Higher prices under Ontario’s renewed market are causing heartburn for mines and greenhouse growers, stakeholders told IESO on Nov. 26.

During the ISO’s quarterly market briefing, IESO officials said the market is performing well, with “intuitive price formation,” and that no new “high-priority defects” have been discovered since their last briefing in August. (See Ontario Nodal Market Nearing ‘Steady State’ After Nearly 4 Months.)

“We’ve now got about six months of operating in the renewed market behind us and … I think everybody’s learning and building their understanding of the new market dynamics that we’re seeing as we shift through each season,” said Candice Trickey, IESO’s director of market readiness and customer experience. “Overall, [based on] everything I hear from you and that I see internally, we are all making, collectively, really good progress in working in this new system.”

However, several stakeholders said they are facing challenges from higher prices since the new market launched May 1.

Alain Cote of Vale Canada — whose five mines and other operations use about 200 MW per hour — said Ontario Zonal Prices in November have risen from about $50/MWh to about $80/MWh in November.

“I’m just having a hard time … forecasting that,” he said. “It’s a big swing.”

Consultant Stephanie Freund, who advises commercial greenhouse companies in southwest Ontario, said her clients have seen increasing price spikes since October, when they turn on their grow lights to nurture winter crops.

“They are really struggling … trying to keep up with the day-ahead [market] in order to manage their lighting schedules … to avoid the spikes,” Freund said. “They’ve never seen such high electricity prices as now. … They won’t be able to afford running” the lights. She asked if IESO had tools to help them manage the volatility.

Darren Matsugu, IESO’s director of markets, said Ontario is seeing higher prices because it is the peak of the fall maintenance outage season. “We are definitely in the period where we have the most resources on outage to make sure that we have that availability before the winter,” he said. He suggested Freund talk to the ISO’s customer relations team about ways to manage the high prices.

Cal Brooks, of FirstLight Power, said that — even accounting for inputs like gas prices and system load — prices appear to be higher than under the Hourly Ontario Energy Price (HOEP), which the ISO used before the Market Renewal Program introduced nodal pricing and a financially binding day-ahead market.

“Do you see that as … something good in that maybe real supply and demand signals are now being reflected in a way they weren’t under the old market?” Brooks asked.

Matsugu noted that the HOEP uniform clearing prices did not include congestion and losses, which now are reflected in LMPs.

“The structural changes that we put in place are to better align the price signals we’re sending with the underlying system conditions,” he said. “Those system conditions are continuing to change. We are getting into tighter and tighter conditions than we have before, and so certainly we would expect that … the underlying prices [would] be higher.”

The ISO says the new market will produce net cost savings for consumers by reducing out-of-market payments and improving the efficiency of scheduling resources.

“I think we are seeing the benefits, particularly when we talk about our intraday unit commitment and our day-ahead commitment,” Matsugu said.

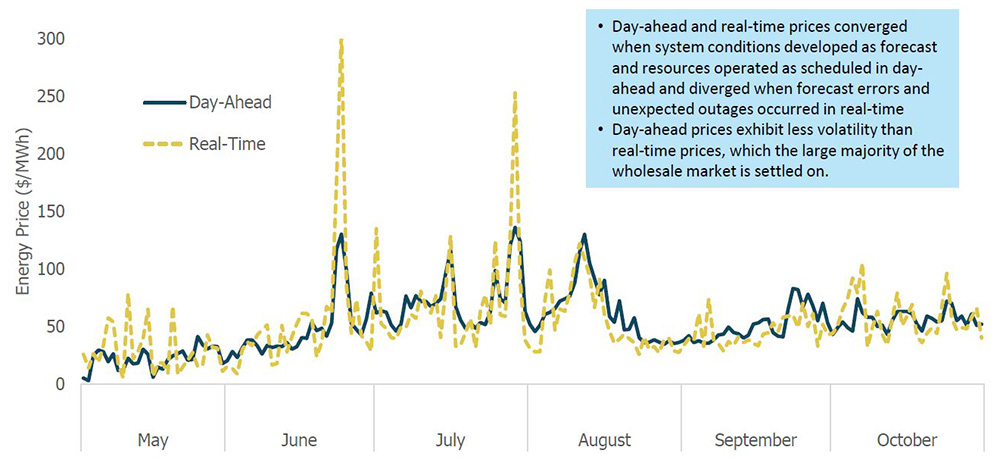

IESO officials said market prices have reflected system conditions, with real-time and day-ahead prices converging when actual conditions match forecasts and varying with deviations in real time.

Jennifer Jayapalan, of Workbench Energy, said her company has seen big changes in how some resources are being used. “We’ve seen a lot more demand response activations, not just in peak conditions, but also into the fall and as recently as the last week or two,” she said. “And we’re seeing a lot more operating reserve [OR] activations across this period as compared to really all years prior to MRP. And neither of these two actions are really publicly reported anywhere by IESO, and both are quite expensive.”

Matsugu said scheduled generation outages contributed to the DR and OR activations and that the ISO will consider whether it can provide more transparency on such actions. “We don’t have, necessarily, all the same resources available that we had during our peak of the summer, but we do that outage planning to correlate with the expected levels of demand.”

Defect Caused Demand Fluctuations

Trickey said the ISO investigated whether a defect that was causing demand fluctuations had an impact on hourly DR activations and concluded it did not create any inappropriate activations.

The defect caused the Ontario demand values published in IESO’s Realtime Totals Report to change by hundreds of megawatts for only a few five-minute intervals.

Because of the unpredictable nature of variables such as supply disruptions, sudden increases in heating or cooling demand, and neighboring system conditions, there often are changes in demand from one interval to the next. But “swings of several hundred megawatts for only a few intervals have historically been quite rare,” the ISO said in a presentation.

The summer brought higher demand, higher prices and greater price separation between day-ahead and real-time markets. | IESO

IESO said it identified a calculation that overstated demand when hourly DR resources are on standby. The ISO has implemented a manual workaround to counter the defect pending a permanent fix.

Without the workaround, the defect could result in incorrect prices for impacted intervals and incorrect peak demand hours for the Industrial Conservation Initiative if they occur on a potential peak day. ICI participants pay their share of Global Adjustment charges based on their peak demand factor, which is calculated based on their contribution to the top five peak hours over a year.

IESO identified 38 intervals with incorrect prices and corrected them with administrative prices. It confirmed that the top 10 peaks posted on the Peak Tracker webpage were not affected.

Settlements, Defects

IESO officials said they have improved settlement processing times, and that statements and invoices issued in October and November were delivered ahead of the ISO’s 5 p.m. goal.

Trickey said the new market is producing much more data “and that was taking longer to process than ideal. So we’ve been working on improvements.”

Of the settlement disagreements that have been resolved, the ISO said about 30% have been attributed to defects that have been corrected, with the remaining 70% of disputed statements confirmed as correct.

IESO continues to work through a backlog of disagreements, some of which are related to pending defect fixes. The ISO is notifying participants if there are delays in correcting settlements because of the pending fixes.

IESO officials said they had discovered several minor defects since August, including scenarios in which non-quick-start resources operating in combined cycle mode are receiving after-the-fact settlement mitigation calculated using the single cycle mode reference level.

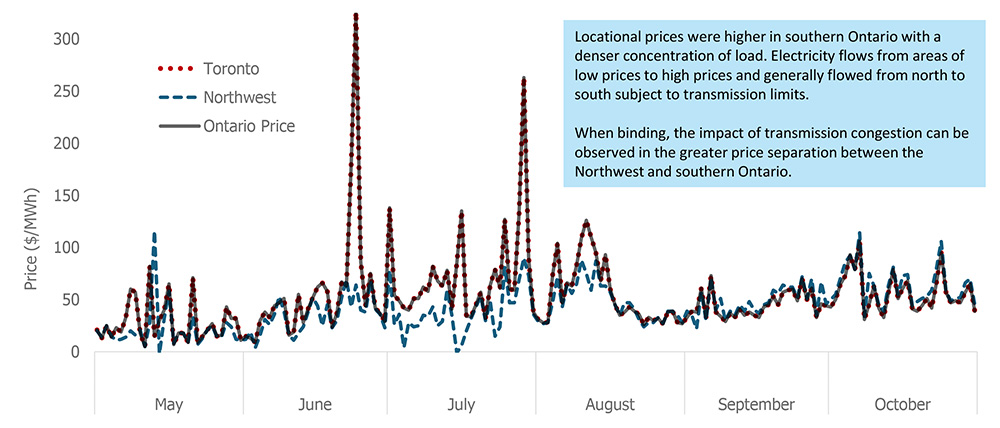

LMPs are similar throughout Ontario when there is little congestion. When demand — and congestion — is higher, as in summer, prices separate between the Northwest and the rest of Ontario. | IESO

The ISO also disclosed economic operating point (EOP) errors that may result in adjustments to real-time make-whole payments (MWPs) in resettlement statements posted on Nov. 17 and Dec. 12. EOPs reflect the output a resource could have achieved based on its physical capabilities and LMP, under actual market conditions.

The impact of the resettlements will be small, “because they’re all fairly specific scenarios impacting just certain types of resources,” Trickey said.

Trickey said IESO will continue its quarterly briefings on the Renewed Market’s performance for the first year of operation.

In response to requests from market participants, the ISO is creating a new group, the Renewed Market Advisory Forum, to discuss ways to improve the market.

Trickey said the group will focus on incremental improvements, not “long-term, evolutionary” changes.

“We’ve implemented this new market. Is everything working the way we thought it would, or as effectively as we hoped?” Trickey explained. “And if we’re seeing some gaps — whether it’s information that people need, or some parts of the system that aren’t working as well as we hoped — this is where we would like to have those kind of conversations with participants that are really engaged in the market.”

Candidates interested in participating should submit expressions of interest by Dec. 19 to engagement@ieso.ca.

Load growth beyond PJM’s ability to serve is a clear and present danger to the reliability of the grid and the functioning of PJM’s markets. After stakeholders tried and failed to meet this challenge, it falls on PJM’s board to solve.

The politics around this are complex, but the answer is clear: The board’s duty is to protect the power grid and the 67 million people who depend on it. This requires decisive action. Putting off the problem or relying on hope are not options. (See PJM Stakeholders Reject All CIFP Proposals on Large Loads.)

Claire Lang-Ree

The sudden explosive growth of data centers might promise to add more load every year than PJM has added in the past 20. Persistent yearslong delays in getting new electrical generation online due to difficulties with the queue, supply chains and construction leave a sobering outcome.

PJM will barely meet reliability standards in 2026 and almost certainly will fall below them in 2027. The capacity market is pegged at its price cap with no prospect of relief. While the flood of new data centers overwhelms the trickle of new generation, things will only get worse.

In a way, the dire situation makes the board’s decision easy. The only way to keep PJM reliable is to hold back the flood. There are a few ways to do that.

Possible Solutions to Demand Growth

The Independent Market Monitor has proposed the direct approach of not letting data centers connect to the grid until supply is available.

Whichever solution the board chooses first and foremost must prepare for the possibility PJM won’t have enough power to promise it to everyone who wants it. Physics leaves no room for compromise.

Other proposals before the PJM board have helpful components. State governors proposed a package of incentives for data centers to support the grid. Many point to the old bugbear of speculative data centers in the hope that more rigorous forecasts can shrink the problem.

These are encouraging, and we hope they work out. But these are just hopes. Hope may be the currency for poets and politicians, but it’s poor coin for engineers and economists. While the board should support every fair chance for a positive outcome, its duty is to prepare for the worst.

Capacity Price Relief Needed

The PJM board’s solution must include capacity price relief. The prices coming out of the reliability pricing model (RPM) right now serve no purpose. Thanks to delays, high prices won’t stimulate new entry in reasonable time frames. Nor are high prices needed to prevent retirements.

We’re coming off a six-year run of prices under $200/MW-day. It’s silly to argue that plants will retire if they can’t get paid double that. No matter what RPM does, any power plant that can make a spark should be able to name its price to tech companies.

The capacity market is being asked to do a job entirely outside what it was designed for, and it’s failing in a way that transfers tens of billions of dollars from the public to lucky generation owners who already were comfortably profitable. Those owners should be thinking about geese and golden eggs.

Avoid Two-tiered Queue System

One thing the PJM board should not do is enable any kind of fast track for new generation that harms projects that already are waiting in the queue.

For many years, PJM has been telling projects — including some required by state law or supported by federal policy — to wait in line. It would be unconscionable for PJM to reverse itself now and let projects that support data centers jump to the front of that line.

This threatens to create a permanent two-tier interconnection system, with one level of service for power plants that support data centers and second-class service for clean energy. PJM stakeholders rejected those concepts, perhaps remembering that open access and fair competition are one of the reasons PJM exists in the first place. The board should do the same.

There’s still room for improvement on interconnection. ERCOT has kept up with the data center boom in Texas in part thanks to their “connect and manage” approach, where new power plants join the grid as-is, accepting the risk that sometimes the transmission system might not be able to deliver their power. PJM should consider reforms like this. But no matter what PJM does on interconnection, no state should tolerate its clean energy laws being treated worse than tech companies’ commercial interests.

PJM requires independence from its board members. Nobody with conflicts of interest that could influence their objectivity is even eligible to serve.

This is for good reason. The board makes final decisions on vital issues for the power grid, often with billions of dollars at stake. There are 67 million people who rely on PJM making independent, objective decisions, even when those are unpopular or painful to some. Now is the board’s chance to justify this confidence.

Tom Rutigliano is senior advocate and Claire Lang-Ree is advocate for the Sustainable FERC Project at the Natural Resources Defense Council.

FERC has approved a transmission security agreement between PECO Energy and Amazon for a data center planned in Falls Township, Pa. (ER25-3492).

The data center is among the first in a $20 billion pool of investments Amazon announced it is making across Pennsylvania. It would not be co-located with any generation and would receive retail service under a schedule approved by the Pennsylvania Public Utility Commission, FERC said in an order issued Nov. 21.

The agreement includes a set of provisions intended to prevent costs associated with the interconnection from being shifted to other customers if the data center does not materialize. It lays out a ramp schedule on which the load is expected to come online, with shortfall payments if those milestones aren’t reached and termination fees if the load is permanently reduced. There is a committed revenue contribution that sets the baseline Amazon must pay, equal to 80% of what a load-serving entity would pay to serve 80% of the monthly load and billing — though that is subject to a customer shortfall event liability cap.

Monarch Energy Development and Constellation Energy argued the agreement should be considered on its own and not as setting precedent on other large load interconnections. The former said there are parallels between the agreement and a pending proposal from Commonwealth Edison seeking to require large loads to obtain a TSA.

Monarch also encouraged the commission to explore whether the PECO-Amazon agreement adheres to cost-causation principles, overestimates the risks large loads present to other customers and conflicts with the federal government’s goal of developing the infrastructure needed to support artificial intelligence.

The PJM Independent Market Monitor argued the agreement should not be approved unless it could be demonstrated that the data center would not adversely impact transmission reliability and resource adequacy. It also faulted the agreement for not considering the implications for energy and capacity market costs the added load could present for customers across PJM.

Throughout PJM’s Critical Issue Fast Path (CIFP) process focused on large load interconnections, Monitor Joe Bowring held that the RTO should not be obligated to accept load it cannot serve reliably, a stance the IMM extended to LSEs in comments on the TSA.

“Despite the protections included in the TSA, it is not just and reasonable to allow the interconnection of this large new data center load when it has not been demonstrated that either PECO or PJM has the capacity available to reliably serve this load,” the Monitor wrote.

It also filed a complaint against PJM on Nov. 25 arguing that its CIFP proposal would require it to accept large load interconnections it cannot reliably serve, degrading the quality of service for existing customers while imposing higher costs (EL26-30).

The commission determined the agreement can be limited to ensuring that Amazon contributes to PECO’s transmission revenue requirement without needing a demonstration that the load will not affect reliability.

“Given that the IMM raises no issue with the terms of the transmission security agreement itself, but rather raises concerns with the provision of service to the data center under PECO’s retail tariff and the provision of transmission service to large loads generally, the IMM’s concerns do not provide a basis upon which to reject the transmission security agreement,” FERC wrote. “We also note that the Pennsylvania commission retains authority to establish terms of retail service between Amazon and PECO, including retail consumer protection provisions.”

Commissioner Judy Chang concurred, writing that the agreement includes some consumer protections and recognition of state authority over retail rates, while urging the commission to develop a comprehensive framework for assigning transmission upgrade costs.

As large load interconnections with significant impacts to the grid become more common, she said the commission’s “higher of” policy could serve as a framework for determining how those costs could be allocated. Under that model, large loads pay the greater of the embedded or incremental cost rates, which she wrote would ensure that a large load pays for network upgrades it triggers.

“It may be time for the commission to proactively consider how to guarantee sufficient customer protections, such as the ‘higher of’ pricing policy, to ensure that we do not outsource our customer protection responsibility to bilateral agreements by the utilities we regulate,” she wrote.

She wrote it’s especially important for agreements between utilities and large customers to recognize the contours of state jurisdiction, particularly when the Mobile-Sierra public interest standard of review is applied, as in the PECO and Amazon agreement.

“Given the potential magnitude of new transmission investment triggered by large load additions, concerns about costs are increasingly spilling into commission proceedings, raising complicated jurisdictional and policy questions with significant implications for both state and federal regulators,” she wrote. “This critical affirmation will help ensure that the commission’s acceptance of the agreement and possible similar agreements in the future recognizes and preserves states’ essential role in protecting retail customers.”

The Virginia State Corporation Commission trimmed Dominion Energy’s rate increase and approved its plan to create a new rate class for large load customers like data centers.

In an order issued Nov. 25, the SCC approved the new GS-5 rate class to become effective Jan. 1, 2027. The new class will help insulate other customers from the rapid buildout of infrastructure needed to serve new data centers, the commission said. Any customers with demand of 25 MW or greater and a load factor of at least 75% will go into GS-5.

Customers in the new class will sign electricity service agreements that last 14 years. If they leave Dominion’s service early for a competitive service provider (CSP), they will have to pay an exit fee that covers 85% of the contracted demand’s distribution and transmission costs and 60% of its generation costs.

“Dominion must consider aggregate forecasted demand over a long-term planning period, must plan to meet those needs with supply resources that typically require many years to develop, and must construct generation to be ready to serve high load customers who are eligible to select a CSP in the future,” the SCC said in its order. “Accordingly, the commission finds that the minimum generation demand charges shall apply to these new shopping customers.”

That will reasonably recover the costs of infrastructure Dominion built to serve such customers even if they retire early, the commission said.

GS-5 customers can reduce their capacity during the ESA term by up to 20% at no cost and an additional 30% if another customer agrees to assume the associated capacity. Each capacity reduction requires a 36-month notice.

The SCC also rejected Dominion’s requested base rate increases of $822 million for 2026 and $345 million for 2027, instead approving $565.7 million in 2026 and $209.9 million in 2027. Those translate into $11.24 more on a typical residential customer’s bill in 2026 and $2.36 more on monthly bills in 2027, which are 23.7% and 51.2% lower than what Dominion had requested, respectively.

The SCC also approved a higher return on equity for Dominion, raising it from 9.7% to 9.8%, which is below the 10.4% it requested.

“As the utility regulator, we are obligated by law to set a revenue requirement that affords the company an opportunity to recover reasonable and prudent projected costs and earn a reasonable rate of return,” the SCC said. “In this case, that has resulted in an increase in rates, but not to the extent requested by Dominion.”

In another order issued Nov. 25, the SCC approved Dominion’s Chesterfield Energy Reliability Center (CERC), a 944-MW natural gas plant made up of four GE Vernova 7F combustion turbines. The turbines will be built in the footprint of a retired coal plant and alongside two existing combined cycle power plants.

The plant is the first natural gas-fired generator that the SCC had to evaluate since the Virginia Clean Economy Act was passed in 2020. Dominion said it was needed to keep pace with demand growth. The plant will cost the average residential customer 60 cents on their monthly bill.

“This case therefore is not about choosing CERC over compliance with the VCEA (or CERC versus renewable generation, demand-side management or batteries, for that matter). Instead, the commission is called upon to determine whether a ‘threat to the reliability or security of electric service to the utility’s customers’ exists, such that the CERC project is required to obviate such threat,” the SCC said in its order. “As discussed herein, the evidence in this case clearly establishes that there is an imminent reliability threat for Dominion and its customers and that the CERC project addresses that threat in a manner that is in accordance with the public interest and the VCEA.”

While the commission acknowledged that some of the forecasted load growth for Virginia and the rest of PJM may be overstated, it also said the demand for power is certainly on the rise. It cited the spiking capacity prices in the RTO, as well as NERC reports that PJM could run short of reserves in extreme weather in the second half of this decade.

The CERC order was opposed by environmental groups including Clean Virginia, which called the approval disappointing.

“Despite major flaws in Dominion’s application and planning process, the commission granted approval to a gas plant that breaks Virginia’s commitments to clean air, further drives up electric bills and which would not be necessary absent the gluttonous energy demands of Big Tech companies,” Executive Director Brennan Gilmore said. “If this is the decision the commission came to under existing rules, then it is upon Virginia’s elected leaders to better align these rules with the interests of all Virginians.”

Citing developments within the Western Power Pool’s Western Resource Adequacy Program, the Oregon Public Utilities Commission waived penalties for electric service suppliers participating in the state’s alternative RA program.

The three-member commission voted Nov. 25 in favor of staff’s recommendation to grant a waiver for electric service suppliers (ESSs) that make filings in Oregon’s state resource adequacy program and directed staff to work with the PUC’s Administrative Hearing Division to decide whether to open a rulemaking or investigation to consider amendments to RA rules.

ESSs are the product of Oregon’s electricity restructuring law, which gave non-residential customers the option to purchase energy from independent PUC-certified suppliers rather than their utilities through the state’s direct access program.

The PUC’s vote came after the Northwest & Intermountain Power Producers Coalition filed a motion asking the commission to consider the waiver because of developments within WRAP, which impacted Oregon’s separate RA program.

Entities not part of WRAP must participate in the state’s RA program, which is modeled mostly on WRAP, except it does not have specified penalties. Those instead are determined by the commission, according to a staff memo.

The commission previously waived penalties for the 2025-2027 compliance period after WRAP delayed its first binding period. Until the recent vote, no waiver existed for the 2027-2029 cycle, but the commission approved one in response to recent WRAP developments.

WRAP participants had until Oct. 31 to commit to the program’s binding season beginning in winter 2027/2028. Citing concern about the program’s readiness, Oregon-based utilities PacifiCorp and Portland General Electric exited, along with Calpine Energy Solutions, which operates as an ESS in the state. (See WRAP Wins Commitments from 16 Entities.)

The entities could choose to rejoin WRAP, but if they do not, they must demonstrate compliance with Oregon’s RA requirements unless another regional RA program becomes available.

In light of these developments, NIPPC asked the Oregon PUC to provide clarity by adopting a penalty framework for the state RA program and adopting an alternative compliance pathway for ESSs.

NIPPC said ESSs are struggling to meet both WRAP and state RA requirements, in particular because of difficulties procuring transmission rights from third-party transmission providers and rights holders.

“[NIPPC] said that uncertainty about ESSs’ ability to comply with requirements or reasonably limit penalties for non-compliance in either WRAP or the state program could irreparably harm the direct access (DA) market by leaving DA customers with ‘no reasonable choice’ but to provide notice to their incumbent utilities of their intent to return to cost-of-service rates,” according to the memo. “Although WRAP and state program penalties are not scheduled to apply until 2027, NIPPC stressed the urgency of its first request, that the commission clarify state program penalties, noting that DA customers must typically provide at least two years’ notice to return to their incumbent utilities.”

In response to NIPPC’s motion, PUC staff said it “believes there is good cause for the commission to waive [RA penalties] for ESSs for the next state program compliance process. This waiver would remove the requirement for the commission to make a compliance determination on ESSs’ forward showings and the firm requirements related to remedies and penalties.”

Staff added that the waiver should give it enough time to investigate and consider changes to the state RA program.

Staff also provided a five-point checklist for what it believes the commission should accomplish moving forward:

Provide load-serving entities with near-term clarity about state RA requirements and consequences of noncompliance.

Ensure, to the extent possible, non-preferential treatment between ESSs and utilities and fair treatment between participants in the state RA program and those in WRAP.

Minimize disparities between available RA programs while also incentivizing participation in a regional RA program.

Ensure the commission maintains visibility into the RA positions of LSEs and the potential for impacts on all retail customers.

Ensure compliance with state program requirements is feasible and incentivized by the program’s design.

‘Ensuring Reliability and Competition’

Stakeholders participating in the meeting backed staff’s recommendations.

Marie Barlow, an attorney with NewSun Energy, said the organization supports the efforts.

“We just want to emphasize that the goal for the resource adequacy and the direct access programs should remain focused on ensuring reliability and competition,” Barlow said. “The outcome that we absolutely do not want is for the direct access program to collapse under the weight of those resource adequacy obligations, resulting in those loads returning to the utilities and further burdening those utilities with their greenhouse gas reductions obligations and additional reliability obligations, especially at a time when they’re already going to be burdened with rapidly increasing loads.”

Other organizations and companies also voiced their support, including PGE, PacifiCorp and Calpine.

PUC Chair Letha Tawney noted that the vote does not mean there will be no RA obligations for ESSs and that most parties appear to agree they should continue to present forward showings.

“I think there may be interim data requests that staff will have to request and ESSs might need to be responsive to,” Tawney said. “As we go forward through this time frame, it might be that every … 24 months showing is sort of sufficient given how dynamic the space is. But I’m hearing an openness to that dialog, and I appreciate that.”

A new report examines CAISO, MISO, PJM and SPP efforts to accelerate interconnection queues and concludes that while some may succeed in speeding generation additions, some sacrifice fairness, transparency and open-access principles.

Early evidence suggests these emergency mechanisms produce portfolios heavily weighted toward thermal resources that potentially face high network upgrade costs, according to the analysis performed by Grid Strategies for the American Council on Renewable Energy.

The ACORE report warns that these programs are labeled as one-time measures but could be extended or repeated. Instead of that, the authors urge a long-term strategy that upholds open access and competition, and they propose two paths to this goal:

An Enhanced Readiness Fast Lane — a narrowly tailored, transparent pathway for projects that address verified near-term reliability needs, activated only under specific conditions and governed by transparent, objective and nondiscriminatory criteria.

Proactive Integration with Transmission Planning — a restructured baseline queue that aligns project intake with available and planned transmission capacity, using scoring systems to prioritize commercially ready and policy-aligned resources.

ACORE released “Interconnection Queue Rationing Reforms” on Nov. 25. The authors acknowledge that while priority interconnection processing can be designed to uphold the open-access principles that are the cornerstone of competitive wholesale energy markets, many such efforts fail to meet this ideal.

“Discriminatory queue processing undermines fair competition among technologies and interconnection customers,” they write, “introducing regulatory uncertainty that ultimately harms consumers.”

The report drills down on four efforts:

CAISO’s Interconnection Process Enhancements;

MISO’s Expedited Resource Addition Study;

PJM’s Reliability Resource Initiative; and

SPP’s Expedited Resource Adequacy Study.

All were implemented after FERC Order 2023 directed a shift from the first-come, first-served approach to queue management to first-ready, first-served.

The driving factors for the changes are well known: The U.S. interconnection queue has grown to more than 2.3 TW of potential capacity, interconnection timelines have grown to more than five years on average and fewer than 20% of queued projects reach commercial operation. Meanwhile, power demand is expected to grow significantly, costs are increasing and the supply chain to build all this capacity is bottlenecked in places.

The authors say Order 2023 produced only modest changes, but early evidence suggests grid operators’ reforms beyond the order have begun to streamline and speed queue processing, and show great promise.

The authors take a critical view of the emergency rationing mechanisms being implemented and say the RTOs and ISOs should give their reforms enough time to work before resorting to emergency measures.

“Queue rationing mechanisms like these should not become the default operating model or a substitute for comprehensive reforms,” the report states. “As a guiding principle, grid operators should exhaust all other alternatives that make the standard interconnection queue more effective before invoking new emergency rationings.”

Rationing measures are drawing legal challenges, with environmental groups recently filing suits against the MISO and SPP processes in the D.C. Circuit Court of Appeals, arguing the programs are unjustly preferential by allowing primarily fossil fuel generation to jump queues while ratepayers are billed for the upgrades needed to accommodate it. (See Enviros Challenge MISO, SPP Queue Express Lanes.)

The authors draw a distinction between the temporary fast-track programs MISO, PJM and SPP adopted and the permanent restructuring CAISO undertook.

CAISO’s changes were not without controversy, they write, but “on balance, CAISO’s IPE represents one of the most comprehensive queue reforms among system operators to date.”

Nonetheless, timelines remain extended, the percentage of projects advancing remains low and transmission constraints continue to strand low-cost energy potential.

“The upcoming refinements under IPE 5.0, particularly around energy-only conversion, long lead-time upgrades and equitable scoring oversight, will determine whether CAISO can transform this framework into a sustainable, scalable model for integrating the volumes of clean energy required to meet California’s 2030 and 2045 goals,” the authors write.

FERC has dismissed Ameren’s bid to gain exclusive rights to build nearly $2 billion of MISO regional transmission projects in the state free of competitors.

The commission in a Nov. 24 order refused to interpret Illinois’ “first-in-the-field” doctrine as Ameren Illinois asked (EL25-105). It said the matter is best left to the state.

Ameren argued in a July petition that Illinois’ first-in-the-field doctrine is the functional equivalent of a right-of-first-refusal law and gives it license to develop the Illinois portions of the lines in MISO’s second, $22 billion long-range transmission plan. (See Ameren Argues Exclusive Rights to MISO Illinois Competitive Tx Projects.)

“We believe that the interpretation of Illinois’ first-in-the-field doctrine is a matter of state law,” FERC agreed. “We are concerned that issuance of a merits order on the petition at this time could conflict with subsequent Illinois court decisions or inappropriately interfere with the Illinois courts’ consideration of Ameren’s arguments.”

FERC said its “declaratory orders to terminate a controversy or remove uncertainty are discretionary” and that it exercised its discretion not to take up the petition.

MISO has put two Illinois projects up for bid from the second long-rang portfolio: the $717.6 million portion of the $984.6 million Woodford County–Illinois/Indiana State Line 765-kV project; and the $940.1 million Sub T–Iowa/Illinois State Line–Woodford County 765-kV project. Ameren argued it should build both.

Among others, the Illinois Commerce Commission (ICC) asked FERC to reject Ameren’s petition and let the state deal with the issue.

FERC pointed out that Ameren already has asked an Illinois court to declare the first-in-the-field doctrine the functional equivalent of a right-of-first-refusal law and allow it to bypass MISO’s competitive bidding.

FERC said it believed Ameren was asking it to construe the law for not only the two long-range transmission projects, but all future transmission projects in Ameren’s Illinois service territory that “otherwise would be eligible to be included in MISO’s competitive developer selection process.”

“In this sense, Ameren appears to request a categorical finding from the commission that the first-in-the-field doctrine will always result in a finding that the doctrine applies. But in each of the cases cited by Ameren in setting forth the doctrine, first-in-the-field determinations appear to have been made on the basis of a contemporaneous record,” FERC wrote.

Ameren argued that Illinois had “broadly” applied the doctrine in bus service, telephone and pager service, for moving companies and for water and sewer service.

FERC concluded Ameren could not cite any case law where the ICC or Illinois courts applied the doctrine “in this manner.”

“[W]e believe that Ameren’s request implicates a question of first impression under Illinois law, and we are not the correct forum for such a novel application of state law,” FERC wrote.

Ameren claimed it wasn’t seeking an interpretation of Illinois law, just FERC’s confirmation that the doctrine is an applicable law MISO should recognize. The ICC accused Ameren of “forum shopping,” with FERC on its list as a means to crush transmission competition.

MISO disagreed with Ameren’s claim that it was wrong to put the projects up for solicitation. The RTO said there wasn’t a “binding determination from an Illinois court or other competent tribunal” to clearly show the doctrine is applicable to the projects.

The Missouri Public Service Commission unanimously approved a settlement agreement on rates for Ameren’s large load customers that insulates ratepayers from most costs associated with supplying data centers’ electricity needs.

The plan defines large load customers as those requiring a maximum 75 MW or more in monthly demand. Supply contracts under the rate would have minimum 12-year terms, with an option for a five-year load ramp period, making for potential 17-year contracts. The PSC sanctioned the rate Nov. 24 (ET-2025-0184).

Agreements would automatically extend for five-year increments unless customers provide a 36-month written notice that they intend to end or reduce their service. Customers who elect not to extend their service must pay exit and early termination fees.

Large load facilities would be required to post collateral equal to two years of minimum monthly bills. Under the plan, they would be able to participate in Ameren’s nuclear and clean energy programs through an expanded clean energy choice rider.

The rate also stipulates that a percentage of excess revenues from large customers be dispersed to benefit ratepayers, with half of the revenues earmarked for low-income customers. Finally, Ameren must evaluate the cost allocations for large loads and ensure that existing customers aren’t paying for costs that should be paid by data centers and manufacturers.

The Missouri PSC said its approval of the agreement is “a significant step forward in implementing” 2025’s Senate Bill 4. The omnibus energy bill enacted by the state legislature prevents large customers’ “unjust or unreasonable” costs from bleeding into other customers’ bills, among other directives.

“Efforts were also made to design a plan that was similar to other tariffs throughout the country, and across Missouri, ensuring Missouri can properly compete for the economic development benefits that these loads represent,” the PSC said in a press release.

Several parties signed off on the settlement agreement, including Ameren, the PSC staff, Google, Sierra Club, Missouri Industrial Energy Consumers, Renew Missouri and Evergy.

The PSC’s vote enshrined more consumer protections than originally were drawn up in the large load rate; an earlier version applied the rate to customers of 100 MW and above and included a 10-year contract term.

Jenn DeRose, a strategist with the Sierra Club’s Beyond Coal Campaign in Missouri, said the rate plan is a “step in the right direction” to protect ratepayers from cost increases from data centers and discourage speculative moves from developers.

“Missourians are rightly concerned about the impacts of new data centers on their electric bills and communities, and they deserve protections,” DeRose said in a statement. “How will customers be protected after Ameren spends billions of dollars of our money on new gas-burning power plants if the AI bubble bursts, the utility overbuilds power plants due to AI speculation, or AI data centers become significantly more efficient?”

Senate Bill 4 also requires utilities to replace retiring plants with dispatchable resources and mandates that utilities source at least 80% of their capacity with dispatchable generation.

That means large loads in Missouri likely would take a lot of natural gas-fired power. Ameren Missouri is planning a significant gas expansion, including the Castle Bluff Energy Center anticipated in 2027 and the Big Hollow Energy Center in 2028. The utility’s 2025 preferred resource plan includes building 1.6 GW of new natural gas generation by 2030 and a total 6.1 GW by 2045. Ameren Missouri’s next integrated resource plan filing is due to the commission in 2026.

U.S. Secretary of Energy Chris Wright has extended the order under Section 202(c) of the Federal Power Act to keep Constellation Energy’s Eddystone Generating Station in Pennsylvania running through this winter.

“Thanks to President Trump’s leadership, the Department of Energy is using all tools available to keep the lights on and heat running for the American people,” Wright said in a statement. “This emergency order is needed to strengthen grid reliability and will help provide affordable, reliable and secure power when Americans need it most.”

The Campbell and Eddystone orders have been challenged in court by state authorities and environmental groups. The former case is further along, with the first substantive briefs due Dec. 19.

Eddystone was scheduled to retire before the summer. PJM dispatched the units during heat waves in June and July, DOE said. The current order will keep the plant running until Feb. 24, 2026. DOE noted the RTO set a winter peak in January 2025.

“Through 2030, PJM anticipates reliability risk from increasing electricity demand, generator retirement outpacing new resource construction and characteristics of resources in PJM’s interconnection queue,” DOE’s order said. “Upcoming retirements, including the planned retirement of the Eddystone units, would exacerbate these resource adequacy issues.”

In total, the two units subject to the order generated 26,434 MWh between June 2025 and September 2025, DOE said in the order.

PJM has been dealing with rising demand and retirements in recent years. DOE’s order said that “will continue in the near term and [is] also likely to continue in subsequent years.”

“This could lead to the loss of power to homes and local businesses in the areas affected by curtailments or outages, presenting a risk to public health and safety,” the order said.

A common theme across the deluge of comments on the Department of Energy’s Advance Notice of Proposed Rulemaking to FERC on large load interconnections was that parties welcomed the process as a vehicle for the commission to improve its rules to help with speed-to-market concerns (RM26-4).

But many of the comments warned FERC and DOE from going too far into jurisdictional issues that could wind up working at cross purposes with the ANOPR’s goal of speeding up interconnections. The first round of comments on the proposal was due Nov. 21. (See Energy Secretary Asks FERC to Assert Jurisdiction over Large Load Interconnections.)

“Any commission action must recognize that large load customers are end-use retail customers, meaning the delivery service they receive necessarily includes an element of local distribution service,” the Edison Electric Institute told FERC. “Even in states that have elected to restructure their electric industry and implement retail choice, the states require that local utilities secure wholesale transmission service on behalf of all retail customers so that they can procure this competitive generation supply.”

The fair and rapid interconnection of large loads can be achieved without calling into question the way states and FERC traditionally have regulated bundled service, the organization said.

“States have successfully regulated retail interconnections for decades, including interconnections of large retail loads, and upsetting that paradigm here may have unintended consequences that could undermine the goals of both EEI members and the commission regarding developing methods to ensure rapid and reliable connection of large loads,” EEI said.

The ANOPR cites EPSA v. FERC as part of the justification for FERC to claim jurisdiction over large loads. In that case, the Supreme Court found that the commission could regulate areas that impact wholesale markets it oversees. But EEI said that decision left intact the Federal Power Act’s savings clause in Section 201, which reserves authorities for the states.

“A court may find an argument that retail customers affect wholesale prices simply because they interconnect to the grid as a clear overreach by the commission,” EEI said.

The National Rural Electric Cooperative Association filed similar comments, saying the ANOPR can help by focusing on issues firmly under FERC’s jurisdiction, but any rule changes should avoid a jurisdictional fight.

If FERC does decide to go forward with asserting jurisdiction, it needs to foreswear jurisdiction over retail sales — even for large loads that connect directly to the transmission system, NRECA argued. The proceeding cannot be a backdoor to impose retail competition on states that are vertically integrated, it said.

“In considering whether to act upon load interconnection processes, the commission should keep core federalism principles at the forefront of its decision-making,” the American Clean Power Association said in its comments. “Load interconnection has historically been a state-jurisdictional issue, and any federal action should be measured and carefully considered.”

FERC could set clear requirements for consistent, timely and transparent load and hybrid interconnections, and then trigger federal action only if and when states and transmission owners cannot keep up with the minimum standards, ACP said.

The Virginia State Corporation Commission, which regulates the largest data center market in the world, made similar comments.

“Under this paradigm, the transmission owners would file with the commission verification that a large load interconnection tariff meeting such requirements has been filed with their state regulatory authority,” the SCC said.

The SCC noted that the ANOPR’s claims about “connecting directly” to the transmission is questionable because almost all such loads have one or more substations on site to step down the voltage before the electricity can be used.

“The legal durability of any final rule in this proceeding will thus depend on the merit of these assertions,” the Virginia commission said. “The VSCC does not believe it is necessary for the commission to even reach these questions, however, as the best approach to these issues is a cooperative one, where the commission sets minimum standards for interconnecting utilities to meet, while leaving it to state commissions to regulate these retail tariffs as they have done for many years.”

The National Association of Regulatory Utility Commissioners argued that nothing in the ANOPR is intended to assert jurisdiction over distribution interconnections, generation facilities and retail sales, and the commission should state that explicitly in any final rule.

“As acknowledged in the ANOPR, FERC has never attempted to assert jurisdiction over end-user load interconnections,” NARUC said. “The reason for this fact is that FERC asserting jurisdiction over load interconnection is outside the boundaries imposed by the FPA.”

If FERC were to assert jurisdiction over the interconnection of a subset of retail customers, it would interfere with the balancing performed by state regulators in retail rate cases and would have significant impacts on all classes of customers.

“NARUC pledges to engage with regulated entities and other stakeholders to explore consensus solutions for FERC’s consideration that will help meet national goals for large load interconnection, while avoiding disputes over jurisdiction that would impede achieving our shared goals,” it told FERC. “Working together, under the concept of cooperative federalism, will lead to optimal solutions.”

FERC can and should regulate large loads’ interstate transmission and wholesale market aspects, the Pennsylvania Office of Consumer Advocate and the Delaware Division of the Public Advocate said in joint comments.

“Due to the resource adequacy and affordability crises that residential consumers face within PJM, the joint consumer advocates support all jurisdictional efforts to effectuate the FPA’s plain text and core purposes as well as cost-causation principles,” they said. “Primarily, the joint consumer advocates support the creation of an expedited large load interconnection queue that includes the large load through its interconnecting utility or electric distribution company, with a workable study time frame, that seriously accounts for participants’ costs to all other affected grid users within the wholesale market.”

Talen Energy’s Susquehanna Steam Electric Station located in Salem Township, Pa. | Talen Energy

The consumer advocates argued that the ANOPR ignores the fact that even very large customers often are connected through distribution facilities that are firmly under the states’ authority.

“FERC should avoid pre-empting existing state authority because courts no longer reflexively defer to agencies’ interpretations of ambiguous statutes, and Skidmore deference will not suffice here,” the advocates said. “A FERC final rule that includes federal pre-emption of any existing, traditional state authority will face an uphill battle under the U.S. Supreme Court’s new standard of review for agency statutory interpretation.”

The ANOPR compares large load interconnections to the process FERC has long overseen for generators, but the Maryland Public Service Commission argued that the two are far different in reality.

“FERC issued Orders 888 and 2003 to correct inefficiencies and discrimination by vertically integrated utilities favoring their own generation resources,” the PSC said. “However, utilities have no comparable incentive to discriminate against large load, as these customers represent valuable opportunities for new retail sales and investment. And unlike generators, end-use customers are retail customers — they do not participate in the wholesale markets.”

Still, like many commenters, the PSC said that FERC can help speed up data center interactions through a policy of cooperative federalism.

The R Street Institute generally supports the expansion of wholesale and retail competition, but it said the fast-paced ANOPR process was not the right venue.

“FERC should narrowly address large load interconnections in ways that hew to the commission’s well supported implementation of generation interconnection planning and that limit regulatory creep,” R Street said. “FERC should further leverage the commission’s competencies and expertise and prioritize litigation risk and implementation concerns.”

What should FERC do in response to the ANOPR?

PJM said a federally regulated large load interconnection process warrants more study, but it urged FERC to move forward on areas where it has firmer jurisdictional footing, such as resource adequacy, ancillary services, interconnection and transmission planning, and NERC reliability requirements.

“Such a construct would have potential benefits including centralization and the promotion of uniform policies and practices,” PJM said. “But, as with the existing generator interconnection process, there will undoubtedly also be costs, claimed delays (many of which will be outside the control of the RTO/ISO), and other complexities that will have to be addressed and that are likely to frustrate the ANOPR’s ‘speed to market’ objective — especially given potential impacts to the existing generator interconnection process.”

The RTO asked FERC to move forward on the pending co-location proceeding that has held up large load issues in its footprint, as did other commenters who do business in its territory (EL25-49).

MISO supports rule changes to help speed up interconnections, but it argued that FERC should respect regional differences.

“MISO’s existing processes effectively reflect unique facts and circumstances of MISO’s system, its states and members,” the RTO said. “Importantly, states and load-serving entities are primarily vertically integrated and responsible for resource adequacy within the MISO footprint. As a result, many states and utilities within MISO have processes which enable them to review and pare through speculative load requests to determine projects with more certainty, allowing MISO processes to enable speed to power for more certain large load interconnections, including determining the associated transmission required to facilitate the required generation interconnections.”

Making large load use the same or a similar process to the generation queue, which has had its own well documented issues with delays, is questionable, the RTO said.

“MISO questions whether standardized large load interconnection procedures will result in the ‘speed to power’ that is necessary to allow the United States to effectively compete in the global competition for economic development, such as in artificial intelligence and creating manufacturing and industrial jobs,” it told FERC.

Meta, the parent company of Facebook and a major player in building data centers, cautioned FERC against a one-size-fits-all approach, even though large load interconnections could benefit from some standardization.

“Some regions of the country are just beginning to bring data centers online, while others have already interconnected substantial large data center loads and are working quickly to add more,” Meta said. “Keeping this momentum going is imperative. Issuing a detailed, standard rule that fails to account for the diversity in the economic landscape could slow down successful interconnection processes and undermine the commission’s goal of bringing more data centers online faster and in a more orderly manner.”

Amazon Energy — Amazon’s energy trading subsidiary — supports FERC action, but whatever the commission does should not upset the planning around data centers that is underway.

“Amazon Energy respectfully urges the commission to apply any new rules or policy changes adopted in this proceeding prospectively, and not to large load interconnection requests currently in progress under existing interconnection procedures,” it said. “Specifically, Amazon Energy proposes any new rules apply only to large load interconnection requests that, as of the effective date of the new rules, have not executed agreements that include a significant financial commitment to the interconnecting utility.”

Google filed comments arguing FERC should work to build out the grid so the growing demand from data centers can be met in a timely and reliable way.

“Now is the moment to right the ship and build out the transmission grid needed to support our nation’s ambitious AI goals,” Google said. “And we must do this with a commitment to affordability: The goal is not to spend more, but to plan better in order to develop a transmission grid that can support the nation’s digital infrastructure needs. Ultimately, a modern, robust transmission grid is the essential platform for delivering affordable, reliable energy to all customers, unlocking transformative dividends across the American economy — from AI leadership to a revitalized domestic manufacturing base.”

The grid needs a holistic planning process, and grid planners need an accurate sense of how much new demand from large loads they will have to meet. Google endorsed SPP’s Consolidated Planning Process, in which generator interconnection and long-term transmission planning are combined.

“The commission should also focus its near-term efforts on identifying pathways to expediting other transmission-level load interconnections that benefit the grid, such as loads that voluntarily offer flexibility via demand reduction or agree to take curtailable transmission service,” Google said. “As with co-located or electrically proximate pairs of load and generation, Google believes that the commission should consider prioritizing reforms to expedite the study of loads that can themselves minimize or help manage the strain on the transmission system.”

Flexibility’s Role

Emerald AI, which works with data centers to make their operations more flexible, endorsed the ANOPR’s idea to create a “Flexible Load Fast Track” for projects that can curtail demand when needed.

“The greatest opportunity in this rulemaking is not merely streamlining the administrative study process but enabling large loads to actively avoid or defer massive grid and energy infrastructure upgrades,” the company said.

The traditional model in which new customers’ load is measured at its maximum and coincident with system peaks requires major investment in new wires and generation and is fundamentally incompatible with the exponential growth and unique physical characteristics of data center demand, Emerald said.

“Delays in interconnection, driven by study processes that do not allow for flexibility — including software-defined flexibility — threaten to stall this economic engine,” Emerald said. “By adopting a technology-neutral, performance-based definition of flexibility and curtailable load, the commission can unlock tens of gigawatts of capacity, ensuring that the U.S. maintains its competitive edge in AI while protecting ratepayers from the costs of unnecessary transmission buildout.”

Non-firm Interconnection Service

American Electric Power commended DOE for launching the rulemaking and said FERC needed to ensure that generation can come online in a timely fashion to serve new large loads. It endorsed the connect-and-manage approach used in ERCOT.

“Under this approach, all generators pay an entry fee and can rapidly connect to the grid, subject to curtailment until supporting network transmission is planned and constructed,” AEP said. “Generators may start as energy resources for some portion of their capacity but are on a pathway to full recognition as capacity resources until supporting network transmission is built.”

The Data Center Coalition also endorsed a change to interconnection service, arguing FERC should regulate energy resource interconnection service more like ERCOT does with connect and manage. Too often, the organization argued, the commission has stringent requirements that are more in line with network resource interconnection service, which is meant to ensure resources can deliver power even during peak hours.

“The stakes are clear: If the United States is to maintain resource adequacy, economic competitiveness and technological leadership, the grid must be capable of interconnecting both load and supply at the pace required by today’s economy,” the coalition said.

NRG Energy urged an even bigger change: using open seasons to help large loads connect to the grid much more quickly.

“A more efficient, market-based approach employing open seasons would provide much needed certainty around the amount and location of large loads, which would benefit regional transmission system operators/independent system operators, transmission owners, generators and consumers alike by facilitating more orderly planning and capital investment,” it told FERC.

Such processes have been used by natural gas pipelines to help raise capital and get customers, NRG said. The Alberta Electric System Operator recently used the concept to allocate open headroom on its system to data center customers.

“AESO began by establishing an interim, reliability-based megawatt limit (1,200 MW) on large load interconnections with its grid and then assigning that capacity to large loads ready to advance in the interconnection process in ‘a fair, efficient and openly competitive manner’ based, in part, on each large load’s ‘willingness to commit’ through the posting of financial security,” NRG said.

Open seasons will require a more proactive role from grid planners, but that should benefit the interconnection and transmission planning processes, NRG said.

“Such an approach is geared toward speed-to-market, getting the most megawatts online at the lowest overall cost, and ensuring a direct allocation of incremental costs to new large users of the grid,” the company added.

What to do about reliability rules?

NERC intervened in the case to ask whether it should consider new rules to deal with issues caused by new large loads and whether the large load customers should have to follow them.

So far customers have not had to follow NERC’s mandatory standards, but the FPA does say they can apply to “users” of the bulk power system and that could cover large customers.

“NERC plans to coordinate with stakeholders over the following year to explore potential revisions to the registry criteria and reliability standards that would incorporate large loads impacting the reliable operation of the BPS,” the ERO told FERC.

The Large Loads Task Force is working on those issues now. NERC laid out a timeline that runs through 2028 to address any needed changes to its mandatory reliability standards in response to the proliferation of large customers.

“Depending on the outcome of these activities, next steps may include NERC registry criteria updates that help mitigate risk associated with emerging large loads,” it said. “As discussed at the commission-led 2025 Reliability Technical Conference, any updates to registry criteria would be dependent upon whether relevant users, owners and operators of the BPS could materially impact, either individually or in aggregate, the reliability of the BPS.”