The geothermal electricity sector continues its slow growth in the U.S., but the cost of next-generation technology has fallen sharply, setting the stage for wider expansion.

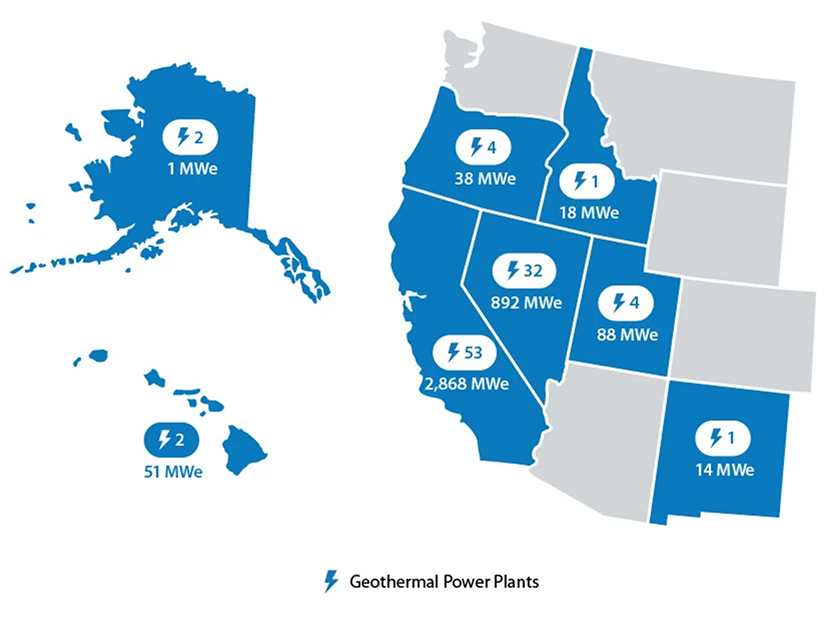

The 99 U.S. plants online in 2024 had a combined nameplate capacity of 3.97 GW, up 8% from 2020, a new report indicates.

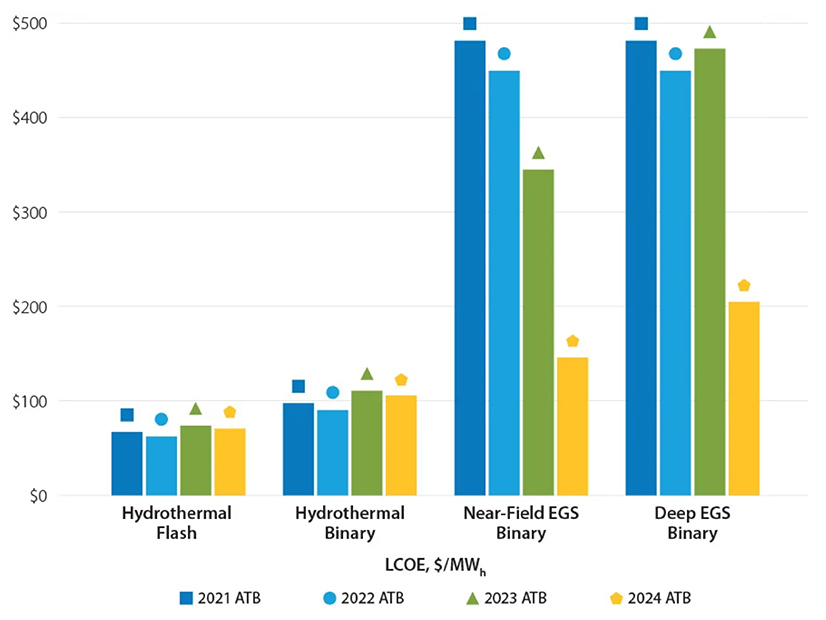

Over the same time frame, the levelized cost of electricity (LCOE) for conventional geothermal technology held relatively steady at $63 to $74/MWh for flash plants and $90 to $110/MWh for binary plants. With reported geothermal power purchase agreements running in the $70-to-$99/MWh range, the authors say, these LCOEs are considered investable for a firm, high-capacity factor source of electricity.

While the LCOE for enhanced geothermal systems (EGS) remained significantly higher — as much as $200/MWh in 2024, depending on technology — it was close to $500/MWh just three years earlier.

Recent advances could lower the cost of EGS to the level of conventional geothermal technology by the mid-2030s, the authors write.

The details come in the “2025 U.S. Geothermal Market Report,” issued in January by the former National Renewable Energy Laboratory (NREL) and nonprofit advocacy group Geothermal Rising.

The levelized cost of electricity from enhanced geothermal systems decreased sharply from 2021 to 2024. | National Laboratory of the Rockies

The Trump administration recently renamed NREL the National Laboratory of the Rockies, an indication and reflection of its energy priorities. However, geothermal energy is among the few components of the renewable energy sector in favor with the current administration amid its push for more oil, gas and coal combustion.

Recent advances in oil and gas extraction techniques have brought down drilling costs in that sector. While geothermal drilling remains more expensive than oil and gas drilling, its costs have declined as well, which is important — drilling accounts for 29 to 57% of the total cost of developing a geothermal field, according to the report, which is an expansion of a 2021 NREL report.

However great its potential, geothermal was a minimally used resource in 2024, accounting for only 15,407 of the 4,308,634 GWh of electricity generated nationwide in all utility-scale sectors, according to the U.S. Energy Information Administration.

The 8% increase in U.S. geothermal generation from 2020 to 2024 was higher than the 7.4% increase for all types of utility-scale generation over the same period.

U.S. geothermal power generation is concentrated in the Southwest. | National Laboratory of the Rockies

Geothermal nonetheless remained one of the least used technologies — wood and other biomass fuels were burned to make three times as many watts as geothermal generated in 2024.

But the report makes an optimistic case for the potential of the earth’s heat to generate more electricity and to heat or cool more structures in the United States.

It indicates the number of geothermal projects in development increased from 54 in 2020 to 64 in 2024 as research improved replicable EGS processes with substantial decreases in drilling time.

As of late 2025, 29 states had enacted geothermal incentive policies, 17 of which encourage geothermal electricity production.

The authors further present geothermal as a component of U.S. energy security and independence: a potential power plant for data centers, a potential option for hybridization with thermal storage and a potential source of critical materials from the extracted underground brine.

A recent analysis by the laboratory estimated 27 to 57 TW of EGS potential at a depth of 0.62 to 4.3 miles across the continental U.S. Approximately 4.4 TW of that is in areas under federal management, but only about 1% of it would be considered economically developable.

California and Nevada remained the center of the U.S. geothermal sector as of 2024, the sites respectively of 53 and 32 of the nation’s 99 facilities.

Analysts with the Public Service Commission of Wisconsin said ratepayers are at risk of subsidizing data centers if We Energies’ proposed rate framework for data centers is given the go-ahead as proposed.

We Energies in late 2025 proposed a framework for customers requiring 500 MW or more to subscribe to dedicated resources, poised to be mostly natural gas at this point.

The utility proposed two types of electricity subscriptions for very large customers: The first would allow data centers to take all of a resource’s output provided they cover all costs associated with the resource; the second would allow data centers to count a resource toward their capacity needs. In the second case, data centers would foot the bill on 75% of the specified resource’s fixed costs; other customers would cover the remaining 25% plus all fuel costs. We Energies theorized that MISO market revenues would be enough to offset the expenses allocated to other customers (6630-TE-113).

Data centers that enroll would be bound to an initial, minimum 10-year contract, renewed thereafter in one-year increments. The rate styles contain early termination provisions where data centers could be billed for unrecovered capital costs if the resources don’t find other customers.

Staff with the commission flagged consumer protection weak spots in We Energies’ filing in late January. They said without stronger protection, utility customers could financially support data centers’ grid needs. They said the 75/25 allocation and 10-year contract term were cause for concern.

Andrew Field, a utility auditor with the commission, said We Energies didn’t capture the full range of market price volatility in its assumption that its other customers wouldn’t underwrite data centers. In testimony, he said We Energies didn’t “provide much detail supporting the specific future scenarios, or potential alternatives, upon which the provided analyses are based.”

Field said We Energies’ own analyses show the potential for costs to exceed benefits for the general rate base.

Even with the hopeful scenarios in its analyses, Field said We Energies found a net benefit for non-participating customers in only 67% of cases that include We Energies’ pending Foundry Ridge turbine project and 81% of the cases that include its planned Red Oak Ridge turbine project.

Tyler Meulemans, a utility financial analyst with the PSC, said he harbors concerns with the 10-year term, including a data center’s “ramp-up period,” when projected load isn’t fully realized. He said including the ramp-up period raises concerns over whether the agreement length is “sufficient to cover the costs incurred to provide service” of a massive data center.

Meulemans said when PSC staff requested a demonstration of revenue recovery would look like during a ramp-up period, We Energies’ analysis showed that a 10-year term “would not cover all costs.”

Two data center projects in We Energies’ territory — Microsoft’s AI data center campus in Mount Pleasant, Wis., and the Vantage/Oracle/OpenAI facility in Port Washington, Wis. — are to double We Energies’ load by 2030. We Energies’ investor presentations show the utility is prepared to spend $19.3 billion on new generation through 2029. The increase of more than $6 billion is due to increasing data center demand.

The Citizens Utility Board of Wisconsin and Power Forward Wisconsin, the latter of which is composed of clean energy groups, oppose the 75/25 allocation and have called on the PSC to make sure data centers pay for all the costs they cause.

Sierra Club’s Jeremy Fisher was critical of the utilities’ proposed rates and said they relied on assumptions that are too rosy.

Fisher said the rate structures “appear to have been negotiated and designed with the company’s new data center customers, Microsoft and Vantage/Oracle,” and rely on the assumptions that immense data centers will become profitable and future customers would have massive electricity needs and the means to finance them.

Fisher asked what happens if the AI boom fizzles.

We Energies “may look at these customers as an enormous opportunity to increase its rate base and expand operations, but the purpose of the tariffs must not only be to provide for reasonable allocation under optimistic conditions but ensure that incumbent ratepayers are protected under adverse scenarios,” Fisher said in testimony to the PSC.

Fisher also said the rates would lead to an “inconsistent and balkanized planning process that should be deeply concerning to regulators in assessing actual resource requirements.”

Richard Stasik, vice president of regulatory affairs of We Energies’ parent company, said PSC staff and interest groups ignored We Energies’ statutory obligation to serve all customers. He said the Sierra Club didn’t quantify risks wrought by data centers and didn’t acknowledge that the situation would be riskier without a dedicated rate schedule.

Stasik said We Energies existing customers would pay at least $1.5 billion in additional capital investments if large customers were to take service under the utility’s existing rate designs.

ACEG said the reforms are starting to improve outcomes in several regions, but rising demand from data centers, manufacturing and electrification are increasing the cost of delay, especially where planning processes remain incremental or reactive.

“Progress is real, but it’s uneven — and demand growth means delay now carries real costs for customers,” ACEG Executive Director Christina Hayes said in a statement. “Where regions have embraced proactive, long-term planning, we’re seeing better results. Where planning remains fragmented, reliability risks and costs increasingly show up in household electricity bills.”

Grades assess performance at the regional level and do not assign responsibility to single institutions, instead reflecting the collective actions of utilities, regional planning organizations, states and other stakeholders. To earn top grades, regions must adopt proactive, long-term, scenario-based planning that evaluates multiple system benefits, integrates regional and interregional needs, and delivers transmission at the pace required to meet rising demand.

CAISO, MISO and SPP continue to show the benefits of proactive, long-term regional planning. SPP’s Coordinated Planning Process, once approved by FERC, would be an important reform that merges transmission planning and generator interconnection planning, the report said.

ISO-NE, NYISO and PJM have shown meaningful improvement due to FERC Order 1920 compliance filings and greater engagement with states.

ERCOT got a C, with the report highlighting the Permian Basin Reliability plan to electrify oil and gas drilling and data centers, which was released in July 2024 with options for 345-Kv and a 765-Kv portfolio. The Texas PUC picked the 765-Kv option in April 2025. While Texas has seen plenty of transmission planned, the report noted it still is done in a “siloed” style, which kept it from a higher grade.

Many regions — including all the non-RTO regions — “continue to face significant gaps in both regional and interregional planning frameworks,” the report said, “In these regions, transmission development often occurs through individual utility investments or ad hoc coordination rather than durable, region-scale planning processes, limiting the ability to fully capture systemwide benefits.”

The West, which is split into three regions, is meeting under the Western Transmission Expansion Coalition (WestTEC), a voluntary interregional planning process that the report called “one of the best interregional transmission planning practices in the country.”

The first report card from ACEG came out in 2023 and ranked the regions before Order 1920 was issued, while the second one from 2024 did not change the grades and checked in after that order. Now, the report takes the requirements from Order 1920 and adds a new focus on interregional transmission.

Load growth forecasts have changed significantly since the last report, with Grid Strategies’ summary of nationwide, five-year peak load forecasts going from 24 GW three years ago to 150 GW in its most recent update. Load growth is affecting transmission development, with FERC saying it was the main driver for 1,000 miles of new facilities in 2024.

“While today’s load growth can tempt a crisis‑response mindset focused solely on short‑term fixes, the industry must move beyond ad hoc solutions and embrace long‑term regional and interregional planning,” the report said. “Proactive, holistic long‑term planning that also accommodates near‑term needs has proven to deliver the lowest costs to consumers. It captures economies of scale that ‘just‑in‑time’ projects miss and enables high‑capacity upgrades to come online ahead of demand.”

The report looked at interregional planning and gave the country an overall “C-minus” that reflects continued reliance on voluntary coordination rather than a formal requirement for regions to implement interregional planning best practices capable of finding the highest value projects.

“The takeaway is not that nothing is working,” Hayes said. “Transmission planning works when it’s proactive, coordinated and long term. The challenge now is scaling those successes fast enough — across and between regions — to keep electricity affordable and reliable for all Americans as demand continues to grow.”

BOSTON — While there is near-universal recognition that New England will need to add a significant amount of new generation over the next two decades, conflicting political and market forces have created major uncertainty about what the next wave of generation projects will look like.

This uncertainty extends to how the region will spur the development needed to meet demand growth, several speakers said at a Northeast Energy and Commerce Association conference on power markets in Boston on Jan. 29.

The scale of the need could be substantial: ISO-NE forecasts peak load roughly doubling by 2050, and decarbonization would require additional clean energy to replace much of the existing fossil fuel fleet.

Incentivizing new generation solely through the wholesale markets may be a difficult proposition. Although energy affordability has dominated policy discussions over the past year, wholesale market prices had remained relatively low until the past two months, which have brought a major increase in energy costs due to sustained cold weather. (See Cold Weather Drives Record December Energy Costs in New England.)

Dan Dolan, president of the New England Power Generators Association, said there has been a “dramatic disconnect” between consumer costs and wholesale market prices. For generators relying on capacity and energy revenues, “if anything, there’s a revenue crisis.”

With consumer prices already high, the increased energy and capacity prices needed to spur new development could lead to political backlash and caps on market prices.

This dynamic has occurred in PJM, where “we’re just now seeing these markets shifting from being long on capacity to being more at equilibrium,” said Ben Griffiths of NRG Energy. “It’s not clear that the prices that [power developers] would require to bring in new entry are actually politically feasible.”

If market prices alone are not enough to bring new generation online, the New England states could assume an even larger role in the procurement of new generation and capacity. But continued reliance on state power procurements would bring its own set of difficulties.

Connecticut’s 10-year power purchase agreement with the Millstone nuclear plant has demonstrated some of these challenges. The difficulty of reconciling PPA costs through rates has led to major swings in the monthly costs to consumers, and Connecticut officials have been pushing for other states to shoulder some of the plant’s costs after the current contract expires in 2029.

Griffiths noted that former ISO-NE CEO Gordon van Welie had pushed the states to take on a larger role in capacity procurement through bilateral contracting.

He added that the region could consider capacity market changes aimed at increasing revenue certainty, such as altering the demand curve to stabilize prices or reintroducing some version of a price lock for new capacity.

But he expressed skepticism about the long-term sustainability of the proposal by the PJM state governors and the White House’s National Energy Dominance Council for a one-time “backstop” auction to procure 15-year contracts with new capacity resources. (See Government-proposed ‘Backstop’ Auction to Test PJM Stakeholder Process.)

“It doesn’t feel long-term sustainable to have bifurcated markets that are providing the same benefits in real time,” Griffiths said, adding that he is “increasingly skeptical of the approach of trying to move all the money out of the capacity market.”

Bob Ethier, current PJM board member and former vice president of system planning at ISO-NE, stressed the need for longer-term solutions to high costs.

“The tension that I see is that there are times where we can do things in the short term that will lower bills but will hurt the market’s functioning in the long run,” he said, emphasizing the importance of maintaining long-term entry and exit signals in the market.

Multiyear price locks for capacity could help reduce year-to-year price volatility, he said, adding that states may be better situated to pursue this strategy than RTOs. He emphasized the need to have these conversations prior to price spikes.

Once a crisis hits, like in PJM, “all we can do is ride [it] out, tweak things around the edges and hopefully learn from it for the next one.”

Policy Pickles

Conflicting objectives between federal and state policies have also added significant challenges and uncertainty to resource development, several speakers said.

“We’re in a pickle in the region for what we can build and what is a sound investment,” said Matt Nelson, principal at Apex Analytics and former chair of the Massachusetts Department of Public Utilities. “We’ve lost some tailwinds and are picking up a lot of headwinds when it comes to clean energy policy.”

Despite the load growth projections and increased demand over the past two years, there is a relatively small amount of generation in the ISO-NE interconnection queue. The first iteration of the Order 2023 cluster study process, initiated by ISO-NE in October, includes 5,632 MW of storage, 355 MW of solar and the 1,200-MW SouthCoast Wind project, which faces considerable challenges from the Trump administration. (See Storage Projects Dominate ISO-NE Transitional Cluster Study.)

Nelson said each new resource category has its own drawbacks: New gas generation seems unlikely with the region’s winter gas constraints and grid’s current “overreliance” on gas; new nuclear looks to be at least 10 years out; the federal government appears to have taken offshore wind off the table; and large-scale solar development faces questions about the loss of federal incentives and a potential capacity revenue hit from ISO-NE’s proposed accreditation changes.

To address load growth amid so much uncertainty about sources of new development, the region must build consensus around a cohesive plan, Nelson said. He added that distributed solar and storage may play an increasingly large role over the next few years.

“State programs are about the only thing left where clean energy resources can get an incentive,” he said.

Aaron Lang, a lawyer focused on clean energy development at firm Foley Hoag, said renewable developers are dealing with “a mountain of uncertainty” related to tariff policy and other potential state and federal policy changes over the past year.

“The pressure is really on the states to do a lot of stuff,” he added, while expressing some optimism about Massachusetts’ efforts to establish a new consolidated permitting and siting process for clean energy resources.

The new process stems from climate and energy legislation passed by the state in 2024. Under the new rules, developers must apply for consolidated state and municipal permits, with the permitting review process limited to 15 months for large projects and 12 months for smaller projects.

The law requires the state to promulgate final regulations by March 1. The state plans to start processing projects through the new process in July.

While there may be some short-term “bumps in the road,” the new process should provide long-term benefits for resource development, he said. “The idea of a consolidated permit is an excellent idea.”

Consumer Cost Drivers

Over the past couple years, New England has seen electricity prices rise faster than inflation, though the inflation-adjusted rate of increase has been relatively modest for most of the region, said Todd Schatzki, principal at the Analysis Group. When accounting for use and rates, customer costs have fallen since 2010 but have risen since 2020, he said.

He emphasized that the cost increases are not felt equally by all customers, with larger impacts on residential customers who have not seen wage growth in line with inflation.

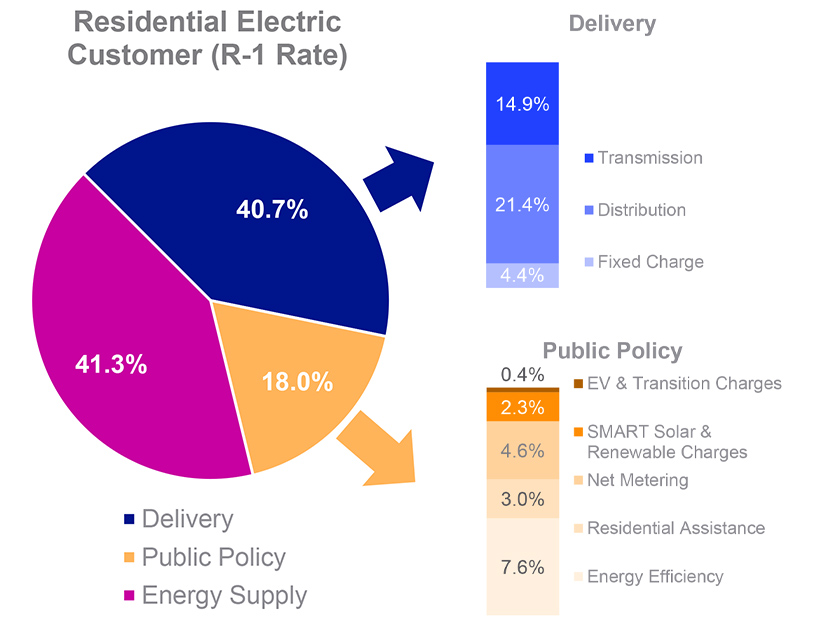

Sandy Grace, vice president of U.S. policy and regulatory strategy at National Grid, presented a cost breakdown of a typical Massachusetts residential electric bill for November. The main cost categories were energy supply (41.3%), distribution (21.4%), transmission (14.9%), energy efficiency (7.6%), net metering (4.6%) and utility fixed charges (4.4%).

Example electric bill for a National Grid residential customer in Massachusetts | National Grid

“It really does require a partnership across sectors to address these costs,” she said.

Rhode Island Public Utilities Commission Chair Ron Gerwatowski focused much of his remarks on the rise of transmission rates in the region.

Asset condition spending, or investment to address degradation of existing transmission infrastructure, has risen significantly in recent years and makes up the bulk of new regionalized transmission spending in ISO-NE. The rising costs, coupled with the limited regulatory scrutiny the spending receives, has prompted efforts to establish internal asset condition review capabilities at ISO-NE.

While this role would not be a regulatory entity, it would be intended to increase transparency into projects and provide information that could be used by third parties to challenge project costs with FERC.

“Quite frankly, it may not be enough,” Gerwatowski said. “We need the transmission owners to temper their appetite for investment in asset condition projects.”

If transmission owners do not scale back their spending, the states may be forced to try to step in and do it for them, he said, noting that states “still control both the method and the timing” of how transmission rates are recovered.

Instead of allowing the quick recovery of transmission spending as pass-through costs, the states could require the recovery of transmission costs through the full base rate case process, he said.

Introducing regulatory lag “could give the financial folks an incentive to push back” on asset condition spending, he said.

If state regulators have little or no confidence in the asset condition planning and development process, he added, “What other options do we have?”

American Electric Power and Springdale Energy will pay ReliabilityFirst a combined $180,000 in penalties for violations of NERC’s reliability standards, according to settlements between the regional entity and the utilities approved by FERC.

NERC submitted the settlements Dec. 30, 2025, in its monthly spreadsheet notice of penalty, along with a separate nonpublic SNOP regarding violations of NERC’s Critical Infrastructure Protection standards (NP26-3). FERC indicated in a Jan. 29 filing that it would not further review the SNOPs, leaving the penalties intact.

AEP’s settlement, carrying a $150,000 penalty, concerned PROC-026-1 (Relay performance during stable power swings), which was in effect from 2018 to 2024. The standard has been replaced by PRC-026-2, but the violation by two AEP subsidiaries, Ohio Power and Indiana Michigan Power, occurred while the earlier version was in effect, according to a self-report submitted by the utility in October 2022.

According to the settlement, PJM notified AEP in December 2020 that it had added the utility’s 765-kV Sorenson-Marysville line to its list of elements covered by PRC-026-1. Requirement R2 of the standard says a transmission owner must ensure the load-responsive protective relay settings on a transmission line meet the criteria in the standard within 12 months of being notified of the line’s inclusion.

The Sorenson substation is owned by Indiana Michigan Power, while the Marysville substation is owned by Ohio Power, and both are managed by separate engineers. While the engineer overseeing the Marysville facility reviewed the line relays within the 12-month period, the Sorenson facility’s manager did not review its relays until August 2022, about eight months after the deadline. Two of the relays were found to be out of compliance and require adjustment.

RF determined the root causes of the violation were “ineffective internal controls and workflow tools to ensure evaluations were completed in compliance with PRC-026-1,” the RE wrote in the SNOP. AEP had flagged the Sorenson relays within its tracking system, but no one was assigned to complete the evaluation and no follow-up notifications were issued to ensure completion.

RF also observed a lack of coordination between AEP’s subsidiaries, with the engineer from Indiana Michigan incorrectly assuming Ohio Power’s engineer would complete the evaluations on the Sorenson facility as well as the one in Marysville.

The RE assessed the violation as posing a moderate risk to grid reliability: greater than minimal because an extra-high voltage line was affected, the evaluation was late and the relays eventually were found to be noncompliant; but not serious or substantial because of the “limited scope of the noncompliance.” RF acknowledged that AEP performed an extent of condition review across the footprint of all its operating companies and found no other instances of noncompliance with PRC-026-1 R2.

AEP’s mitigation activities included performing the required evaluations of the Sorenson-Marysville line, along with the extent of condition review and creating a unified process for evaluating relays for PRC-026 compliance. The utility also updated its tracking system to specify the due date, estimated completion date and personnel assigned to each task.

Vendor Failed to Ensure Springdale’s Compliance

Springdale’s settlement stemmed from a violation of PRC-025-2 (Generator relay loadability). The utility notified RF in August 2022 that it was in violation of requirement R1 of the standard, which requires generator owners to apply the appropriate settings to their load-responsive protective relays “while maintaining reliable fault protection.”

RF observed that Springdale’s violation “was a continuation of a prior noncompliance” that the utility had failed to fully mitigate. Springdale reported the initial noncompliance in February 2020, telling the RE that it had failed to ensure the correct relay settings on three of its five generating units. To mitigate the issue, the utility hired a vendor to update the relay settings.

A month later, the vendor reported it had completed the updates; based on this report, Springdale reported to RF that mitigation was complete. However, when the utility retained a new vendor to review relay settings two years later, the second vendor discovered the settings still were not in compliance.

Springdale launched an investigation into the original vendor, which reported that “the technician who performed the work had properly changed” one relay’s settings but had incorrectly changed another. Six relays were affected by the oversight. The original vendor returned to fix the error in May 2022, but the second vendor reported in June that one of the units still was not compliant, affecting two relays. These finally were brought into compliance in November 2022.

RF determined that the root cause of the second noncompliance was vendor oversight, because the utility did not validate that settings changes had been implemented correctly. The RE assessed the violation as a moderate risk, observing that although the noncompliance lasted more than three years and the size of the settings changes increased the risk of an unnecessary trip, the limitation to three of five generating units “somewhat” reduced the potential magnitude of harm. The earlier violation did not constitute a reason to aggravate the penalty, RF added.

Springdale’s mitigation efforts included updating its vendor contracts to require engineering review of changes within 48 hours and vendor draft reports within 30 days after completion of work. The utility also implemented a vendor quality assurance process to ensure Springdale staff review the vendors’ work, and a requirement that the NERC compliance manager review the vendor draft report to check that it includes all necessary information to demonstrate compliance.

CAISO released its first mandatory report under the California assembly bill that paves the way for an independent regional organization to assume responsibility over the ISO’s energy markets.

Under AB 825, CAISO must submit an annual report to the California governor and Legislature about the ISO’s various initiatives and decisions. Gov. Gavin Newsom signed the law in September 2025, and CAISO submitted the first report to the Legislature on Feb. 1, according to a news release.

“The ISO appreciates the commitment by Gov. Newsom and the Legislature to support independent governance of the real-time and day-ahead regional electricity markets that benefit consumers across the West,” CAISO CEO Elliot Mainzer said in a statement. “We look forward to continuing to work with the state and stakeholders throughout the region to help make that new governance framework a reality.”

AB 825 allows for the creation of an independent organization to oversee CAISO’s Western Energy Imbalance Market and soon-to-be-launched Extended Day-Ahead Market. The bill authorizes CAISO and California’s investor-owned utilities to join the organization.

In the AB 825 report, CAISO listed activities from the past year, including federal tariff proceedings, policy initiatives, decisions, market activity and transmission planning.

The report lists suggested enhancements to congestion revenue rights, initiatives to address reliability needs and uncertainties between the day-ahead and real-time market, new resource adequacy rules, storage enhancements and greenhouse gas coordination, among other initiatives.

CAISO also is working to “extend participation in the day-ahead market to the [WEIM] entities in a framework similar to the existing WEIM approach for the real-time market. EDAM will improve market efficiency by integrating renewable resources using day-ahead unit commitment and scheduling across a larger geographic area,” according to the report.

The report notes that CAISO intends to seek approval from its Board of Governors for its 2025/26 transmission plan in May 2026.

Under the 2024/25 transmission plan, CAISO received approval for 31 projects valued at $4.8 billion, 28 of which are for reliability purposes for $4.6 billion. The ISO estimated it needs 76 GW of additional capacity to meet increasing building electrification and electric vehicle loads. (See CAISO Approves $4.8B Transmission Plan to Support 76 GW of New Capacity.)

NYISO began what is expected to be a yearlong effort of revising its Reliability Planning Process at a Transmission Planning Advisory Subcommittee meeting Jan. 20.

“This is the best opportunity, if you have more concrete feedback, especially any specific suggestions so that we can consider those as we consider revisions before we roll them out,” said Ross Altman, NYISO’s senior manager of reliability planning.

The existing process uses a single base case to determine whether the transmission system meets all reliability criteria. Base case assumptions are identified in May, finalized over the summer and voted on in fall. The final reliability need assessment is issued in late fall. This goes hand-in-hand with the Comprehensive Reliability Plan (CRP), which considers system conditions a decade into the future.

“The only specific feedback we’ve received so far to process revisions is to consider a longer horizon,” Altman said. “There was a suggestion of 15 years. We welcome folks’ thoughts on that.”

Altman said the use of base case means the ISO needs to use the most conservative assumptions to account for growing uncertainty across all elements of grid planning. (See NYISO’s 2026 to be Dominated by Reliability Concerns.) The use of a single base case when reliability margins are tight can mean “flip flopping” between having and not having a reliability need.

Several stakeholders said they were concerned with moving away from a single base case to multiple base cases or scenarios that might trigger a reliability need. Representing Multiple Intervenors, Mike Meager asked Altman to clarify how the ISO would weigh different scenarios or circumstances probabilistically.

Altman said it was difficult this early in the process for the ISO to come up with a “true stochastic” look at probabilities.

“Not declaring needs on outliers is something we’re thinking about how to accomplish,” Altman said.

He said the process must maintain that reliability needs be based on criteria, and he added that multiple combinations of system conditions could more accurately reflect the changing grid. He stressed that the ISO was committed to “open and transparent” stakeholder involvement in revising the process.

The ISO is planning to review key study assumptions for the 2026 reliability needs assessment study with a particular focus on load uncertainty, aging generation, emergency assistance and generator outage rates.

Howard Fromer of Bayonne Energy Center asked how the ISO planned to stick to a 10-year planning horizon for the CRP, given that it was planning on folding multiple forecasts into the reliability process.

“How do we prevent that flexibility you’re looking for from swamping the competitive market, which is what we designed to achieve whatever our reliability requirements are?” Fromer asked.

Altman said that was always a risk when using a decadelong planning horizon for a one-year market. He suggested that the issue be separated from short-term reliability needs planning.

Fromer replied that it deserved consideration because the ISO could force a lot of unnecessary infrastructure investment.

Another stakeholder asked whether NYISO would consider changing some of its base case inclusion rules to be more realistic rather than conservative. Meager said he agreed and wanted the ISO to seriously consider how realistic its assumptions are.

“It’s not difficult to show some reliability criteria will be violated … if there’s no bounds or restrictions or constraints on what assumptions the NYISO can pick and choose to use each year,” Meager said.

Altman replied that the ISO is indeed considering the issue.

Alex Novicki, representing Avangrid, requested that extreme weather events be accounted for in the base case because, he said, NERC was going to try to account for them in upcoming resource adequacy standards.

Meager also questioned the ISO’s timeline for potential changes.

“What you are contemplating are some of the most significant changes to the Reliability Planning Process we have ever considered, with huge impacts moving forward,” Meager said. “There’s not a lot of meat on the bones before us right now. The idea that we’d be voting on tariff changes in a couple months is incredibly ambitious, if not highly unlikely.”

New York generators had to rely on oil as gas was scarce throughout the Eastern Interconnection during the Jan. 25-27 winter storm, NYISOsaid in a preliminary analysis that was a last-minute addition to the Installed Capacity Working Group’s agenda Feb. 2.

“We wanted to be timely and at least talk about some high-level stuff about what happened last week for folks so we could at least level-set some of the conversation,” said Shaun Johnson, NYISO vice president of market structures.

While the storm, dubbed “Fern” by the Weather Channel, caused few disruptions in the Northeast, it had such a large footprint that it affected demand and prices across the East.

“For those of you who are upstate New York natives, last week’s weather was cold, but it wasn’t extreme New York cold,” Johnson said. “The really important part of this is that it was cold in Atlanta.”

The weather created high demand for natural gas, causing price spikes that rippled through the market. Downstate generators had difficulty obtaining natural gas at all. Index prices during the winter storm were in the $50 to $200/MMBtu range, with some spot quotes in excess of $300. Average prices typically are much lower, with Johnson citing October 2025’s average of $2.17/MMBtu as an example.

Dual-fuel units shifted to trucked-in oil, which is less efficient than piped gas. Simultaneously, snow on solar panels and overcast conditions prevented solar resources from shaving down the peak load.

“During the first two days of Fern, we went through 20% of our oil inventory in New York,” Johnson said. He said the ISO ran its fuel survey multiple times over the week and heard stories of oil-fired generators being continuously served by caravans of tanker trucks “running out the gate” the entire week.

Johnson opened a map of the U.S. from the National Oceanic and Atmospheric Administration that showed the entirety of New England, New York and most of the PJM footprint under an extreme cold advisory. Cold weather extended southward into Tennessee Valley Authority and SPP territory. Effectively, the entire eastern half of the U.S. was in a state of elevated natural gas and electricity demand.

Johnson cited the NYISO 2025 Gold Book forecast of 24,200 MW of peak load in winter. He said the ISO had come close to that several days the previous week. He displayed a graph of day-ahead peak load forecasts during Fern that plateaued just under the Gold Book forecast for several days.

Additionally, several emergency actions were taken to reduce demand. The Special Case Resource program was activated multiple hours daily Jan. 25 to Jan. 30.

External prices also were extremely high, making it impossible to stabilize prices with cheap imports, Johnson said.

For most of the electrical industry’s history, weather was a constraint we designed around. Climate, by contrast, now is a system we operate inside of: a wild, unstable system.

That distinction matters more than many grid leaders, regulators and policymakers have absorbed. Extreme heat, wildfires, intense rain, drought and sea level rise often are approached as separate hazards — each deserving its own planning docket, modeling exercise or capital program. And while this column just completed a series on the impact of each hazard on the grid, they are not a collection of independent risks; they are a tightly coupled system of climate-driven stresses that interact, compound and persist in ways the grid never was built to handle.

Climate risk no longer is an environmental problem. It’s a governance, planning and management problem. And it sits squarely on the desks of utility executives, system operators and policymakers.

From Discrete Events to Systemic Risk

The industry knows how to deal with events. We respond to heat waves, storms, fires and floods when they occur individually. Mutual assistance is activated, crews are staged, emergency declarations are issued and restoration begins.

Climate change has turned those events into conditions.

Dej Knuckey

Heat no longer is a single-day peak but a multiday, multinight stress that simultaneously drives record demand, reduces generation efficiency and lowers transmission capacity. Drought is not just a hydroelectric issue; it constrains thermal cooling, increases wildfire risk and exposes weaknesses in the water-energy nexus. Wildfires are not seasonal hazards but year-round threats with cascading impacts on air quality, solar output, worker safety and liability exposure. Extreme rainfall doesn’t merely knock down lines; it floods substations, undermines foundations and complicates recovery logistics. Sea level rise isn’t a future storm-surge problem; it’s a slow, permanent redrawing of where infrastructure can safely exist.

Taken together, these risks do not stack neatly. They collide.

A heat dome can arrive during a drought, elevating fire risk. Fires strip vegetation, increasing the likelihood of debris flows and flash flooding when rain eventually comes. Flooded substations disrupt power to water systems just when pumping capacity is needed most. Smoke degrades solar output and limits air operations for line inspections. Each stress amplifies the next.

We can’t plan for each hazard in isolation.

Polycrisis, Meet Multisolving

Two terms I keep coming back to as I consider how the industry will manage in a future in which uncertainty is the norm are polycrisis and multisolving.

The term “polycrisis” was coined by French complexity theorists in the early 1990s and popularized in the early 2020s as the planet struggled with a pandemic, climate change, wars and economic instability. Climate change interacts with energy sources, generation, transmission and distribution infrastructure and the safety, well-being and economic stability of residential and commercial customers. It interacts with other critical infrastructure systems that both depend on and support the grid. And this is happening against a backdrop of income inequality, declining health outcomes, population migration and unstable federal emergency management support. Climate is not a single crisis for the grid.

“Multisolving” was coined by Dr. Elizabeth Sawin and focuses on the positive flipside of the coin: solving for one problem can solve for others. Think of it as the BOGO of the solutions crowd. For the grid, building resilience against one extreme challenge comes with the bonus of creating resilience against others, with a further ripple effect of improving reliability and lowering corporate exposure. Similarly, decarbonizing the grid with renewables and energy storage comes with the bonus of lowering exposure to fuel prices, increasing grid stability and improving the health of communities near power generation.

They are both linked to unintended consequences: polycrisis in a negative sense where one challenge results in multiple, compounding challenges; multisolving in a positive sense where one solution solves more than one challenge.

Grid Resilience in the Time of Climate Change

Most grid planning frameworks still assume three things that no longer hold: historical climate baselines, independent hazards and short disruption durations.

Reserve margins, resource adequacy models and integrated resource plans often are still calibrated to yesterday’s weather. Reliability metrics reward fast restoration after discrete outages, not the ability to avoid catastrophic system failure during prolonged, overlapping stresses. Yesterday’s n-1 contingency planning won’t work when climate delivers n-many failures simultaneously.

The problem isn’t a lack of data. Climate science has advanced rapidly, and hazard modeling is more sophisticated than ever, assuming inputs and assumptions are adjusted for today’s reality. The problem is institutional inertia: Planning processes and regulatory structures have not evolved at the same pace as the risk landscape.

The industry needs to focus on correlation risk. Heat waves reduce solar efficiency at the same time demand peaks. Wildfire smoke causes “wiggling” in photovoltaic output while also limiting crew deployment. Flooding disrupts electricity, communications and transportation at once. These interactions are predictable and need to be built into planning assumptions.

This planning needs to be done against a backdrop of rapidly accelerating risk. The creators of the First Street Correlated Risk Model found, “the frequency of losses resulting from major climate disasters in the U.S. has increased over fivefold in the past four decades, with climate change and increased development in vulnerable areas being the primary drivers.”

And there’s no one-solution-fits-all. Existing adaptation approaches typically assume rather simplified models, an IEEE study found. “The reality, however, is that climate change patterns and the uncertainties they introduce can differ regionally, complicating the formulation of effective countermeasures.”

As climate hazards become more frequent, more extreme and more varied, the industry can’t afford to rely on plans that appear robust on paper but are brittle in practice. The industry must invest in comprehensive planning and prioritize infrastructure upgrades that address multiple risks.

Climate Risk Has Become a Balance-Sheet Issue

The most underappreciated shift may be financial rather than technical.

Climate exposure is reshaping utility balance sheets. Wildfire liability has driven bankruptcies and forced restructuring, insurance providers are retreating from high-risk regions or sharply raising premiums, and credit rating agencies are flagging climate exposure as a material risk. Capital costs are rising fastest for utilities with the greatest climate vulnerability, often the same utilities facing the largest infrastructure reinvestment needs.

In effect, climate risk is becoming a de facto regulator, often acting faster and more bluntly than public utility commissions.

This matters because resilience investments too often are framed as discretionary or extraordinary: nice to have if regulators approve, deferrable if rates are politically sensitive. But in reality, failing to invest in resilience now simply shifts costs forward, where they reappear as higher borrowing costs, insurance gaps, emergency repairs and, ultimately, customer harm.

Swiss-Re Institute, which studies the risk landscape closely — because reinsurance companies are the ones pricing the growing risk — said, “Ongoing risk assessment is necessary to ascertain how resilient infrastructure is. Assets that are poorly maintained are more vulnerable.”

Conversely, today’s resilience investments can pay dividends beyond repairing and preparing for the same risk. Think about the $1 billion, four-year Con Edison storm fortification initiative following Superstorm Sandy: It was triggered by outages following a storm surge, but is paying dividends as the utility faces ice storms, heat waves and more.

Executives who treat climate adaptation as an environmental compliance issue are misreading how quickly financial markets are moving.

No Utility is an Island

Another lesson emerging across climate hazards is that grid resilience cannot be built in isolation. Power outages cascade. They shut down water pumping and wastewater treatment. They cripple communications networks. They undermine emergency response and health care delivery. During fires and floods alike, loss of electricity turns manageable crises into life-threatening ones.

Yet in many states, energy planning remains siloed from water utilities, emergency management agencies, transportation departments and telecom providers.

Cross-infrastructure coordination can’t be ad hoc or occur only after a disaster. Integrated planning and response reduce both risk and cost. If infrastructure needs to be protected from rising sea levels, for example, it’ll be more cost effective if all affected agencies coordinate resilience investments, hardening power, water, wastewater treatment and roads simultaneously.

At the same time, a region may be more of an island than ever before: If multiple states face an event at the same time, like the winter storm that recently shut down a solid slice of the lower 48, mutual aid agreements break down as crews are needed locally and flying in distant crews becomes impossible. Mutual aid is ideal, but some disasters will be more Lord of the Flies than Swiss Family Robinson.

Resilience is not something the power sector can buy on its own. It is an interdependent system, and governance structures have to reflect that reality.

What a Climate-adjusted Grid Strategy Actually Looks Like

If climate risk is now a core management challenge, what follows is not a checklist of projects but a shift in mindset.

First, resilience must move beyond asset hardening toward system flexibility. Hardening substations and elevating or undergrounding equipment remain necessary, but they are insufficient on their own. Islandable microgrids, distributed energy storage and modular recovery strategies allow systems to absorb shocks rather than simply resist them. Flexibility — not brute strength — is what enables systems to function under compound stress.

Second, planning must explicitly account for duration. Multiday heat waves, weeks of wildfire smoke, yearslong droughts and permanent sea-level rise pose fundamentally different challenges than short, sharp events. Planning processes that focus on peak hours or single-day extremes underestimate both operational strain and human fatigue.

Third, we must align incentives with future conditions. Regulators play a critical role here: Cost-recovery frameworks still favor post-event rebuilding over preemptive adaptation, even though avoided outages and avoided disasters deliver far greater public value. Utilities, for their part, need to treat resilience as a core dimension of service quality — not a regulatory add-on.

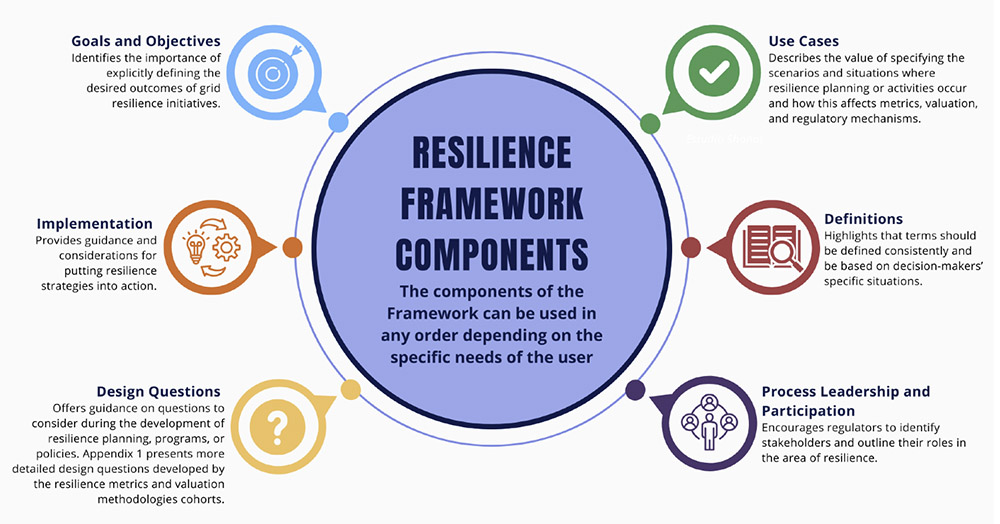

Planning for grid resilience requires a comprehensive framework such as the one developed by NARUC | NARUC

Fourth, reliability metrics need updating. Measures that prioritize restoration speed after outages do little to encourage investments that prevent catastrophic failure in the first place. In a climate-altered grid, success increasingly looks like outages that never happen, liabilities that never materialize and emergencies that never escalate.

Leadership in a Non-Stationary World

The grid already is operating inside a climate-stressed environment. The question facing leaders and policymakers is not whether the lights can be kept on during the next storm, it is whether governance structures, planning tools and investment frameworks can evolve fast enough to manage permanent instability.

That evolution will be uneven. Some utilities and system operators are already internalizing climate risk as a core design constraint. Others remain trapped in a compliance mindset, waiting for clearer regulatory signals or the next disaster, legal action or insolvency to force action.

The future of our industry will not be defined by how cheaply it delivers electrons, but by how well it absorbs shock, and that can happen only if leaders treat climate risk as the multidimensional management challenge it has become.

With natural gas being the dominant fuel for electricity generation in New York, rising electricity prices are driven by the increased cost of gas because of the ongoing Russia-Ukraine War and increased LNG exports, according to a recent policy paper by NYISO.

The paper, released Jan. 29, comes after a week of winter weather and elevated off-peak prices. It relied on the Short-Term Energy Outlooks (STEOs) by the Energy Information Administration and an analysis of electricity prices by Lawrence Berkley National Laboratory.

Prior to the surge in LNG exports, prices remained low because of the shale gas fracking boom of the late 2000s, just as President Barack Obama entered office. Around the same time, Russia began antagonizing Ukraine, culminating in the invasion and annexation of the Crimean Peninsula in 2014. Russia, which also controlled most of Europe’s supply of natural gas, cut off supply to Ukraine the same year.

To counter Russia’s aggression and lessen Europe’s dependency, the Department of Energy under Obama began in 2012 to issue approvals of LNG facilities for exports to countries with which the U.S. did not have free-trade agreements, a policy that continued under Presidents Donald Trump and Joe Biden — though Biden would unsuccessfully attempt to pause such exports in early 2024.

The U.S. became a net exporter of LNG in 2017 and the world’s leading exporter in 2023, according to a 2024 study at Harvard University. In its STEO for January 2026, EIA noted that LNG exports in 2025 increased by roughly 26% compared to 2024 exports, growing to an estimated 15 Bcfd.

“For context, U.S. residential gas customers consume approximately 12 billion cubic feet of gas per day,” the NYISO paper says. “In other words, the U.S. is forecast to export more natural gas than residential customers are expected to consume.”

The result has been a strong correlation between gas and electricity prices across the U.S., including in New York. The Transco Zone 6 pricing hub is the primary procurement site for the state’s gas fleet. In 2020, amid the COVID-19 pandemic, the price at the hub was $1.64/MMBtu. In 2022, Russia began its full-scale invasion of Ukraine, and exports to Europe — sent over pipelines that run through Ukraine — dwindled. The Transco 6 price shot up to $7.01/MMBtu.

The price for electricity followed the spike, from the record low of $25.70/MWh in 2020 to $89.23/MWh in 2022, according to the paper.

While prices for both electricity and gas fell in the short term, they gradually rose again over the next three years as LNG exports continued to grow. In 2024, gas traded on average at $2.10/MMBtu; by 2025 prices were hovering around $4.64/MMBtu. “The result was significantly higher wholesale prices for electricity as well — with an average price of $74.40/MWh throughout 2025, compared to $41.81/MWh for 2024,” the paper says.

The paper was published just after a Jan. 28 meeting of the Budget & Priorities Working Group in which stakeholders asked NYISO staff why energy prices were trading high when load was not near peak.

“We’re noticing right now that while the load isn’t great, the marginal cost of energy is very high,” said Kevin Lang, a lawyer representing the New York City and Multiple Intervenors.

Many stakeholders asked for specifics on hourly pricing, and what facilities on which pipelines were involved in setting daily natural gas prices.

“It’s not just as simple as ‘Transco 6 day-ahead cleared at X,’” said Doreen Saia, chair of natural resources law at Greenberg Traurig. “There’s a lot of factors going on.”

In an email, Lang told RTO Insider that the policy paper did not answer his questions about why energy prices had been surging during periods of low demand, particularly in recent days. According to Yes Energy data, off-peak prices have been on average higher than on-peak prices over the previous 10 days.

Barbara Kates-Garnick, a professor of the practice of energy policy at Tufts University and former Massachusetts Department of Public Utilities commissioner, said rising price trends could be broadly attributed to natural gas prices, Trump’s energy export policy and demand.

“Exporting LNG does subject all burns over time to world markets,” Kates-Garnick said. “Global natural gas prices were something that we had to become more sensitive to” during her time on the DPU and as undersecretary of energy.

She said the question facing local policymakers is whether to invest in infrastructure or “cobble” solutions together to deal with emergent price spikes.

“We keep pushing this can down the road. Every time it emerges, we address it as if it’s a new problem,” she said. “It’s very frustrating.”