an aspect of the case that other consumer watchdogs have complained about elsewhere: The proceeding moved quickly and was not fully transparent, and some details of the contract were redacted. (See Report Faults Utilities on Data Center Planning.)

The ratepaying public and its advocates, in other words, must take the parties at their word.

The Response

The Michigan PSC conditioned its Dec. 18 approval of the DTE-Oracle contracts on requirements including:

-

- Boosting the minimum term of contract from the standard five years to 19 years.

- Billing a minimum of 80% of the contracted electrical use, even if actual usage is lower, instead of the standard 50-60%.

- Making a termination payment of up to 10 years’ worth of minimum billing.

- Assigning to DTE responsibility for any costs it cannot recover from Green Chile Ventures, the Oracle-backed LLC behind the Saline Township data center.

Harris mentioned the ratepayer protections baked into the contract agreement during the conference call with financial analysts Feb. 17.

She also said the 3 GW of additional hyperscale data center demand in late-stage negotiations could drive the compound annual growth of DTE’s earnings/share above 8%/year in 2027-2030.

Three to 4 GW of data center load is in earlier-stage discussions.

DTE will use existing infrastructure to cover the Saline Township facility as it ramps up to 1.4 GW, and the utility will add new storage in a peak-shaving role at the data center’s expense.

Another hyperscale contract could be announced shortly, but there is not enough existing capacity to power it, Harris said: “This next data center agreement will require a combination of new generation and storage resources, providing significant capital upside to our plan.”

Harris offered other details and thoughts on data centers in DTE’s business plan and in Michigan. They are summarized here:

-

- By the second or third quarter, DTE will be able to say how much capital it is putting into the plan.

- DTE plans to propose a large load tariff for PSC approval, and it could govern future agreements with hyperscalers, but it would be too late for the second data center, now in final-stage negotiations.

- All discussions with data center developers emphasize that no costs will be borne by existing customers.

- The Oracle project, at full operation, should benefit existing customers to the tune of $300 million/year.

- Details about the Oracle facility and other projects will be included in the integrated resource plan submitted to the PSC in the third quarter of 2026.

- The areas in Michigan where data center moratoria are being proposed or imposed are not suitable for large load data centers to begin with; no moratorium is in effect in Saline Township, where construction has begun.

- The developers DTE is talking with have been through local regulatory processes and are engaging local communities, which is a key to influencing local sentiment.

- DTE will need a large, dispatchable 24/7 resource when it retires its 3.3-GW coal-fired Monroe Power Plant, and that means combined-cycle gas turbines with carbon-capture capability.

- Given the lead times in meeting the expected growth, DTE has taken steps to get in the MISO queue and has placed down payments on gas turbines.

Harris tried to strike a balance on the commotion surrounding data centers like the one DTE will power in Saline Township:

“DTE is always committed to a bipartisan approach from policymaking … obviously, affordability is a top question on the campaign trail, and we take it very seriously for obvious reasons.”

She added that monthly electric bills are not the only financial metric by which to measure data centers’ impact.

“The biggest lever we have to address affordability is economic development that comes with load growth done right,” Harris said. “And case in point, the Oracle deal is going to yield $300 million worth of affordability benefits once they reach their full ramp.”

The development partners expect their 1.65-million-square-foot data center, part of the Stargate initiative, to create more than 2,500 construction jobs and more than 450 operational jobs on site, plus 1,500 jobs across the county and thousands more elsewhere.

DTE reported 2025 earnings of $1.53 billion or $7.36/share, up from $1.42 billion or $6.83/share in 2024.